42 / 92

42 / 92

42

of 6% and invested £10,000 for ten

years, the return (excluding the impact

of fees and the upfront 30% Income Tax

relief) is £31,058 or 211%.

If we made the same investment, but

this time the dividends were taxed at

38.1% (the rate for higher rate taxpayers

today), the return would be £25,270 or

153% a difference of £5,788.

This suggests that participating in the

Dividend Reinvestments Schemes (DRIS)

that many VCTs run is perhaps the best

way of investing for the long run.

AT RETIREMENT - HOW DO

VCTs INTERACT WITH THE

NEW PENSIONS FREEDOMS?

It’s worth considering VCTs and

pensions, and how they interact with

each other - especially in the light of so

many recent changes to the rules and

regulations governing pensions.

LIFETIME ALLOWANCE

We’ve already mentioned the first

change to consider - the reduction in the

lifetime allowance. This has come down

from a peak of £1.8 million in 2011 to

just £1.25 million* at the time of writing,

soon to be lowered again to just £1

million.

£1 million might sound like a lot of

money, but at current rates it would

buy an annuity worth approximately

£33,000 a year (before tax) for a 65 year

old - for many people that might not be

enough for the lifestyle they want.

The two charts on this page and the

following page show that advisers will

have many clients who will potentially

reach, or breach, the £1.25 million limit

(note that both assume no further

contributions).

Of course, what the reduction in the

lifetime allowance means is that many

savers and investors will have to look

for other tax-efficient options, beyond

pensions and ISAs - such as VCTs.

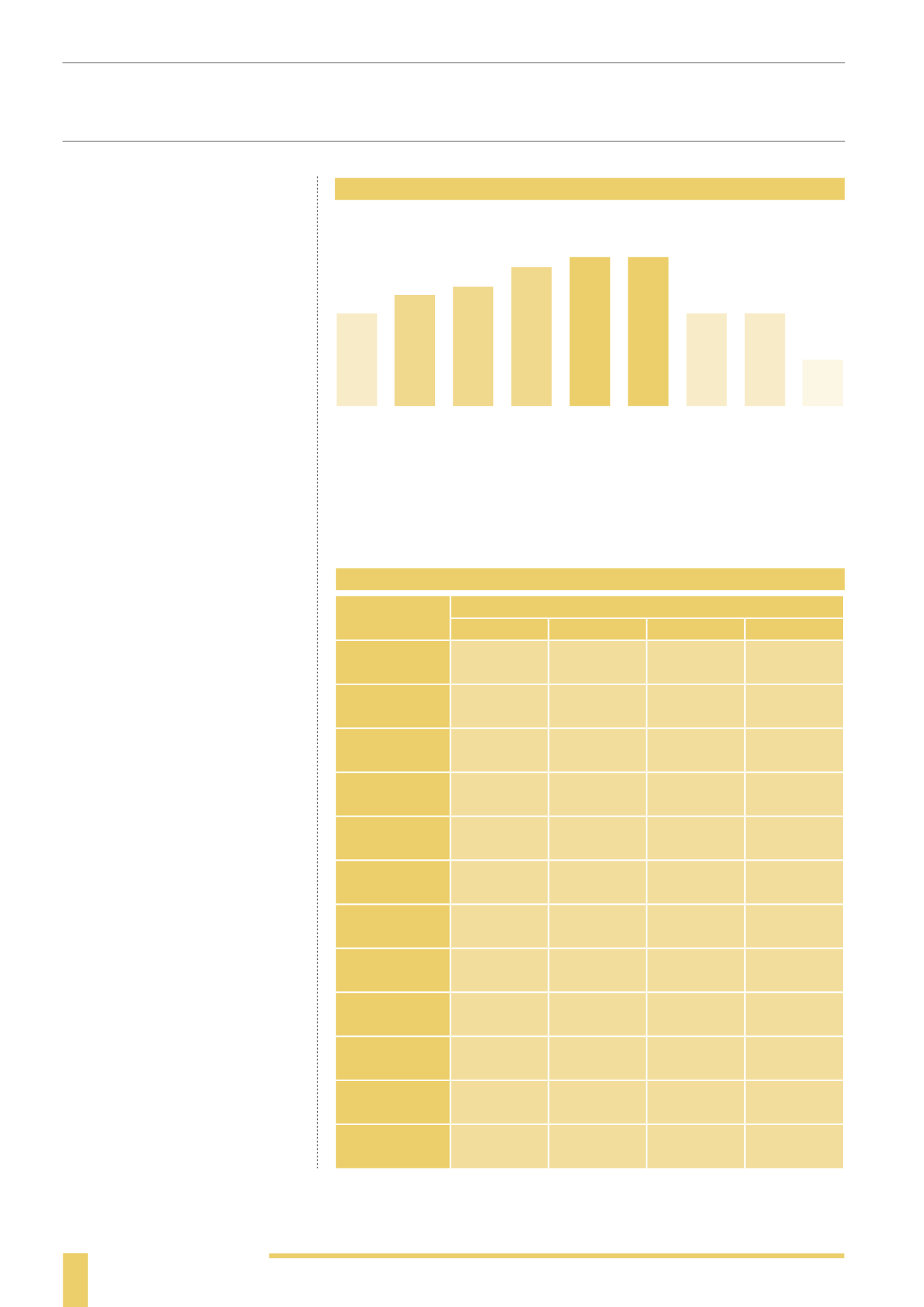

LIFETIME ALLOWANCE

(2006-2015)

ANNUAL GROWTH RATE REQUIRED TO FUND FOR £1.25m

EXISTING

FUND VALUE

TERM TO RETIREMENT

5 YEARS

10 YEARS

15 YEARS

20 YEARS

£100,000

65.72%

28.73%

18.34%

13.46%

£200,000

44.27%

20.11%

13.00%

9.60%

£300,000

33.03%

15.34%

9.98%

7.40%

£400,000

25.59%

12.07%

7.89%

5.86%

£500,000

20.11%

9.60%

6.30%

4.69%

£600,000

15.81%

7.62%

5.01%

3.74%

£700,000

12.30%

5.97%

3.94%

2.94%

£800,000

9.34%

4.56%

3.02%

2.26%

£900,000

6.79%

3.34%

2.21%

1.67%

£1,000,000

4.56%

2.26%

1.50%

1.12%

£1,100,000

2.59%

1.29%

0.86%

0.64%

£1,200,000

0.82%

0.41%

0.27%

0.20%

“Appetite to invest in VCTs has been strong recently as investors have sought attractive tax-free yields

in an environment of low returns for savers and limits on pension contributions for higher earners”

Mark Wignall, Mobeus Equity Partners

* Note that technically this allowance can be exceeded, but anything above the allowance will be subject to a hefty 55% tax charge.

Source: HM Revenue and Customs

The limit will be reduced even further to £1m in 2016/17, and then linked to the Consumer Price Index.

Interestingly, if the original £1.5 million had been linked to RPI, the limit would be approximately £2

million

Source: HM Revenue and Customs

2006/07

£1.5m

2007/08

£1.6m

2008/09

£1.65m

2009/010

£1.75m

2010/11

£1.8m

2011/12

£1.8m

2012/13

£1.5m

2013/14

£1.5m

2014/15

£1.25m