13 / 40

13 / 40

13

for the investment sector which is

closely correlated to wider economic

markets and factors, but also with

potential for substantial gains. This

allocation might form part of a diverse

satellite portfolio of EIS, VCT and other

investments into unquoted companies.

TAX BENEFITS

Tax regimes on maritime activities

in many world-wide jurisdictions

are particularly low and this is also

the case with UK shipping, thanks to

the UK Tonnage tax, which is “a ring-

fenced regime allowing ship-operating

companies to have their taxable profits

from shipping activities determined at

fixed rates, according to the carrying

capacity (tonnage) of the ships in their

fleet. These, rather than the actual

profits, are then subject to corporation

tax in the normal way, producing a

low tax charge that is competitive in

the international shipping markets.

Introduced in 2000, this system reflects

the norm in many other countries

throughout the world and is explicitly

approved under the EU’s state aid

policy. ”

25

This means that Dry Bulk shipping, as a

part of the international shipping fleet,

is not an industry which is subject to

significant taxes on its profits, leaving

a larger element of funds for the

successful upkeep of its vessels, running

of its businesses and preservation of

their capital reserves.

From 2000 to 2011, there was

remarkable growth of shipowners and

operators within the UK. The UK-owned

fleet grew by almost three times, and

the UK-registered fleet – albeit from a

very low base – grew by more than six

times

25

. This has been of major benefit

to the UK economy.

The eligibility of Dry Bulk shipping for

tax efficient investment wrappers such

as EIS and VCT, is also advantageous.

“Shipping is large, is experiencing long-term growth and will recover within private equity’s

three to five year investment horizon”

Wilbur Ross, Private Equity Investor

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

1980

1986

1992

1998

2004

2010

1983

1989

1995

2001

2007

2013

1982

1988

1994

2000

2006

2012

1985

1991

1997

2003

2009

2015

1981

1987

1993

1999

2005

2011

1984

1990

1996

2002

2008

2014

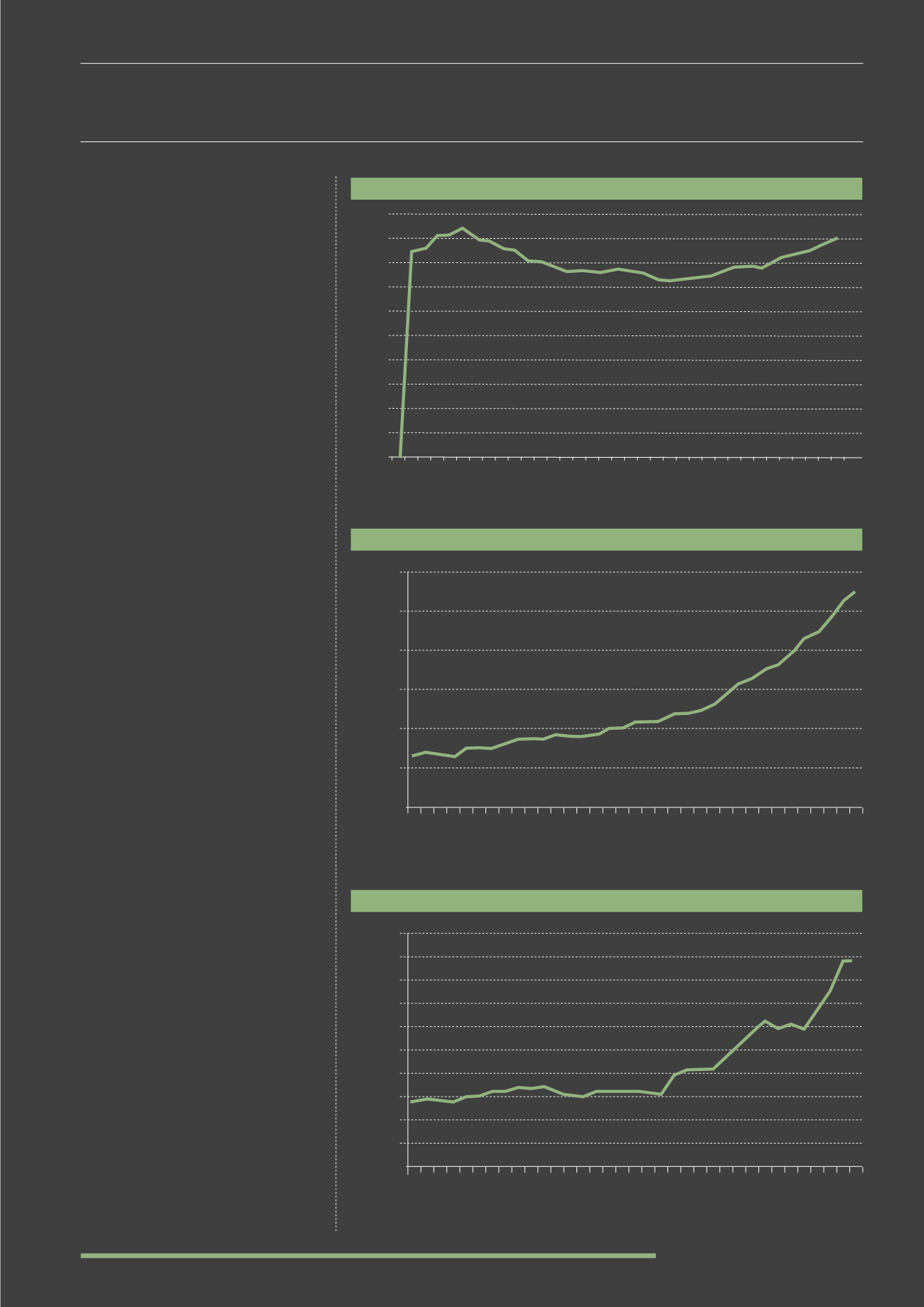

DRY FREIGHT % OF WORLD SEABORNE TRADE

(1980-2015)

TOTAL DRY BULK MAJOR BULKS SEABORNE TRADE

(1980-2014)

TOTAL DRY BULK MINOR BULKS SEABORNE TRADE

(1980-2014)

Source: Drewry Research

9

Source: Drewry Research

9

Source: Drewry Research

9

1980

1986

1992

1998

2004

2010

1983

1989

1995

2001

2007

2013

1982

1988

1994

2000

2006

2012

1985

1991

1997

2003

2009

1981

1987

1993

1999

2005

2011

1984

1990

1996

2002

2008

2014

3000

2500

2000

1500

500

0

1000

1980

1986

1992

1998

2004

2010

1983

1989

1995

2001

2007

2013

1982

1988

1994

2000

2006

2012

1985

1991

1997

2003

2009

1981

1987

1993

1999

2005

2011

1984

1990

1996

2002

2008

2014

50

400

450

500

300

250

200

100

0

50

150

Millions of tonnes

Millions of tonnes