45 / 92

45 / 92

45

#2 FLEXI ACCESS DRAWDOWN

In this example, the client is a higher rate taxpayer using flexi access drawdown and a combination of VCTs and Unit Trust

investments to invest their £500,000 pension pot in over a five year period. This is based on the assumption that the client doesn’t

need to spend the money in their pension pot over this time frame.

FUND SELECTION

The obvious place to start looking for distinguishing criteria is the fund’s investment objective and the sector it will be investing in.

The online comparison engine and review site MICAP define the objectives as either:

For the VCTs listed on their platform at the time of writing, they all fell into either: ‘Growth and Income’, ‘Capital Preservation’ and

‘Growth and Income’ or ‘Capital Preservation and Income’ categories.

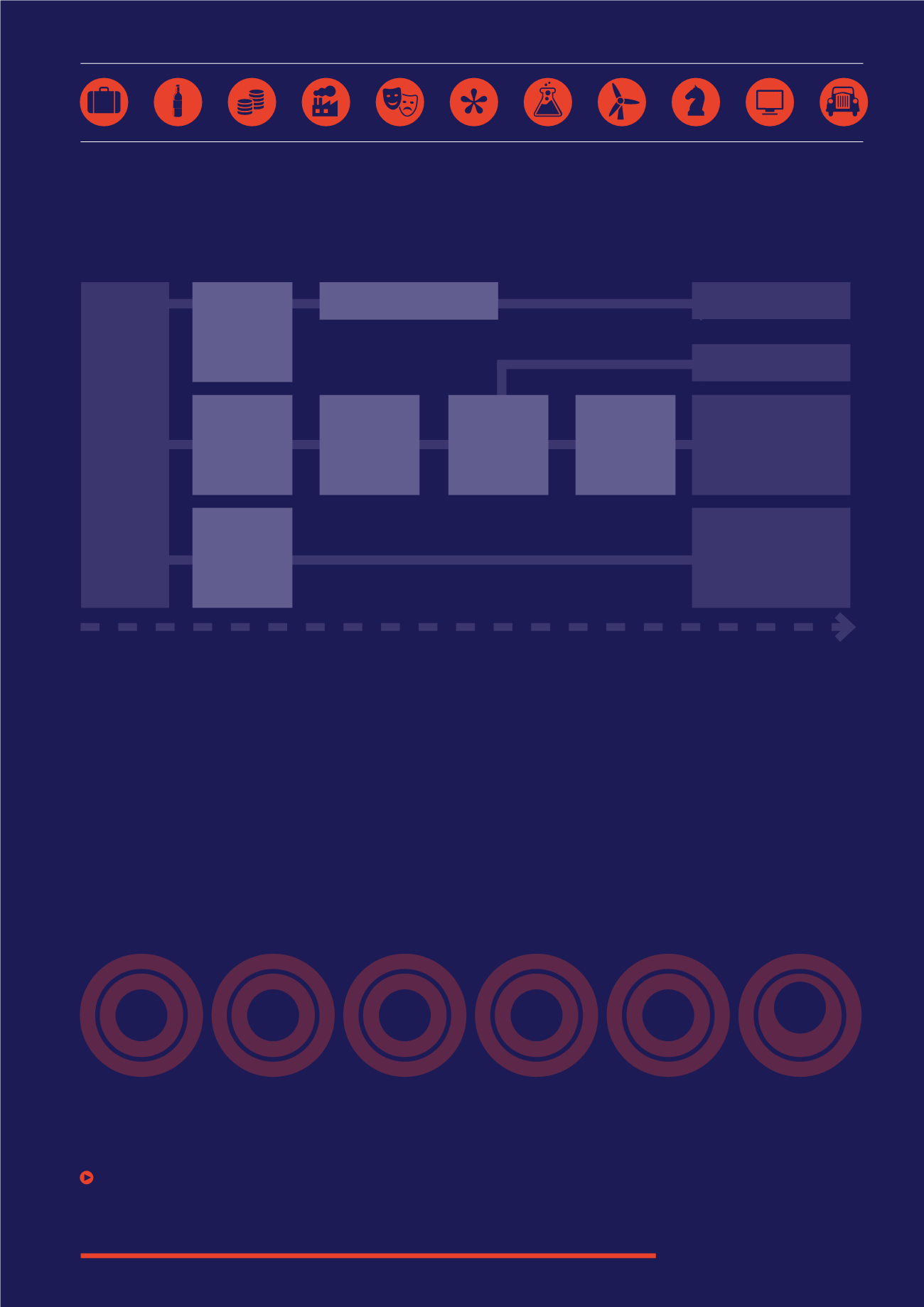

The 25% tax-free pension commencement lump sum is taken out in year one and invested in a Unit Trust portfolio, and £83,000 is

drawn down from the pension in each of the five years, taxed at the marginal rate of 40% and then the net amount is invested into a

VCT portfolio.

Assuming that both the Unit Trust portfolio and the pension pot grows at approximately 6% per annum, and that the VCTs do not

grow at all, after five years the pension pot will be exhausted, but the sum of the Unit Trust portfolio, VCT portfolio and tax relief will

be approximately £492,000.

A simpler idea would be to assume 0% growth in any of the assets. £125,000 would be taken tax free. £75,000 would be drawndown

from the remainder each year and (assuming 40% tax) the net amount of £45,000 could be invested in VCTs, providing £13,500 of

tax relief. After five years, the pension pot would be exhausted, but there would be a VCT portfolio of £225,000 paying dividends

and an additional pot of £67,500 received in tax relief.

MICAP also lists the sector and sub sector the VCT will be investing in: Financial Services, Food and Drink, General Enterprise,

Industry and Infrastructure, Media and Entertainment, Multi Sector, Pharmaceuticals/Biotechnology, Renewable Energy, Sport and

Leisure, Technology, and Transport.

£500

k

PENSION

POT

£125

k

TAX-FREE

@6%

UT GROWTH

£83

k

TAXED

£50

k

INTO VCT

£15

k

TAX RELIEF

£83

k

DRAWDOWN

ANNUALLY

£375

k

GROW @6%

PENSION

EXHAUSTED

£75

k

TAX RELIEF

£167

k

UT

£250

k

VCT

After 5 years

CAPITAL

PRESERVATION

CAPITAL

PRESERVATION

& GROWTH

CAPITAL

PRESERVATION

& INCOME

GROWTH

GROWTH

& INCOME

SUPER

GROWTH