30 / 92

30 / 92

30

DEPTH AND DETAIL

How do these risks and benefits interact, how do the managers try to mitigate the issues they face, what are some of the additional,

existential risks, what are some of the unique considerations that advisers and investors need to keep in mind?

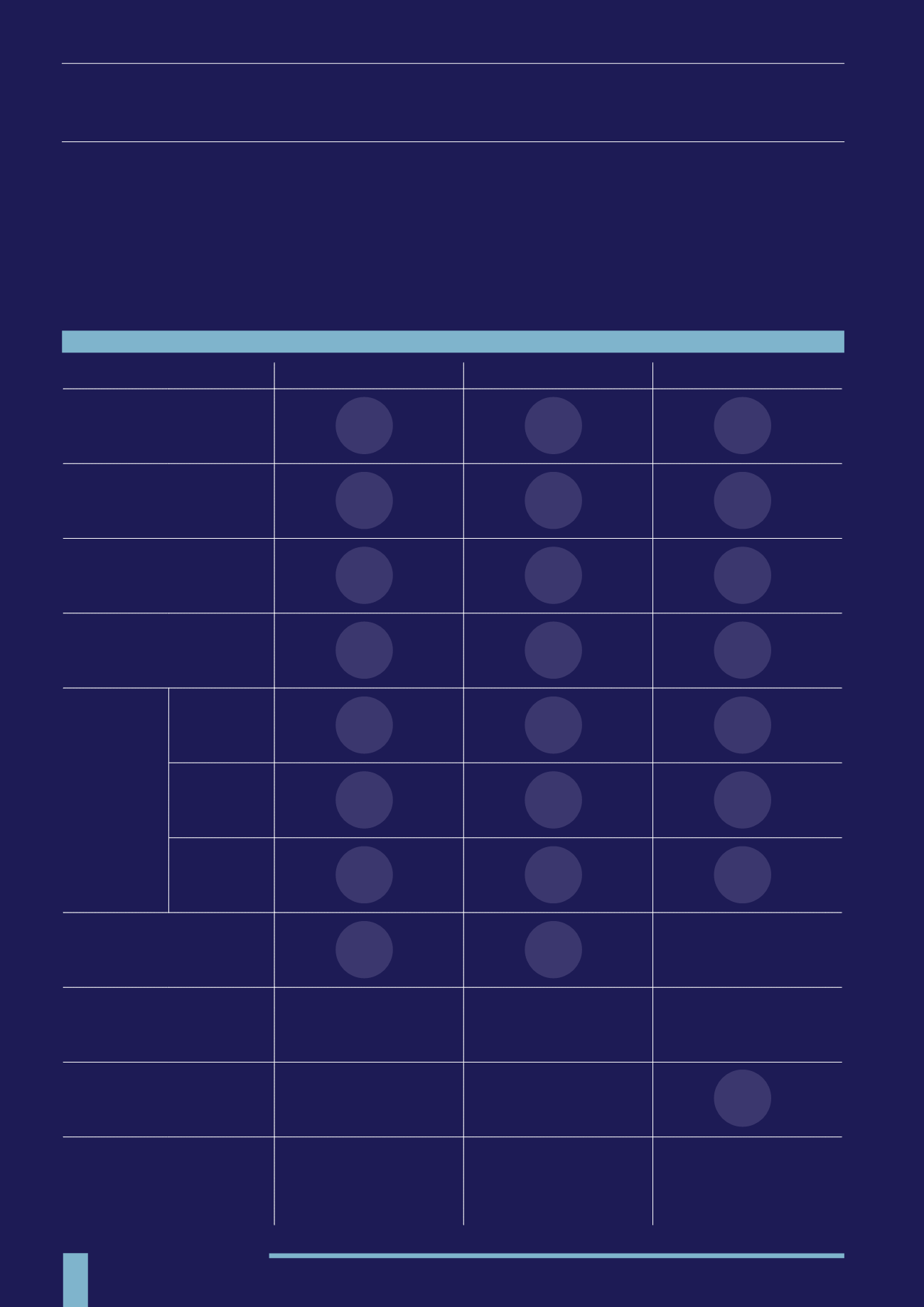

LEGISLATIVE CHANGES

This section has been promoted to give it more prominence after the July Budget. The VCT sector has always been subject to rule changes

as the Treasury has tweaked the scheme to ensure that it represents value for money for the UK taxpayer (see Policy Changes Timeline on

page 88 for a full list of the changes since inception), but perhaps the most sweeping changes to qualifying companies were announced

this year in order to comply with European State Aid rules. These changes represent significant upheaval for some VCT managers.

PRE-MARCH 2015

BUDGET 2015

SUMMER BUDGET

AGE LIMIT

No limit

12 years*

7 years*

LIFETIME CAP

No limit

£15m

£12m

ANNUAL

INVESTMENT LIMIT

£5m

£5m

£5m

EMPLOYEE LIMIT (FTE)

250

250

250

KNOWLEDGE

INTENSIVE

COMPANIES

LIFETIME

CAP

No limit

£20m

£20m

EMPLOYEE

LIMIT

250

500

500

AGE LIMIT

No limit

12 years

10 years*

USE OF EIS & VCT MONEY

FOR ACQUISITIONS OF

BUSINESS

Allowed

Allowed

New rules to prevent EIS and

VCT funds being used to acquire

existing businesses

GROWTH &

DEVELOPMENT

No requirement

Require that all investments are

made with the intention to grow

and develop a business

Require that all investments are

made with the intention to grow

and develop a business

SEIS MONEY

70% of SEIS money be

deployed before raising EIS

70% limit removed

No limit

EXISTING

SHAREHOLDERS

No restriction

For EIS only, a requirement that

investors are independent from

the company at the time of

the first share issue (excluding

founder shares)

For EIS only, a requirement that

investors are independent from

the company at the time of

the first share issue (excluding

founder shares)

*Unless total investment represents more than 50 per cent of the company’s turnover over the preceding five years

OUTLINE OF THE CHANGES PROPOSED IN 2015