25 / 92

25 / 92

25

THE INVESTMENT CASE

There’s a multi-faceted investment

case for VCTs - as there is with most

investments. Of course the tax benefits

are very attractive and provide a great

incentive for investment, but the old

adage that the “tax tail should not

wag the investment dog” applies here

- the investment has to make sense

in its own terms and not just as a tax

planning exercise. With this thought

in mind, we’re going to leave the tax

reliefs to the end and look at the other

aspects of the investment case first.

SMALLER COMPANY

INVESTING

There’s a good case for investing in the

kinds of smaller companies that are

VCT qualifying (new shares of privately

owned or AIM listed companies with

fewer than 250 full-time equivalent

(FTE) employees and gross assets of

no more than £15 million). It’s smaller

companies that go on to be the giants

of tomorrow, and depending upon

where we are in the business cycle, they

can offer a lot more value than bigger

companies. They are less researched

than larger listed firms, so there is more

opportunity for investment managers

to identify bargains and find ways in

which they can help to grow business.

So the first point in favour of

smaller company investing is the

opportunity to identify the kind of

value that is much harder to find (or

some might say impossible to find)

in the mainstream market today.

As the businesses grow, the VCT might

seek to exit, either through a trade sale

or listing, realising the value of their

investment. For example, over the

last three years (to August 2015) AIM

VCTs have generated a total return of

26%, excluding income. Over a similar

period, the AIM index returned around

7%. However, price performance is

patchy with wide distributions, so we’ll

look at this in more detail on page 33.

But not all VCTs are just looking

for profitable exits. Many VCTs are

focused on generating income for their

investors. The average VCT yield at

the time of writing is 8.5% (although

of course as with all averages that

44%

35%

3%

7%

11%

number hides a huge amount of

variation, ranging from zero to the

high twenties). Often these yields are

achieved by Generalist or Limited Life

VCTs providing loan notes to larger

companies, securing healthy income

streams, or investing in established

firms with regular distributions of

profits. It’s also worth noting that while

VCTs’ share prices will correlate with the

markets, very often their underlying NAV

and ability to generate income is not.

As we see when we examine the

investment performance information

on VCTs, the income is the major

component of the total return for

many of them. Selecting a high

yielding VCT and then reinvesting the

income appears to be the best way of

maximising the return (consider that

the income is not taxed).

So another reason to invest in smaller

companies is to capture yields that

would be difficult to find elsewhere -

with interest rates set so low, bonds

and other fixed income investments

are much less attractive than in a

normal environment, and high yielding

mainstream large cap equities are also

considered to be overvalued by some

measures.

The final reason to invest in smaller

companies is less about investment

returns and more closely connected to

the impact on the investee companies

we were talking about in the

VCTs in Focus

section.

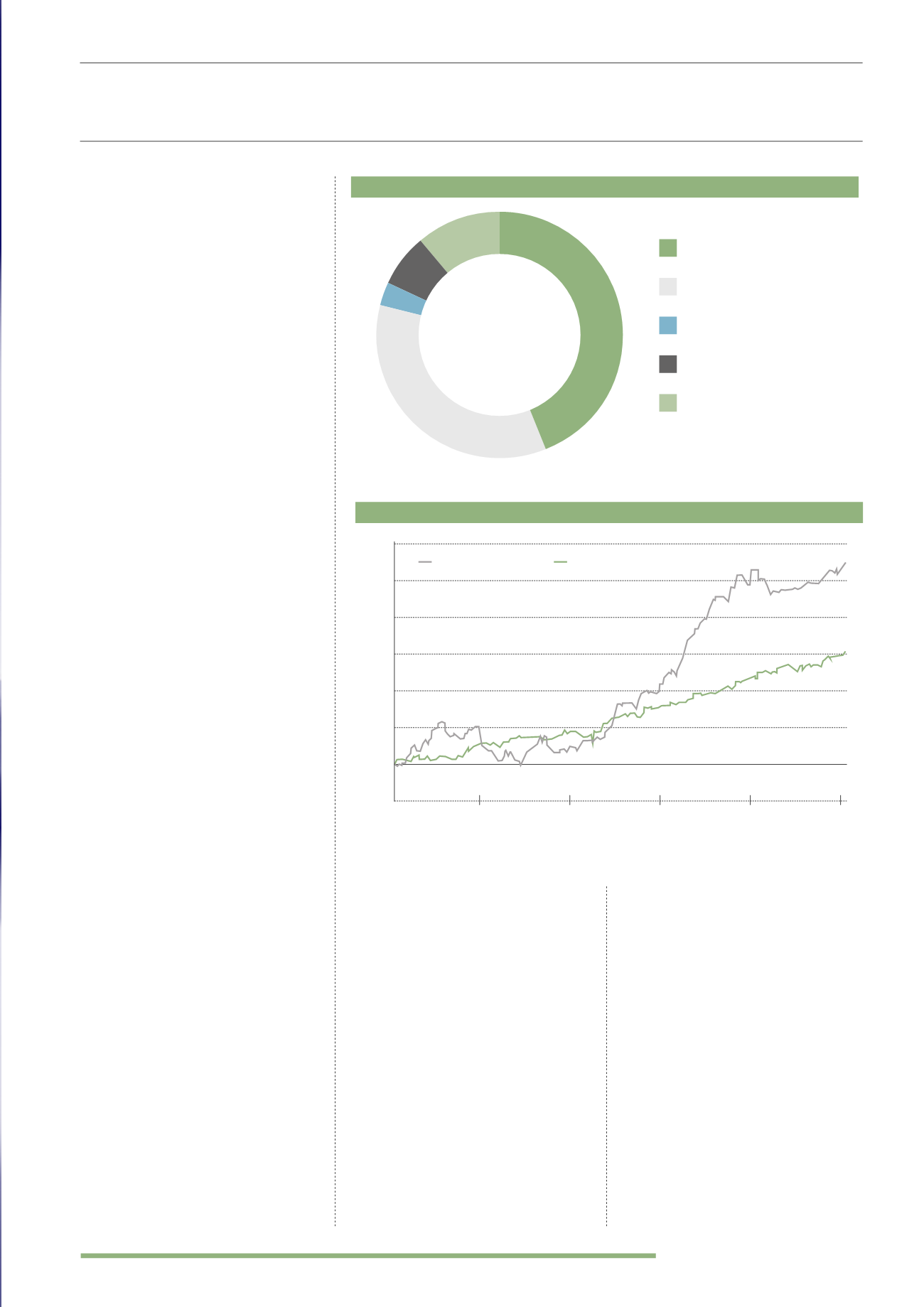

VCT DIVESTMENT

(2014)

VCT SECTOR PERFORMANCE

(2010-2015)

82%

Of investee companies

exit VCT portfolios as

thriving businesses

Trade sale

Secondary market

Sale to management

Administration

Other

Source: AIC, Going for Growth (2014)

There are a number of exits routes for VCTs investing in smaller companies

Performance over the five years to August 2015 (rebased, income reinvested)

60%

50%

40%

30%

20%

10%

0%

-10%

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Source: FE Analytics

VCT AIM Quoted

VCT Generalist