35 / 92

35 / 92

35

of inflows - perhaps another reason to

favour closed-ended funds over OEICs,

as inflows drive the share price up, but

a good manager can still keep control

of the amount of funds they raise for

investment.)

The ideal is for managers to match their

fundraising to their anticipated deal

flow, and we think that the majority

do this quite well. There are rarely

unusually big spikes in funds raised,

and managers are generally happy to

explain them when they occur.

CASH MANAGEMENT, CASH

DRAG (AND MORE ON THE

DISCOUNT)

Unlike open-ended funds, VCTs are

not obliged to pay all of their profits

out to investors. This is actually a very

big advantage, as cash can be retained

and then used to smooth out dividend

payments, even in a falling market. So

VCTs can pay out dividends tax-free and

(if they manage their cash position well)

continue to pay those same dividends

even in times of market distress - many

established VCTs maintained their

dividend throughout the downturn

in 2008. This is a very appealing

proposition.

Holding onto cash has its downsides

though, as the low return on cash can

reduce the overall performance of the

VCT (“cash drag”). Analytics sites, such

as Morningstar, Trustnet for the AIC, can

be used to check the cash position of

individual funds (as can the funds’ own

documentation).

As of August 2015, the average net cash

position of both Generalist and AIMVCTs

was 13%, but this hides huge variations -

VCTs at different stages of their life will hold

very different amounts of cash.

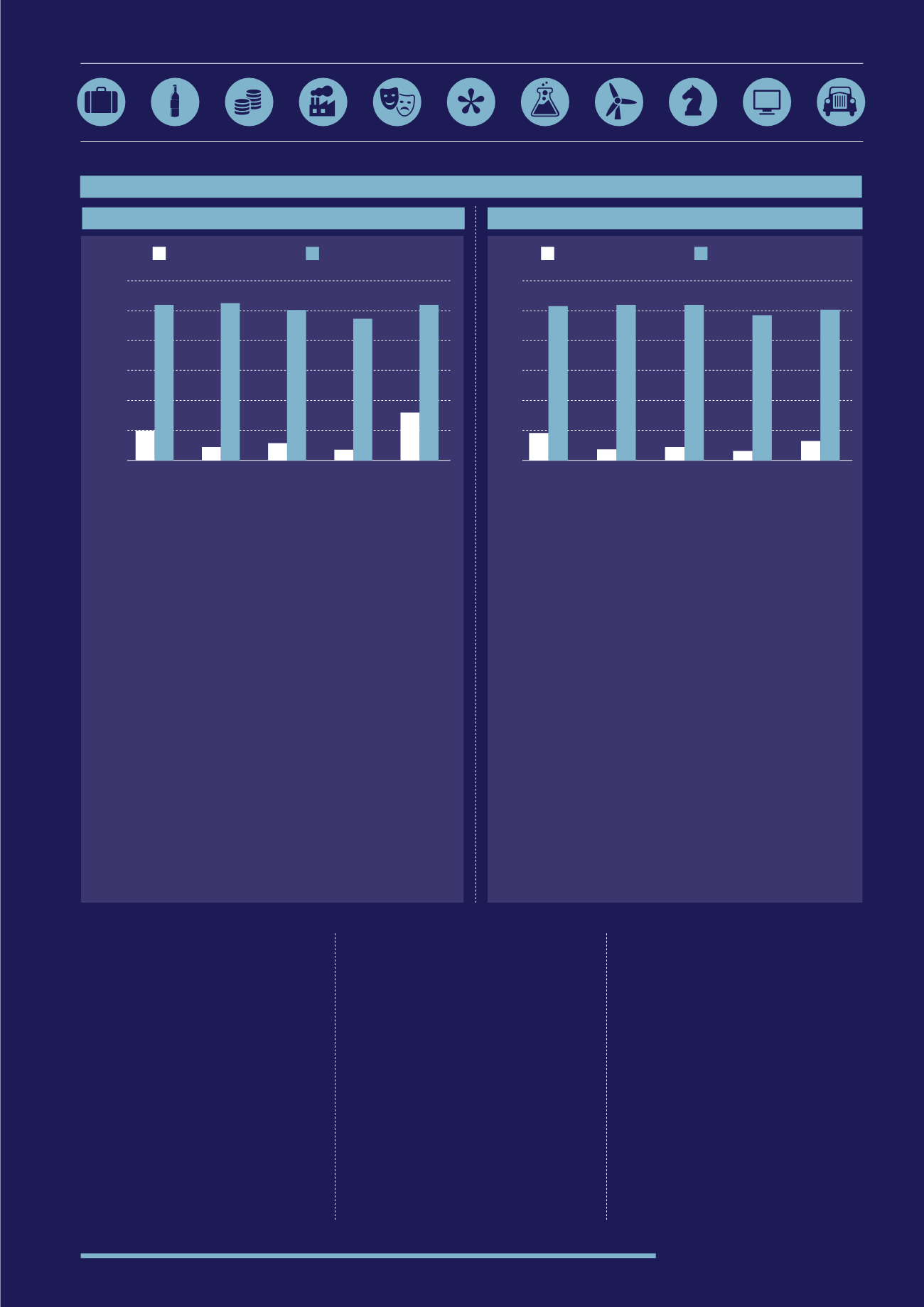

MEASURING VOLATILITY

The average share price is a good heuristic for expected

return, but does not show what the variance has been. The

standard deviation of the returns gives a better indication

of the volatility of the total share price returns. On average,

the Generalist sector has had the highest returns over the

period with fairly low volatility. We can also see the standard

deviations for AIM Quoted and Technology sector has been

extremely volatile. Media, Leisure & Events Specialists VCTs

have the lowest variance in share price. Many of these

companies may have more predictable returns but the ability

to generate higher returns is likely to be more difficult with

these companies.

NAV total return is also worth examining, as NAV total

return shows performance which isn’t affected by

movements in discounts and premiums, and also takes

into account that different VCTs pay out different levels

of dividends. Volatility for all of the sectors is much lower

when looking at the NAV return, and the average return is

very similar to the share price.

The NAV total return assumes the average weighted, by the

starting shareholder funds of each company, performance

on a theoretical £100 assuming any net income was

reinvested. The chart shows that environmental VCTs offer

a similar average NAV total return than VCT generalist

but just as with the share price total return, the standard

deviation for specialists is higher. On the other hand, it

is worth noting that the AIM VCTs sector has the highest

standard deviation for the NAV total returns.

1 YEAR TOTAL SHARE PRICE RETURNS

1 YEAR NET ASSET VALUE TOTAL RETURN

Source: AIC and Morningstar

Source: AIC and Morningstar

Standard deviation

Average

Standard deviation

Average

VCT

Specialist

environ.

VCT

Specialist

media, leisure

& events

VCT

Specialist

technology

VCT

Generalist

VCT AIM

Quoted

120

100

80

60

40

20

0

20.48

9.60

11.79

7.31

103.79

105.27

100.64

94.39

103.28

32.23

Jan 07 -

Oct 15

Jan 07 -

Oct 15

Apr 10 -

Oct 15

Apr 09 -

Oct 15

Jan 07 -

Oct 15

VCT

Specialist

environ.

VCT

Specialist

media, leisure

& events

VCT

Specialist

technology

VCT

Generalist

VCT AIM

Quoted

120

100

80

60

40

20

0

103.45

17.48

6.54

7.99

4.98

11.86

104.31

104.66

97.55

100.72

Jan 07 -

Sept 15

Jan 07 -

Sept 15

Apr 10 -

Sept 15

Apr 09 -

Sept 15

Jan 05 -

Sept 15