17 / 40

17 / 40

17

In recent years, China has been the most important macroeconomic driver of demand in Dry Bulk shipping and the slow-down in

its economic growth has therefore been a significant negative influence on the sector; China has experienced sharp corrections in

its equity markets, weak manufacturing output and reduced growth rates since 2013. The country is targeting 6.5% annual growth

97

for the next five years, which would be the country’s slowest growth pace in the last 25 years

36

. This slow-down has reduced

building rates and additionally, in recent years, the Chinese government has worked hard at implementing more renewable energy

sources such as hydropower, thereby reducing its reliance on coal, which has traditionally generated 70% of China’s energy

37

.

said that, according to the IMF’s April

2015, World Economic Outlook, “Global

growth remains moderate, with uneven

prospects across the main countries

and regions. It is projected to be 3.5% in

2015. Relative to last year, the outlook

for advanced economies is improving,

while growth in emerging market and

developing economies is projected to

be lower, primarily reflecting weaker

prospects for some large emerging

market economies and oil-exporting

countries. The International Monetary

Fund outlook also points out that,

“Asia’s growth is forecast to hold steady

in 2015, and the region is expected to

continue outperforming the rest of the

world over the medium term. While the

Chinese economy is shifting to a more

sustainable pace, growth is projected to

pick up elsewhere in the region.”

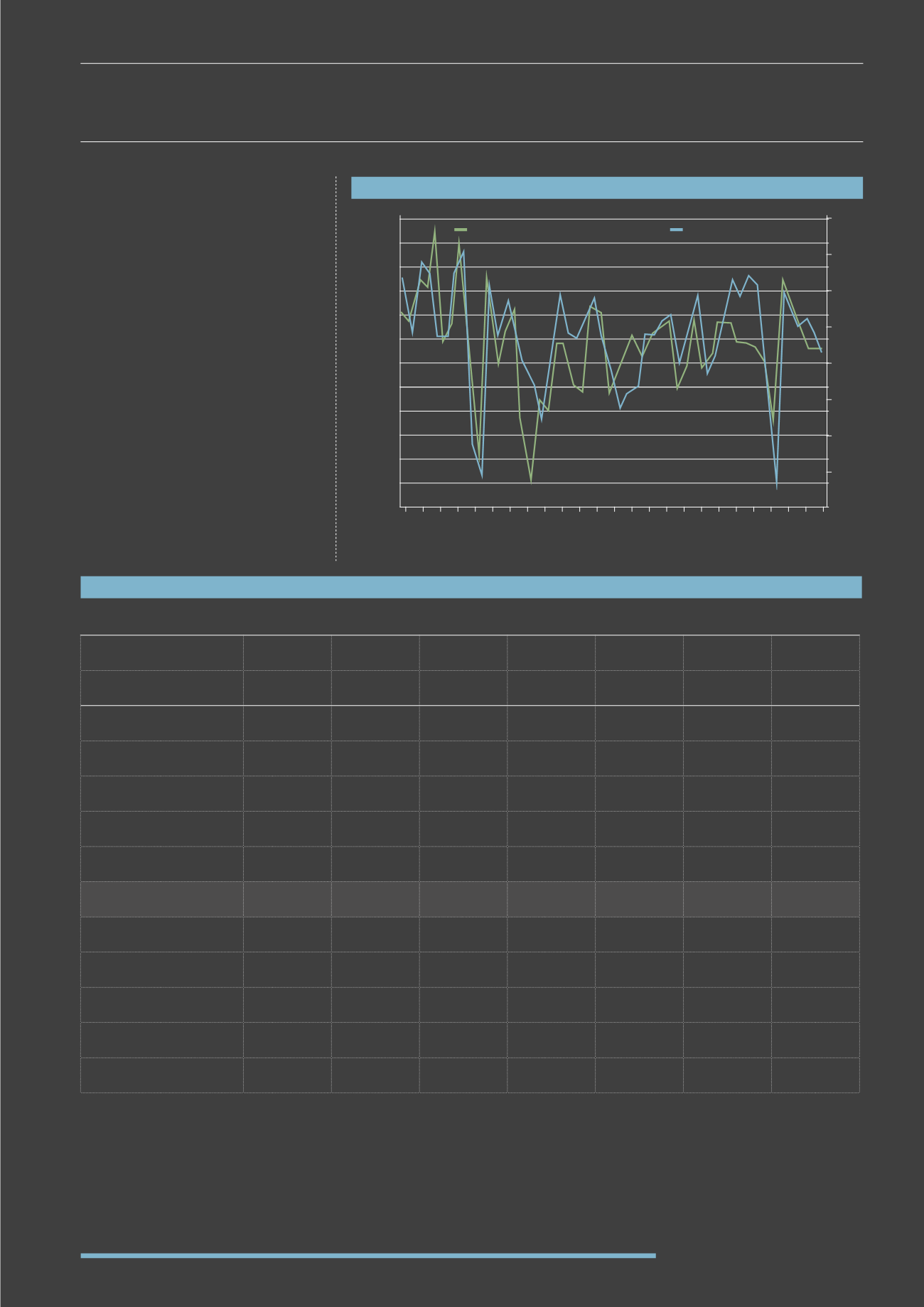

CORRELATION BETWEEN GDP AND SEABORNE TRADE GROWTH

HISTORIC AND PROJECTED GDP GROWTH

(% CHANGE PREVIOUS PERIOD)

(2010-2016)

% Trade Growth YOY

% GDP Growth YOY

2010

2011

2012

2013

2014

2015

(expected)

2016

(expected)

GLOBAL ECONOMY

5.2

3.9

3.5

3.1

3.1

3.5

3.8

INDUSTRIAL WORLD*

2.8

1.6

1.7

1.3

1.6

2.1

2.0

USA

2.5

1.8

2.8

2.2

2.1

2.8

2.3

EUROPE

2.0

1.7

-0.3

-0.4

0.8

1.2

1.7

GERMANY

3.9

3.4

0.9

0.1

1.4

1.5

1.8

FRANCE

1.7

2.0

0.3

0.4

0.4

1.0

1.6

JAPAN

4.7

-0.5

1.4

1.5

0.8

0.8

0.7

UK

1.7

1.1

0.3

1.7

3.1

2.7

2.5

EMERGING ASI A

9.7

7.9

6.7

6.1

6.0

6.3

6.5

CHINA

10.4

9.3

7.7

7.7

7.3

6.5

6.5

INDI A

10.3

6.6

4.7

4.7

5.3

6.3

6.8

KOREA

6.3

3.7

2.0

3.0

3.6

4.1

4.0

LAT IN AMER ICA* *

6.0

4.6

2.9

2.5

1.1

1.9

2.8

Source: Drewry

21

Source: ICS and UNCTAD

“The average age reduction is around 4 to 5 years since 2011, with Handymax and Supramax

falling from 30.6 to 26.6 years”

34

Drewry Maritime Research, Dry Bulk Forecaster | 3Q 2015

7%

14%

6%

12%

5%

10%

4%

8%

3%

6%

2%

4%

-4%

1%

2%

-6%

0%

0%

-8%

-1%

-2%

-10%

1966

1982

1998

1968

1984

2000

1970

1986

2002

1972

1988

2004

1974

1990

2006

1976

1992

2008

1978

1994

2010

1980

1996

2012

2014

Seaborne trade

World GDP

*

G10

**

Latin America and Caribbean