44 / 92

44 / 92

44

DECUMULATION

The new pension freedoms that came

in from April 2015 give people much

more flexibility when it comes to taking

their pension at retirement, and for

many VCTs could play a role in planning

for a retirement without purchasing

an annuity, and to ensure tax-efficient

decumulation.

SATELLITE PORTFOLIO

The simplest strategy to consider is

to have a satellite portfolio of VCTs

alongside the pension - in the previous

section this is what we were implying

could be an option for clients who are

at, or near to, maxing out their pension

limits. With upfront tax relief, tax-free

gains and tax-free income, VCTs have

some similar features to pensions when

it comes to tax-efficiency. Of course

they do not have the same flexibility

of investment as pensions and will

generally be invested in much higher

risk underlying assets, but as a rule

of thumb investors who are near to

maxing out their pension are more likely

to have the requisite capacity for loss,

sophistication and attitude to risk (of

course this is not a given though and

must be ascertained and evidenced by

the adviser).

A small satellite portfolio like this can

grow alongside a pension, or provide

a tax-free yield to supplement pension

income.

TAX-EFFICIENT STRATEGIES

FOR DECUMULATION

VCTs can also be used in a more

sophisticated way to provide tax-

efficient decumulation. We’ve included

some ideas on how this could be done

below and on the following page.

“With a sizeable net asset base and the right balance between generating capital growth from the underlying

investments, while successfully building a steady and increasing income stream from dividends: then you

can potentially have an interesting proposition”

Chris Hutchinson, Unicorn Asset Management

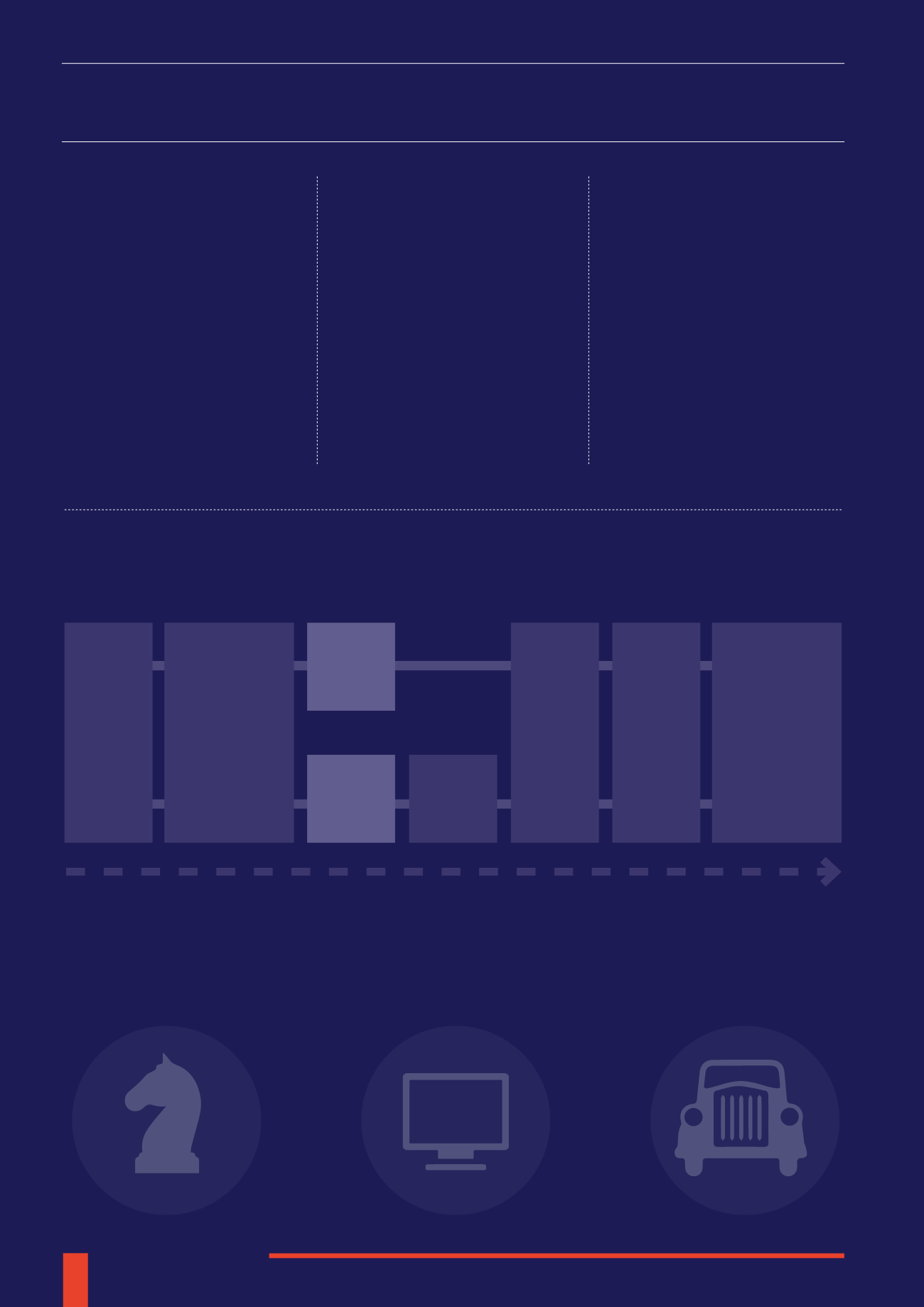

#1 CRYSTALLISING £100K

In the example below, the upfront Income Tax relief from the VCT investment is used to offset the tax payable on the funds that

have been crystallised (over and above the £25,000 tax-free lump sum).

This means that the net cost of withdrawing £100,000 from the pension pot is £9,000 instead of £30,000. Of course, this also means

that £70,000 of that £100,000 has to be invested for a minimum of five years. The example assumes the client is a higher rate

taxpayer is suitable for VCT investments and can afford to go without the income the £100,000 that is withdrawn from the pension

pot could provide.

£500

k

PENSION

POT

£100

k

CRYSTALLISE

£70

k

INTO

VCT

£21

k

TAX

RELIEF

£91

k

WITHDRAW

£100K AT A NET

COST OF 9%

£25

k

TAX-FREE

£75

k

TAXED

£45

k