23 / 40

23 / 40

23

There is no doubt that the industry is at or near the bottom of a cycle, but commentators views on the short term progress of the cycle vary, although all agree that

there is a lot of room for improvement: Starting 2015 at 771, the BDI dropped to 509 on 18 February 2015, rose to 1,066 in August and as of 20 November 2015 it

had slumped back to 498, the first time it has ever dipped below 500.

due to contracting demand for iron

ore and coal, and any recovery is not

expected until 2017. Falling demand

and over-supply has severely impacted

commodity values, with iron ore and coal

prices in virtual free fall.

The Dry Bulk shipping sector has been

a casualty of these developments with

resultant impacts on vessel earnings.

However, there is some optimism for

small vessel employment, as the onset of

El Nino weather conditions will increase

demand in the long-haul grain trade.”

50

The Chief Executive of international Dry

Bulk shipping company, Golden Ocean,

cited over-supply could be a quicker

process than some expect (but still up

to 18 months). His reasoning was that

over 50% of the current orderbook for

new vessels is at Chinese yards and

that the precarious financial status of

such yards suggests a high proportion

of these orders will simply not be

delivered.

51

It is certainly true that Chinese

shipyards in particular have seen a

number of newbuilding cancellations.

Recently after its yard allegedly failed to

meet deadlines and deliver vessels, Dry

cargo ship-owner Precious Shipping,

cancelled two shipbuilding contracts

for 64,000 dwt Dry bulk carriers due

from Nanjing based shipbuilders, Sainty

Marine

52

. In addition, in November

2015, a European buyer cancelled the

construction of one 82,000 dwt bulk

carrier due to be built at the Cosco

shipyard in Dalian, China. The vessel

was originally scheduled for delivery in

the third quarter of 2016. Other Chinese

shipyards are in serious financial

trouble, with Rongsheng, once China’s

largest shipbuilder, on the verge of

bankruptcy after orders dried up, with

debts of 20.4 billion yuan in combined

debt owed to 14 banks, three trusts and

three leasing firms and allegations of

exaggerated order books designed to

make the company look stronger.

53

Deutsche Bank is also optimistic

about the short term for the Dry Bulk

shipping sector – so much so, that in its

September 2015 Industry Update on

Dry Bulk shipping, it re-rated its stock

recommendation on listed shipping

companies such as Diana Shipping from

Hold to Buy

54

. This was on the back of a

trip to Asia, where, “Nearly everybody

we spoke with was cautiously optimistic

on the prospects for Dry Bulk rates,

asset values and equities - the result

of recalibrated demand expectations

and scrappage-driven supply control.

In particular expectations were for a

“Slow and steady improvement in 2016,

translating to 15-20% year on year

increase in spot rates after excluding the

first quarter of 2015’s weak levels”.

However, Platts Dry Bulk Market Survey

of August 2015 revealed a slightly longer

projected period of recovery, citing 50%

of industry respondents feeling the

recovery of the Dry Bulk freight market

was three to five years away. Presumably,

the major European financial institution

which provided Scorpio Bulkers with a

commitment for a loan facility of up to

$12.5 million in late November 2015, with a

final maturity of five years from the date of

signing

55

, shares the view that there will be

money to be made in the sector by then.

“Since 2013, there have been billions of dollars in equity flowing into the industry, and the scary

thing is that the reported number is not all of it. A lot of private placements don’t show up on

anyone’s league table”

2

Chris Weyers, Head of Maritime Investment Bank

ng at Stifel Financial

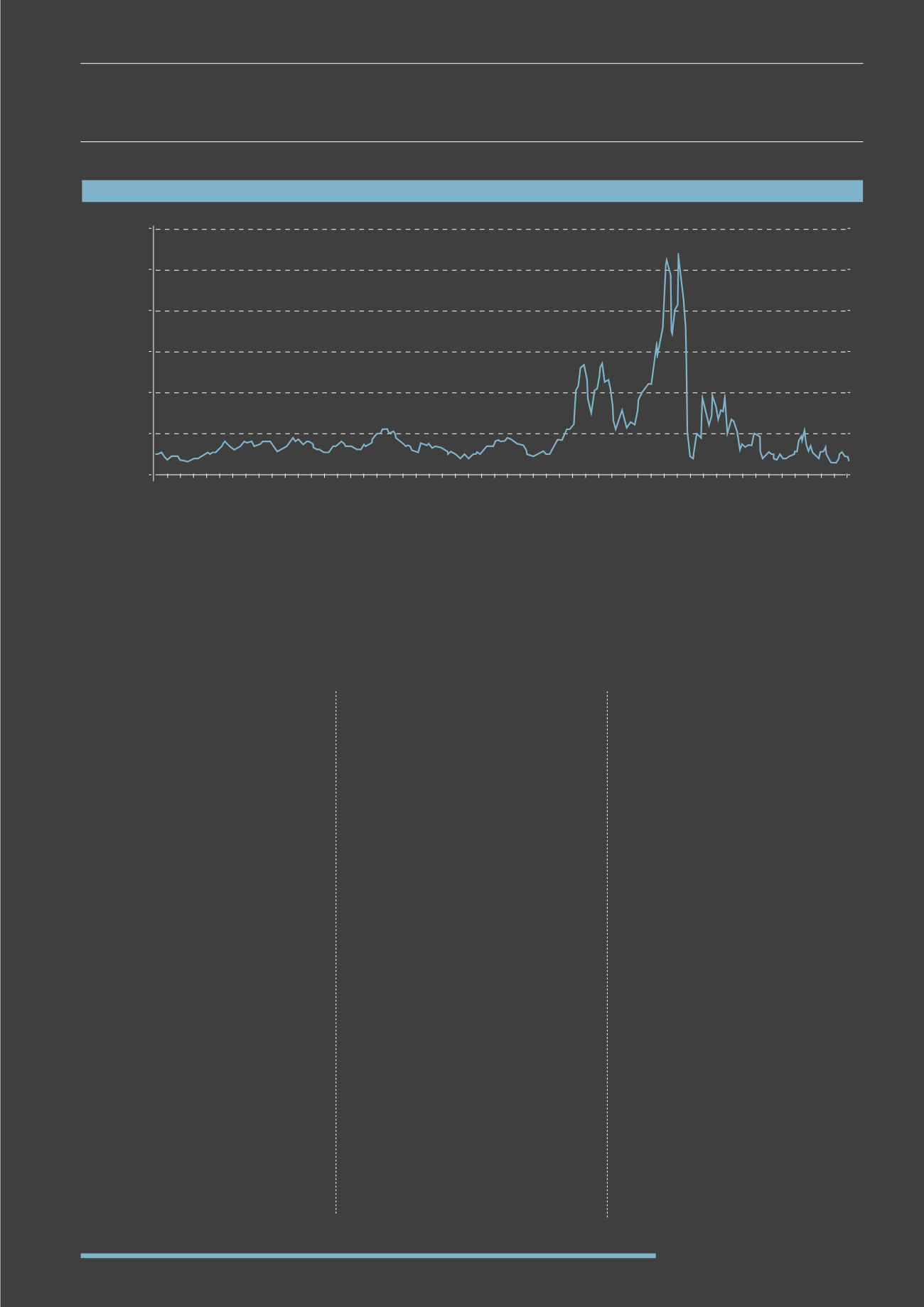

Source: Baltic Exchange

14

BALTIC DRY INDEX (BDI)

(1985-2015)

12,000

10,000

8,000

6,000

4,000

2,000

Jan 85

Aug 85

Oct 86

Dec 87

Feb 88

Apr 90

Apr 91

Apr 92

Oct 93

Dec 94

Feb 96

Jan 92

Jan 99

Jan 06

Aug 06

Jul 88

Jul 95

Jul 02

Jul 09

Jan 13

Mar 86

Mar 93

Mar 00

Mar 07

Oct 07

Dec 08

Feb 10

Apr 11

Jun 12

Aug 13

Oct 14

Sep 89

Sep 96

Apr 97

Jun 98

Aug 99

Oct 00

Dec 01

Feb 03

Apr 04

Jun 05

Sep 03

Sep 10

Mar 14

May 87

May 94

May 01

May 08

Nov 90

Nov 97

Nov 04

Nov 11

May 15

Dec 15

0