34 / 92

34 / 92

34

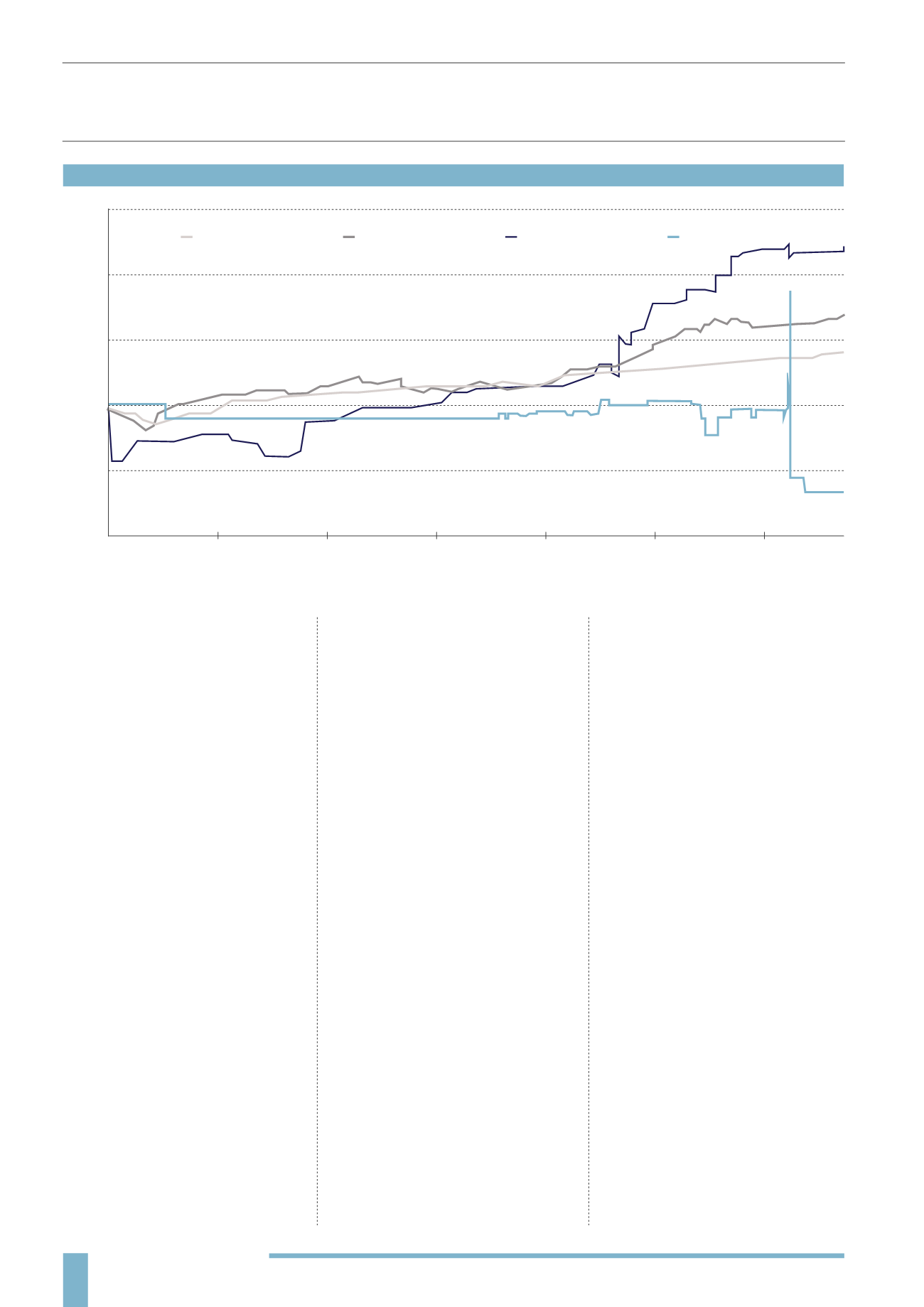

And by adding in just two individual

funds, we can see that the sector

averages mask a wide range of

performance from their constituents

(and a high degree of volatility in some

funds).

Now, we suspect that none of this

will be new news for many readers,

and it’s certainly not really any

different from examining mainstream

fund performance. Indices are not

representative of individual fund

performance, managers can have

good spells followed by lean spells

and performance can look stunning

or average depending upon the

measurement period. Funds need to

be judged on their own merits, in the

context of their stated objectives, asset

class and risk profile. But we do think

that there are two key issues that merit

extra attention when it comes to VCTs.

One is the importance of income to the

returns achieved. The other is (again) the

issue of the NAV versus the share price.

Not only is the NAV frequently higher

than the share price, but it is also a

much more opaque measure. This is

really something to be queried in due

diligence. Who calculates the NAV, how

often do they do it and how independent

are they?

The NAV is of course dependent

upon the valuation of the underlying

investee companies, so the accuracy

of these valuations needs to be taken

into account. Established valuation

guidelines are followed by VCT

managers, but within these there is

room for interpretation - small, unlisted

companies are hard to value and so

there is an element of human judgement

in the process. The timing and frequency

of valuations can have an impact, and

the actual realisation obtained for an

investment may differ materially from a

valuation, depending on the motives of

the buyer and the VCT manager.

This is, of course, much more of an issue

for Generalist VCTs and much less of an

issue for AIM VCTs, where the valuation

of the underlying holdings is down to the

raw market forces shaping AIM.

Lower levels of transparency are

something that goes with the territory

when investing in smaller companies

and this is one of the reasons why VCTs

are considered high risk. It requires an

awareness that performance is harder

to measure, and that it can then be hard

to realise the value of that performance

(liquidity again). This is another area

where the active VCT manager hopefully

earns their money - by establishing and

maintaining genuine valuations for the

underlying firms, and therefore providing

a transparent way to invest in a less

transparent market for their investors.

PORTFOLIO MANAGEMENT

AND PORTFOLIO RISKS

There are a couple of issues around

the construction and running of VCT

portfolios that are worth examining, as

they can impact upon the performance,

liquidity and risk of the investment.

DEAL FLOW AND

FUNDRAISING

This is a problem across the fund

management sector - paid a percentage

of Assets Under Management (AUM),

funds can be tempted to operate as

asset gatherers rather than asset

managers. Having raised more cash than

they have the capability or deal flow to

deploy, fund managers might be rushed

into making poor quality deals. This

links to the point about transparency we

made above. It would be very difficult to

identify early on if bad deals were being

made - not because of some subterfuge

on the part of the manager, but simply

because of the nature of investing in

unquoted equity. (And we note that

past performance is the biggest driver

“A lot of clients and some financial advisers do not understand that VCTs are based on a private

equity and venture capital operation, where a balance must be struck between having cash

available and being able to actually deploy it”

Mark Wignall, Mobeus Equity Partners

VCT SECTOR PERFORMANCE

(2008-2015)

Source: FE Analytics

Performance over the five years to August 2015 (rebased, income reinvested)

Dec 08

150%

100%

50%

0%

-50%

-100%

Dec 09

Dec 10

Dec 11

Dec 12

Dec 13

Dec 14

VCT AIM Quoted

VCT Generalist

Fund C

Fund D