15 / 40

15 / 40

15

MARKET UPDATE

In November 2015, Frank Dunne

(a partner at Watson, Farley and

Williams, who undertakes a broad

range of ship finance work and

commercial shipping transactions for

major international shipping finance

lenders and shipowners) summed up

his thoughts on the Dry Bulk sector;

“We appear to be at a ten-year low

in the value and freight rate cycle for

dry cargo. If so, now is a good time

to buy, so long as leverage is low and

the further investment in a carry cost

is available. Market sentiment is that

values and freight rates are unlikely

to improve significantly for the next

couple of years. The fleet is young

so it will take time for over-capacity

to be worked out. Much depends on

China and growth. Also restraint by

Shipyards to avoid adding capacity as

soon as conditions start to improve.”

OVER-SUPPLY

There is no denying that the Dry Bulk

shipping market has experienced very

tough times since the effects of the

world economic recession took hold

in the sector in late 2008. Pricing was

hit hard: as an example, one-year time

charter rates were at their highest for

the Supramax vessels in 2008, reaching

over $60,000/day and have since

struggled to recover, and in late 2015

were sitting at well below $10,000.

9

The Baltic Dry Bulk Index (BDI) hit an

all-time low in 2015, but, although

reduced, there is still trade growth

within the sector, with expected

total Dry Bulk trade growth in 2015

at 1.2%, compared to 8.4% in 2014

26

.

This indicates that there is increasing

demand to move commodities by sea,

albeit affected by demand-side issues,

and highlights the huge importance of

supply-side factors in terms of the Dry

Bulk fleet. It is these supply-side issues

which have had the greatest influence

on the market in recent years, with

the Financial Times commenting that,

“Most shipping sectors remain in deep

financial trouble. Delivery of the glut

of vessels ordered before the financial

crisis has driven down earnings for

dry bulk carriers, most tankers and

container ships.”

27

Owners, operators and analysts are

fully aware of the cycles experienced by

this sector and according to Platts Dry

Bulk Market Survey August 2015, ”55%

[of bulk market participants] indicated

tonnage oversupply as the main issue

for the dry bulk market.”

This recognition of the contribution

of vessel over-supply to the weak

market has led to action in the form

of a reduction in the number of new

ships ordered, coupled with high levels

of demolitions (scrapping of ships);

Bimco, the world’s largest international

shipping association was positive about

the trend for market improvement in

October 2015, citing the marginal year-

to-date growth of the dry bulk fleet of

just 2.1%, made up of the inflow of 39.7

million dwt offset by demolition of 23.8

million dwt. In terms of new orders,

Clarkson’s orderbook statistics showed

only 84 new contracts recorded at the

end of August 2015, in stark contrast to

less than two years ago when capacity

equal to the year-to-date amount in

2015 (4.7 million dwt) was contracted in

just 16 days.

28

In fact the delivery of previously

ordered new vessels, at a time when

the market outlook was stronger, is

part of the problem and a further 36.3

million dwt of Dry Bulk vessel capacity is

expected to hit the water by the end of

2015

29

. This is made up of 118 Capesizes,

139 Panamaxes, 300 Supramaxes (155

ships last year) and 217 Handymaxes.

However, delay, cancellation or default

on newbuild orders should also be

taken into account, with a number

considered doubtful for delivery;

Drewry expect 7% of Handymax orders

and 17% of Supramax orders to be

cancelled. Furthermore, a number of

Chinese shipyards are in trouble or have

filed for bankruptcy protection while

Korean yards are also burdened with

high debts.

When demolition is taken into account,

Bimco predicts that 2015 fleet growth

will be at a 10-year low of 2.5%

28

.

Dryships Inc. puts this figure at only

2.4% in 2015, followed by a 4.0%

increase in 2016

30

.

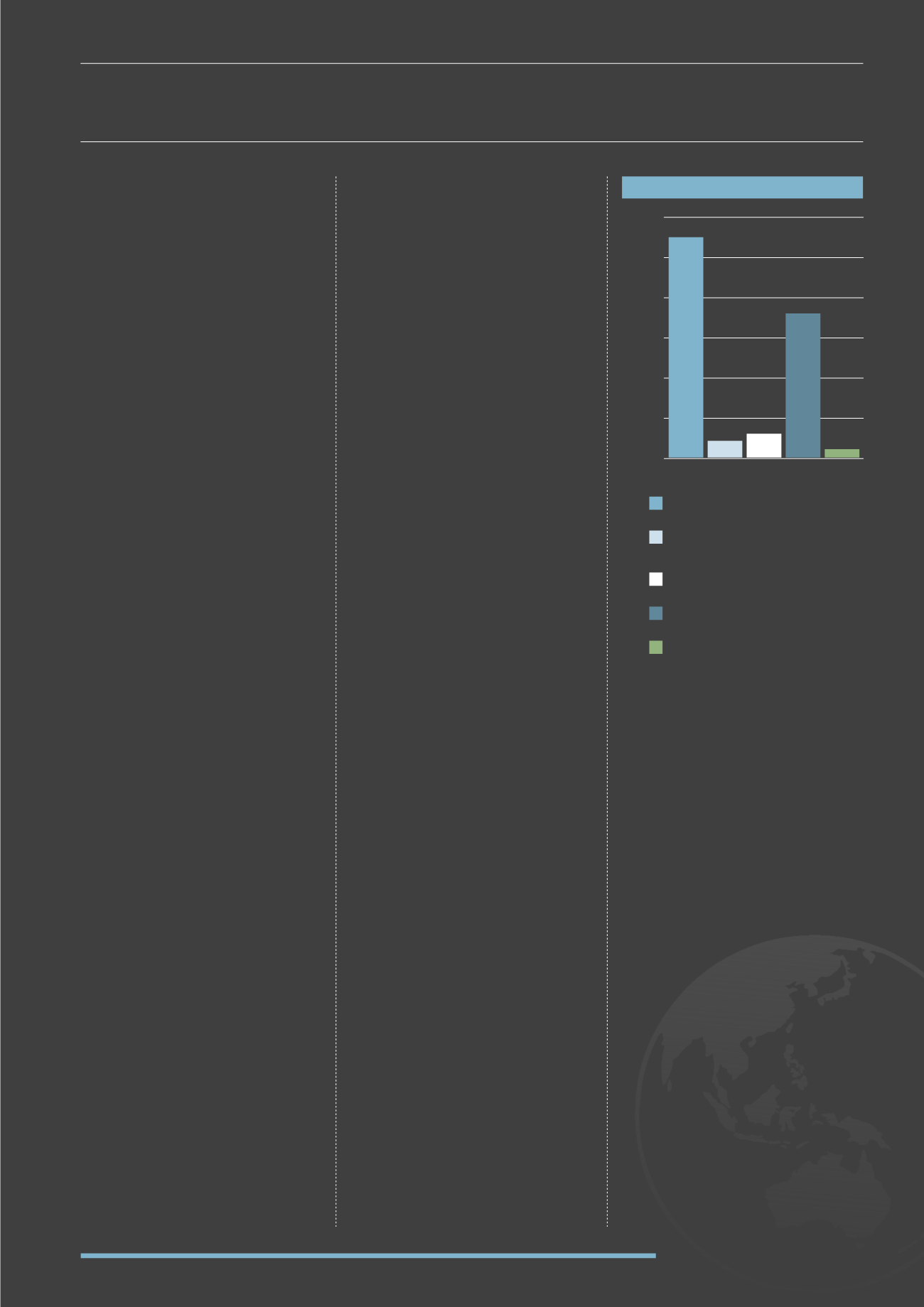

MAIN ISSUE FOR THEMARKET

60

50

40

30

20

10

0

“Most shipping sectors remain

in deep financial trouble.

Delivery of the glut of vessels

ordered before the financial

crisis has driven down earnings

for dry bulk carriers, most

tankers and container ships.”

Financial Times

Oversupply of tonnage

China & Europe push towards

greener energy

Low tonne-mile demand

All of these factors

Other

% of respondents

For the year to September 2015, Drewry

figures put fleet growth at around

3%, bearing in mind the overall fleet

size of 10,237 vessels of 747 mdwt in

September 2014, compared with the

September 2015 numbers. Previous

years’ increases have been much more

significant, with Intercargo putting the

2012 Dry Bulk fleet at 8,141.

Of course, these statistics mask

variances for different vessel types,

which in turn have an impact on

the market. For example, Panamax

and Supramax fleets are expected to

increase by 1% and 4% respectively

31

in

2015. Such variations are a mark of the

differing markets in which the various

Source: Platts