28 / 92

28 / 92

28

Holdings on AIM do have more liquidity

in theory, but in practice volumes in

certain shares can be thin, spreads

can be wide and disposing of a large

investment could be problematic.

However, for patient buy and hold

investors these issues do not impact

VCTs very often. AIM shares also value

daily and do not have long closed

accounting periods, so striking the NAV

and facilitating buybacks is much easier

for AIM VCTs.

In general we would suggest that AIM

should be considered more liquid, but

some VCT managers make investments

in unquoted firms with a very definite

plan for exiting them and - providing the

business can deliver on the plan - some

commentators consider that these

kinds of investment are actually more

liquid than AIM.

The point about the business delivering

on the plan is important. In unquoted

businesses it is important that the

management has a desire and drive to

sell and eventually exit. A complacent

management might sit tight, happy to

run a reasonably successful business,

and leave their investors in limbo. This

is another area where the VCT manager

should be adding value by careful

vetting of the management team and

maintaining ongoing monitoring and

involvement. Its also important that the

VCT manager strikes a good deal with

the investee that keeps them motivated,

rather than simply trying to wring as

much out of the deal as possible. It’s vital

to interrogate the manager’s investment

and due diligence process and get a feel

for the house philosophy. More on due

diligence on VCTs on page 49.

These risks won’t impact VCT investors

directly, but they will impact the

ultimate performance of the VCT, and

they would constrain the manager’s

ability to close out losing positions -

investors have to be prepared to hang

on and ride out a downturn in the

“AIM based VCTs typically have a more diversified portfolio than other types of VCT, likely to be

invested in larger more established companies, with transparent market pricing and reasonable

liquidity”

Dr Paul Jourdan, Amati Global Investors

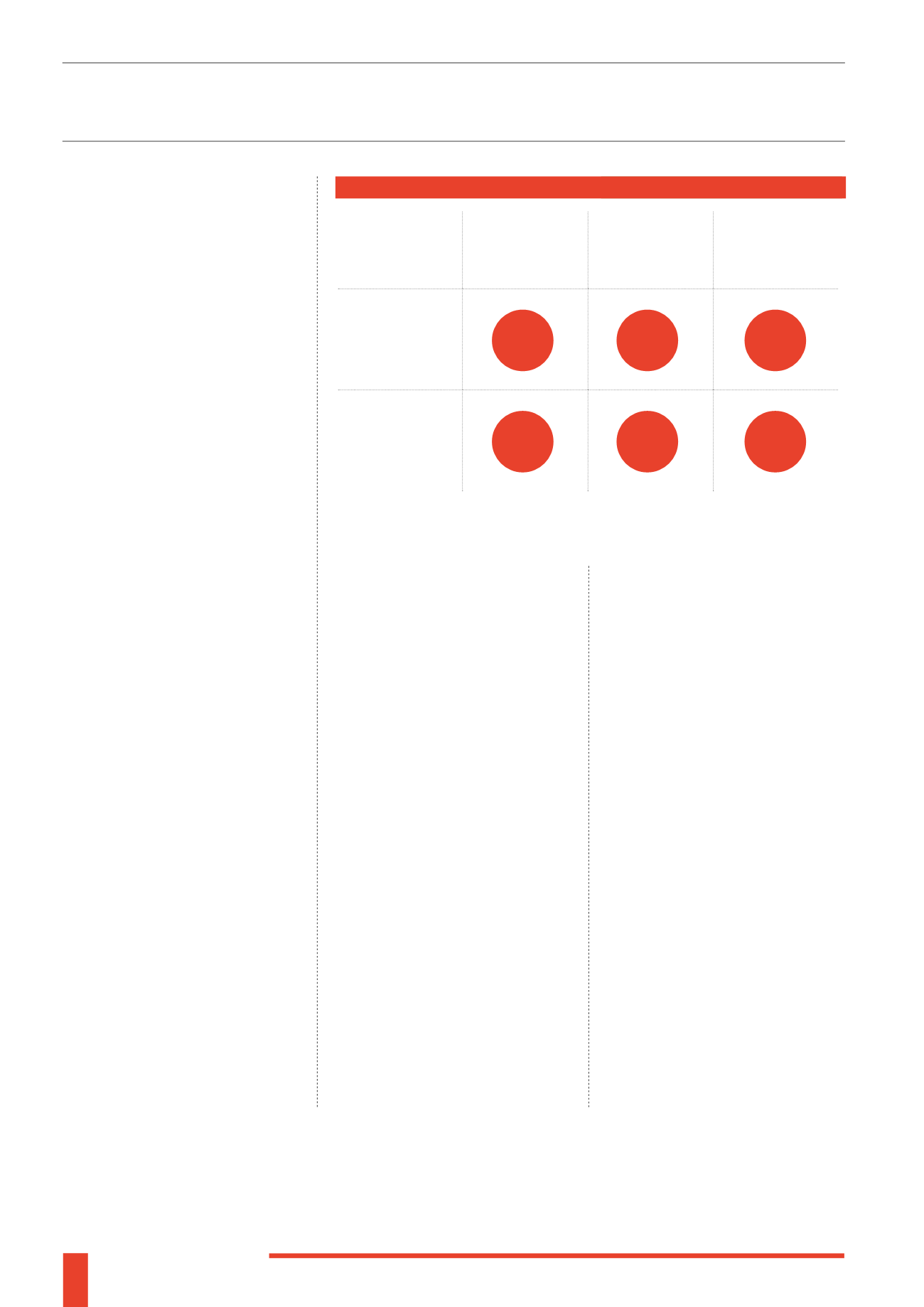

VCT DISCOUNTS / PREMIUM: 12 MONTHS TO AUG 2015

DISCOUNT

ONE YEAR

HIGH %

DISCOUNT

ONE YEAR

LOW %

DISCOUNT

ONE YEAR

AVERAGE %

VCT AIM

QUOTED

-4.1

-12.5

-8.3

VCT

GENERALIST

0.8

-17.5

-9.1

market or the wider economy without

expecting the investment manager

to re-weight the portfolio into more

defensive assets.

LIQUIDITY OF THE VCT

As noted above, the biggest liquidity

risk to investors is really the prospect of

a discount to the NAV, and sometimes

this can be quite large. Because the

share price is driven by demand for

the shares, this can be quite severe in

times of market distress. VCT providers

attempt to address this by operating

‘buyback’ policies. These are promises

to buy the shares back at a certain level

- say a 5% discount to the NAV. On the

face of it this solves the problem (a 5%

discount after 30% Income Tax relief is

probably going to feel acceptable) but

the strength of the promise needs to

be examined - wording such as “we will

endeavour” might not be worth much

when everything is nose-diving. The

VCT board can only agree to buy shares

back for as long as they have the cash

to do so and it is not detrimental to the

remaining investors. Investors must be

clear that they probably won’t be able to

exit at anything like the NAV if there is a

panic. This shouldn’t be a showstopper

though – it’s really true of any stock

market based investment.

At the time of writing (November 2015),

the VCT Generalist sector was at an 8%

discount to the NAV and the VCT AIM

sector was at a 7.9% discount in the

secondary market (note - these figures

do not apply to buybacks where the VCT

purchases shares back from investors at

a smaller discount, as described above).

It’s also worth remembering that this

lack of liquidity can be an advantage for

the fund manager. Worried investors

who run for the exits can be absorbed

by the discount and the manager is

not forced to sell assets at low prices

to meet redemption requests. This

seems fair - why should investors

who are prepared to stay the course

be penalised by those who lose their

nerve?

Investors need to be aware of that most VCTs will trade at a discount to their NAV

Source: Morningstar (August 2015)