36 / 92

36 / 92

36

And as we noted earlier, advisers should

be clear on how and where VCTs invest

their cash and near cash.

There’s also another point about the

discount to the NAV. If a fund used its

cash to maintain the discount at an

acceptable level (say, 5%) that would

make it very hard to identify a run of

redemptions on the fund. We think (but

we can’t evidence this at the moment)

that would mean that the discount

would fall very steeply once the fund

suspended its buyback policy. Again,

this point is not a showstopper, but

it’s another reason to be clear that the

investment must be made for the long

term, and should be considered an

illiquid investment.

PORTFOLIO VOLATILITY

Of course the portfolio will experience

some volatility. Volatility in the share

price will be driven by supply and

demand for the shares. Volatility in

the NAV will be driven by acquisitions,

realisations and the timing of valuations.

Therefore both the share price and

the NAV can be quite erratic. It’s worth

considering this, if only for a moment:

VCTs are subject to two sources of

volatility.

AIM quoted VCTs can be very volatile,

and at least some of that volatility will

simply be a reflection of the volatility on

the AIMmarket itself. Generalist VCTs

tend to be less volatile as their underlying

investments are valued less frequently.

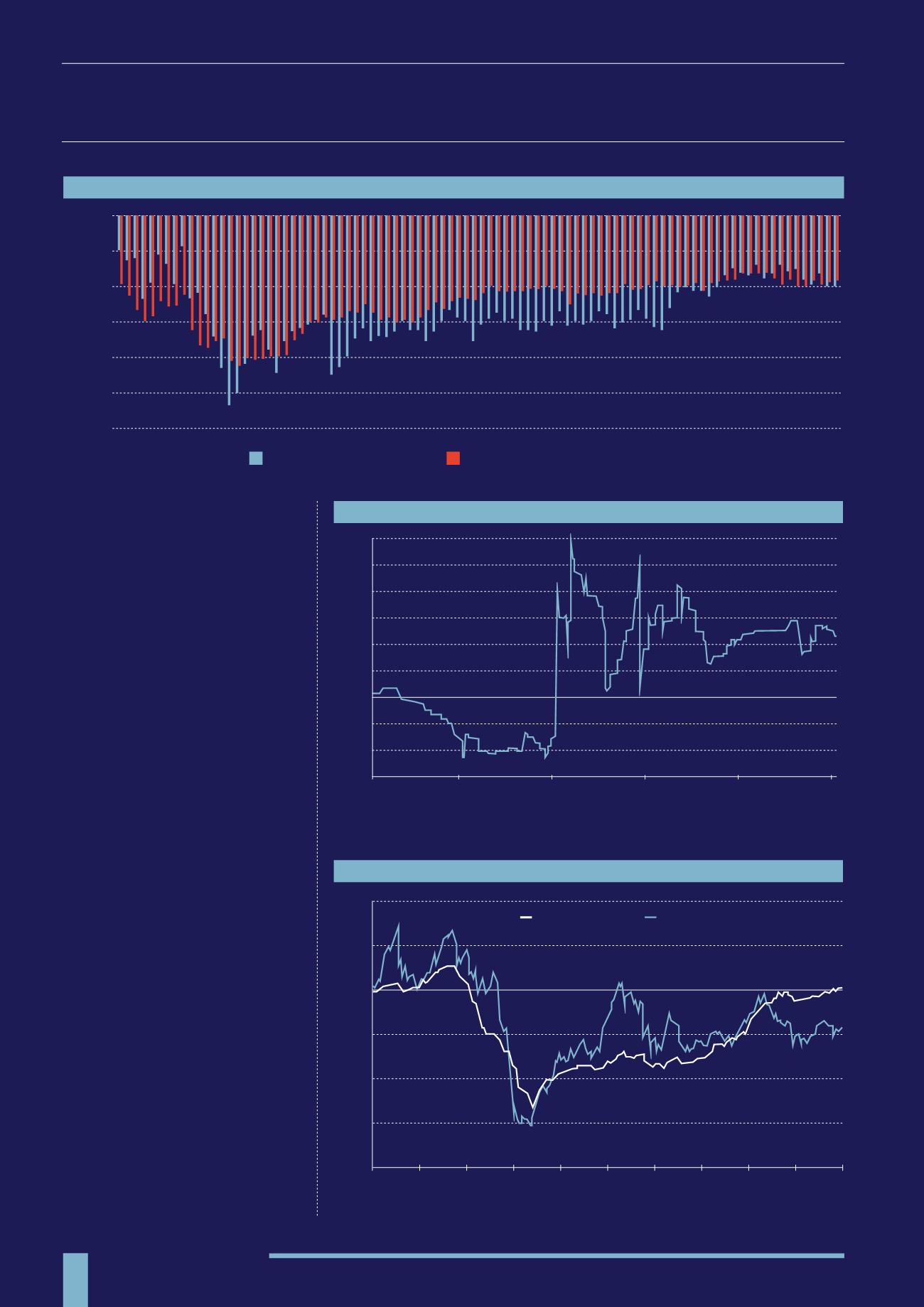

AVERAGE DISCOUNT TO NAV

(2008- 2015)

PORTFOLIO VOLATILITY

(2010 - 2015)

AIM VS. AIM QUOTED VCTs

(11/2005 - 11/2015)

Source: FE Analytics

“A good Generalist VCT looks for companies that thrive in industries undergoing fundamental

change - often driven by new technology or consumer behaviour”

Shane Elliot, Beringea LLP

AIM Quoted VCT Sector mirrors the volatility on AIM itself

VCT AIM Quoted

AIM

Source: Morningstar and the AIC

Source: FE Analytics

This is a Specialist VCT investing in a high risk sector

0

-5%

-10%

-15%

-20%

-25%

-30%

VCT AIM Discount Average

VCT Generalist Discount Average

60%

50%

40%

30%

20%

10%

0%

-10%

-20%

-30%

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

40%

-40%

-60%

-80%

Nov 05 Nov 06 Nov 07 Nov 08 Nov 09 Nov 10 Nov 11 Nov 12 Nov 13 Nov 14 Nov 15

20%

-20%

0%