40 / 92

40 / 92

40

ADVISING ON VCTs

Clearly, due to their risk profile and tax benefits, VCTs are not going to be suitable for everybody. Not everybody will have

the requisite tolerance for risk or capacity for loss, and not everybody will have maxed out their other, lower-risk tax-efficient

investment options. But, because of their unique features, VCTs can have a role to play at any stage of a financial plan:

accumulation, at retirement and decumulation.

SUITABILITY

It makes sense to start by placing VCTs in the context of the other tax-efficient investment options that are out there:

The focus should be on the conventional

first - using up the ISA and pension

allowances. These are lower risk

options (or more accurately they can

be depending upon what is invested

in - they are only wrappers for allowable

investments) that provide tax reliefs

and form the backbone of saving and

investing plans. Pensions have recently

become much more attractive from an

estate planning perspective as well, with

the removal of the punitive 55% “death

tax”. Ordinarily you would expect to see

extensive ISA and Pension investments

made before VCTs are considered.

However, new lower annual and

lifetime pension investment limits,

new limits on what people earning

greater than £150,000 can save and the

threat to higher rate tax relief are all

going to mean that more people than

ever before are going to have to look

beyond pensions for other tax-efficient

investments. And consumers looking to

offset particularly high Income Tax bills

will be attracted by the upfront relief

regardless of whether they are at or

near their pension and ISA limits.

At the other end of the spectrum, EIS

and SEIS investments are usually - but

not always - more risky than VCTs. Like

VCTs, they invest in smaller companies,

but they are unquoted vehicles with

very low levels of liquidity. They have

more generous tax reliefs than VCTs,

pensions and ISAs to reflect the fact that

they are more risky.

As a consequence, all things being

equal you might expect to see VCTs, as

the lower risk option among the Tax-

Advantaged Venture Capital Schemes,

being used in clients’ portfolios before

EIS were: however, the higher annual

investment limit and additional benefits

around IHT relief and CGT deferral often

mean that EIS are preferred to VCTs.

Of course the major attraction of VCTs

is the upfront Income Tax relief, but

investors can only claim relief on what

they have paid. Therefore it is unlikely

that VCTs are often going to be suitable

for basic rate taxpayers - the relief is

unlikely to be great enough to justify

the risk.

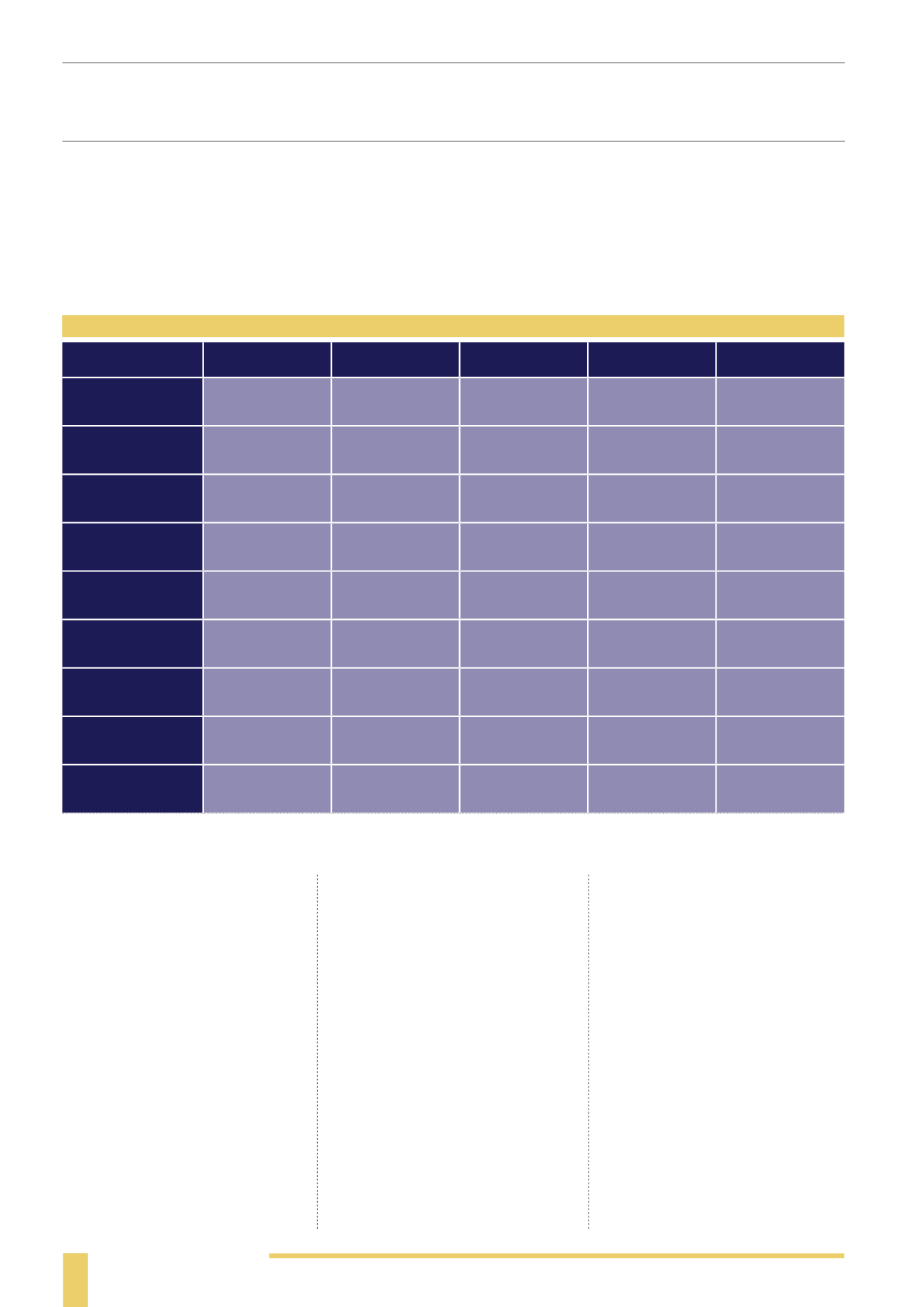

As a rule of thumb, as you move to the right-hand side of the table, you will be looking at riskier investments. Note income in ISAs is taxed at 10%, which does

represent a significant saving for higher rate taxpayers

COMPARING TAX-EFFICIENT INVESTMENT OPTIONS

ISA

PENSION

VCT

EIS

SEIS

ANNUAL CAP

£15,240

£40,000

£200,000

£1m

£100,000

LIFETIME CAP

x

£1.25m / £1m

x

x

x

INCOME TAX

RELIEF

x

√

30%

30%

50%

LOSS RELIEF

x

x

x

√

√

IHT RELIEF

x

Depends

x

√

√

CGT FREE

GROWTH

√

√

√

√

√

CGT DEFERRAL

x

x

x

√

√

TAX-FREE

INCOME

x

x

√

x

x

TAX-FREE

LUMP SUM

√

25%

√

√

√