16 / 40

16 / 40

16

DEMAND FACTORS

Demand is reliant on commodity

production and distribution

requirements and this is strongly

influenced by macroeconomic factors

and in particular their effects on

commodity supply industries such as

energy, manufacturing and construction

4

.

In terms of commodities, iron ore and

coal (both sued in the production of

steel) make up almost two-thirds of the

Dry Bulk shipping industry and China is

currently the biggest consumer of these

two commodities.

35

MACROECONOMIC ELEMENTS

The close correlation of world trading

activity and GDP levels and the resulting

effects on the Dry Bulk shipping market

are well known; with the contributions

of China, India and Brazil increasing as

their GDP growth rates are significantly

higher than those of developed

countries. It is expected that trade

between Africa and Asia and the Middle

East and Asia will keep growing at a

higher pace than the rest of the world

as we approach 2020, with a positive

effect on the Dry Bulk market

4

. Having

vessel types operate. Drewry’s 3Q 15

Forecaster noted that delivery numbers

have remained consistent for Supramax

and Capesize vessels in the third

quarter, with shipowners still taking

deliveries of Supramax vessels as grain

trade was seen flourishing in the ECSA

region in the third quarter with growth

anticipated in the Black Sea grain

shipments in the last quarter of 2015.

Increased demolitions are a symptom

of a weak market and 2015 is likely to

be a record breaking year in terms of

vessels being sent to the scrapyards.

This occurs when a ship reaches the

end of its useful life at around 25 years,

but in a depressed market, it is not

uncommon for ships to be scrapped

at 20 years. In the first six months of

2015, 19.5 mdwt were demolished,

an increase of approximately 145%

compared to the same period in 2014

30

and Drewry expects demolition to

increase further as small players,

particularly those burdened with debt

repayments on top of standard opex,

will find it difficult to to survive for long

in the weak freight market and wish

to avoid the costs of dry dock surveys.

(According to international regulation,

every sea-going vessel has to undergo

two dry docks within a period of five

years to allow for inspection to ensure

the safety of the vessel. A ship in dry

dock is a ship out of service and it is a

complex process which is expensive

and, depending on the number of days

out of the water, represents ongoing

loss of income)

32

The reducing age of vessels being

scrapped in 2015 (with the exception

of the largest vessels) indicates the

growing pressure that low freight prices

places on ship operators to cut their

losses, particularly with older vessels

incurring higher operating costs and

thereby diminishing the scope for profit

in poor market conditions.

33

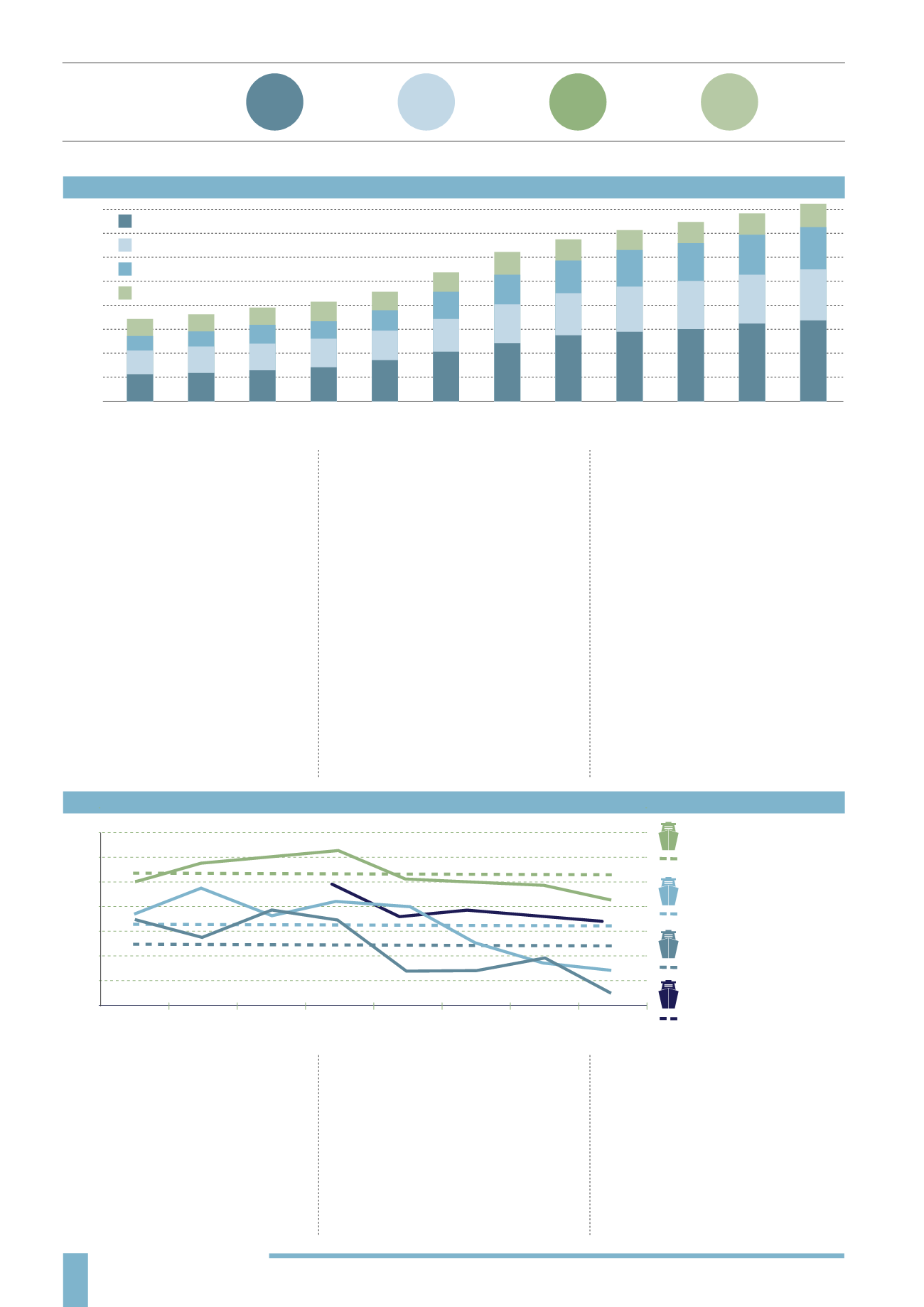

The average age reduction is around 4

to 5 years since 2011, with Handymax

and Supramax falling from 30.6 to 26.6

years.

34

Source: British Marine

NUMBER OF VESSELS

AT DEC 2015:

(TOTAL 10,689 VESSELS)

CAPESIZE

309.6 mdwt

196.4 mdwt

179.3 mdwt

92.3 mdwt

PANAMAX

HANDYMAX

HANDYSIZE

3323

3266

2467

1633

DECREASING DEMOLITION AGE

(YEARS)

(2008-2015)

FORECAST DRY BULK FLEET DEVELOPMENT

(2005-2016)

HANDYSIZE

average age since 2008

average age since 2008

average age since 2008

average age since 2011*

* Data for 2008 to 2010 for Handymax/Supramax unavailable at time of going to print

PANAMAX

CAPESIZE

HANDYMAX/SUPRAMAX

Source: Drewry

34

2008

34

32

30

28

26

24

22

20

2009

2010

2011

2012

2013

2014

2015

Years

Capesize

Panamax

Supramax

Handysize

2005

0

100

200

300

400

500

600

700

800

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: Market Realist

mdwt