38 / 92

38 / 92

38

FOCUS ON LIMITED LIFE

VCTS

One of the most interesting ways of

returning capital to investors is by

winding-up the VCT itself. The VCTs

assets are liquidated and the capital

and income are distributed to the

investors. This is the basis of Limited

Life (sometimes known as Planned Exit)

VCTs.

They follow a low risk investment

strategy backing companies with

favourable characteristics:

Substantial assets

Experienced management

Secure or contracted revenue

streams

Clear exit

Often Limited Life VCTs will invest in

loan notes, taking a first charge over the

assets and/or revenue streams, as well

as investing equity. Essentially, they are

looking for secure and predictable asset

backed revenues. The potential returns

are lower, but the risks to investors

should be lower too. When the VCT

comes to the end of a predefined term

(never less than five years, to ensure

investors secure their Income Tax

relief) the board will propose a special

resolution for the shareholders (the

investors in the VCT of course) to vote

on process of winding-up the VCT. This

can be an efficient way of returning

capital to investors, without relying

upon the secondary market and having

to grapple with the issue of shares

trading at a discount to the NAV.

DISTRIBUTIONS FROM CASH

OF RESERVES

We’ve already discussed the ability of

a VCT to use its cash reserves to pay

dividends - and thus “smooth” them

out over time - as a positive feature.

However, VCTs do use this feature to

pay dividends out of the funds they

have raised rather than out of their

investment profits: essentially returning

investors’ capital to them (tax-free). The

government looked into this to see if

this was being exploited, but found that

“Limited Life VCTs will typically offer investors an opportunity to vote on winding up the VCT

after the fifth anniversary, which means not having to worry about selling their shares in the

VCT on the secondary market”

Eliot Kaye, Puma Investments

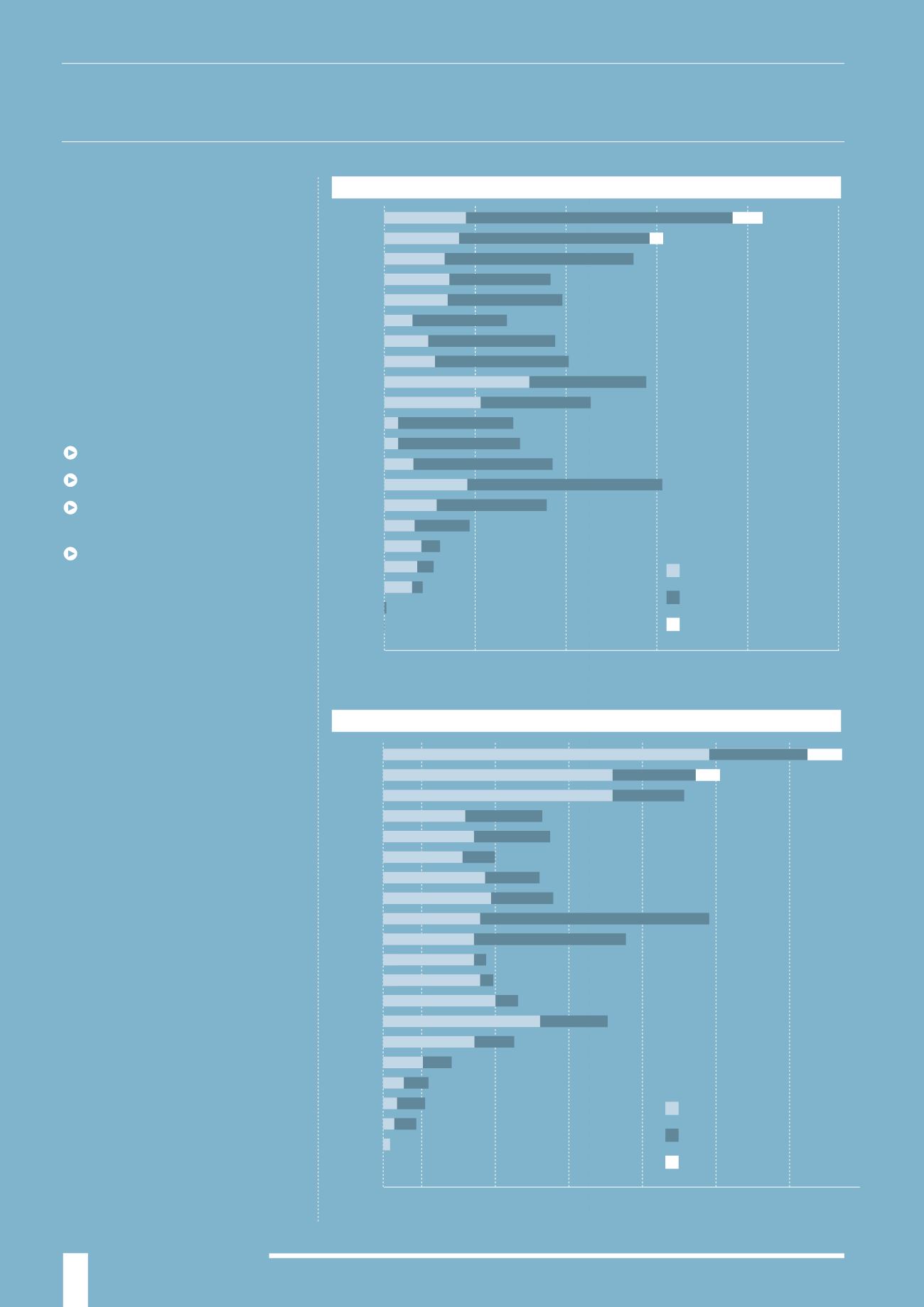

UPFRONT COSTS TO THE TAXPAYER

(1993-2015)

Source: HMRC (2015)

EIS Tax Relief Cost

VCT Tax Relief Cost

SEIS Tax Relief Cost

2013-14

2012-13

2011-12

2010-11

2009-10

2008-09

2007-08

2006-07

2005-06

2004-05

2003-04

2002-03

2001-02

2000-01

1999-00

1998-99

1997-98

1996-97

1995-96

1994-95

1993-94

0 50

150

350

250

450

550

436.98

309.69

309.45

109.76

124.54

103.54

141.46

146.5

129.52

121.28

125.44

133.46

152.18

213.04

122.74

58.8

22.7

18.8

10.6

38

34

32

28

0.78

33

54

90

31

14

14

208

312

81

69

45

102

105

97.5

120

25.77

132

49.05

FUNDRAISING BY VENTURE CAPITAL SCHEMES

(1993-2015)

Source: HMRC (2015)

2013-14

2012-13

2011-12

2010-11

2009-10

2008-09

2007-08

2006-07

2005-06

2004-05

2003-04

2002-03

2001-02

2000-01

1999-00

1998-99

1997-98

1996-97

1995-96

1994-95

1993-94

0

500

1000

1500

2000

2500

Total VCT funds raised

Total EIS funds raised

Total SEIS funds raised

440

400

325

350

340

150

230

270

780

520

627.2

667.3

760.9

1065.2

450

270

165

190

170

160

113.4

94.3

52.9

14

9

294

613.7

70

70

155

606.4

647.6

707.3

732.5

517.7

622.7

548.8

1031.5

1032.3

85.9

1456.6

163.5

Funds raised (£millions)

Cost of Tax Relief (£millions)