41 / 92

41 / 92

41

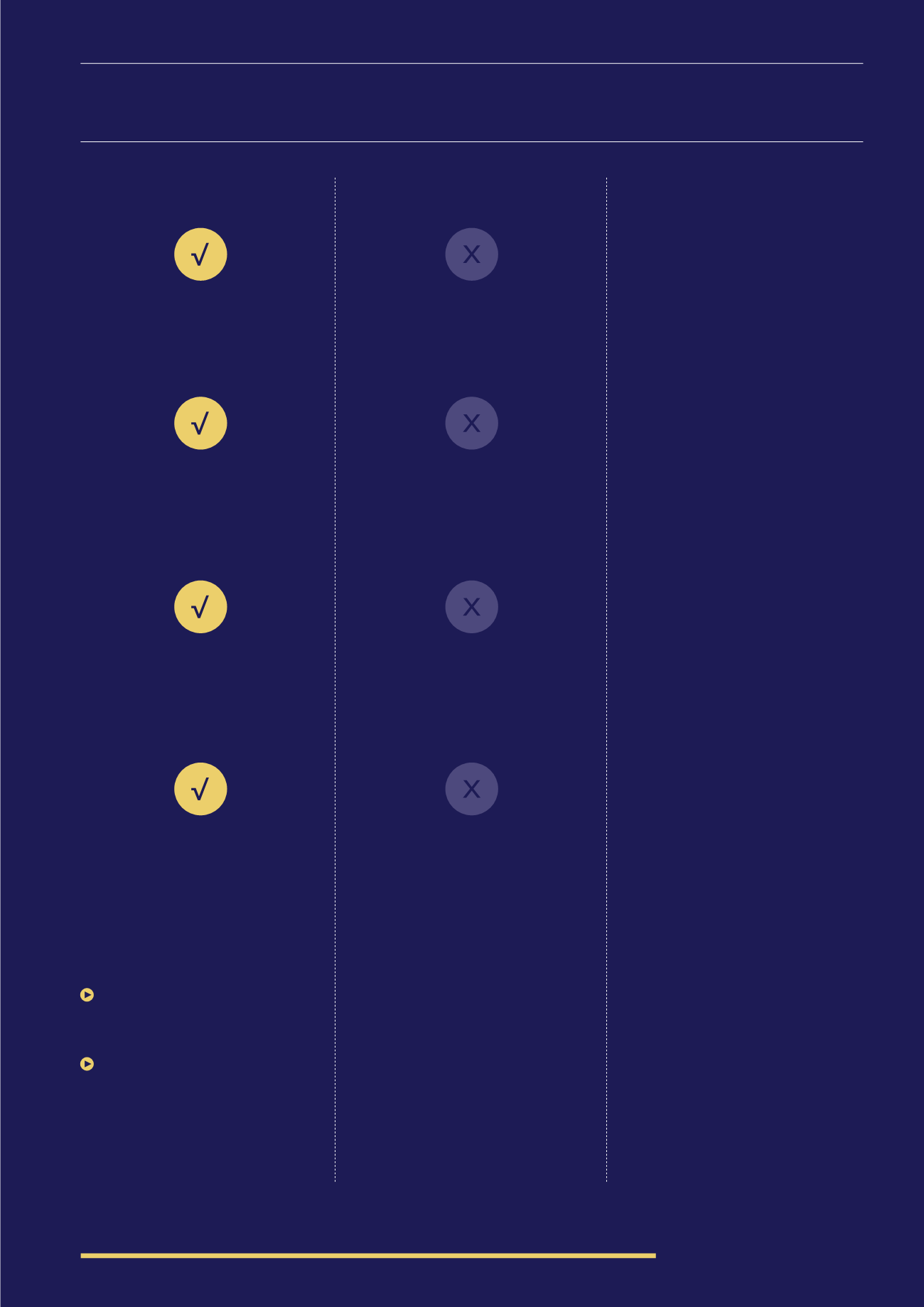

We think that this means that VCTs

should

be considered

for investors who are:

Finally, we can conclude that VCTs are

not

suitable

for:

And bearing in mind the likely

investment horizon and the higher risk

of VCTs, investors should be:

Prepared to hold their investment

for the long term (at least five years but

potentially much longer)

Comfortable with taking on a higher

level of risk than mainstream stock

market based investments

SUBJECT TO THE HIGHER (40%)

OR ADDITIONAL (45%) RATES OF

INCOME TAX

NON-TAXPAYERS (SINCE THE

INCOME TAX RELIEF AVAILABLE

ON NEW SHARE SUBSCRIPTIONS IS

AN IMPORTANT FEATURE)

THOSE WHO CANNOT STAY

INVESTED FOR A MINIMUM OF

FIVE YEARS (SINCE THEY WOULD

HAVE TO REPAY THE TAX RELIEF IF

SOLD EARLIER)

NOVICE INVESTORS

INVESTORS UNCOMFORTABLE

ABOUT TAKING A HIGHER LEVEL

OF RISK THAN MAINSTREAM

STOCK MARKET BASED

INVESTMENTS

ALREADY HOLDERS OF

PORTFOLIOS OF MAINSTREAM

INVESTMENTS, PROBABLY

WITHIN A PENSION

LIKELY TO BE ALREADY FULLY

UTILISING THEIR ANNUAL ISA

ALLOWANCE (£15,240 IN THE

2015/16 TAX YEAR)

CONTRIBUTING TO A PENSION

(IF WORKING)

“For the last 20 years, VCTs have provided financial advisers with an effective retirement

planning option for their clients”

Will Fraser-Allen, Albion Ventures

We’ve referred to “mainstream, stock

market based investments on the

left (and in several other places in the

report) because it gives us a reference

to compare VCTs to when it comes to

risk, but we admit this is a pretty vague

concept. Many stock market based

investments will be much more risky

than VCTs. We’re really using this term

as shorthand for the sorts of popular

equity based funds that invest in large

cap stocks in developed markets that will

form the backbone of most investors’

portfolios (and of course these funds

themselves are by no means risk-free).

And of course as higher risk investments

VCTs should only comprise a small

part of an investor’s’ total portfolio,

depending upon their attitude to risk

and level of wealth.

Much of this can be summed up in the

old adage “don’t let the tax tail wag

the investment dog”. Investors must

be comfortable with the risk they are

taking on, comfortable with the lack of

liquidity and they must have capacity

for loss before considering VCTs. The

tax reliefs don’t completely outweigh

these risks - they only make them more

tolerable. The point is that if investors

can tolerate these risks, there are

potentially big rewards for them if the

VCT performs well.

It’s also worth noting that FOS will closely

scrutinise the suitability of an investment

if they receive a complaint, even if the

tax was the primary basis for investing.

ACCUMULATION

Of course, as investments in smaller,

high-growth companies VCTs can form

part of an accumulation strategy. Tax-free

dividends and tax-free gains mean that, if

those dividends are reinvested, investors

are exposed to the compounding effect

tax-free. Compounding is the often the

key to a successful investment strategy

over the long term.

The impact of compounding tax-free

returns is quite startling: We used a

simplistic example, but if we assume a

yield of 6% (reinvested), annual growth