19 / 40

19 / 40

19

being made by the government, with the

Chinese central bank cutting interest

rates, improving bank lending tools to

boost economic activity, introducing new

stimulus measures to fund construction

projects and devaluing the yuan to

increase export competitiveness.

41

Whilst the knock-on effects of economic

and political movements in China have

proved to be an unwanted and frankly

huge drag on the Dry Bulk market, it is

certainly not the only country to impact

trade, with India filling a meaningful

portion of the demand gap for coal left

by China

33

and the growing requirements

of both developed and developing

nations, including Japan and Vietnam

34

,

for increasing amounts of electric power.

For coal, the main exporters are Australia,

South Africa, Russia, Indonesia, United

States, Colombia and Canada. The main

importers are Europe, Japan, South Korea,

Taiwan, India and China.

Indeed, the supply of ships versus

the demand for the movement of

commodities is predicted to show

demand outstripping supply by 2018 for

some Dry Bulk sectors.

In the short term, iron ore and coal shipments from China have actually been boosted by the slowdown in steel consumption within

China, as mills have sought to find overseas buyers for their output

39

and in the longer term, the use of these commodities in the

production of steel is an important factor, with Dr Edwin Basson, Director General of the World Steel Association saying that, “For the

past decade, the steel industry was dominated by events in China. The evidence is that the steel industry is now entering a period of

pause before undoubtedly picking up again when markets other than China drive new demand.”

42

For other commodities such as grains, international demand continues to be strong with wheat exports from the Black Sea countries

projected at record levels in 2015/16, much of which is destined for the Middle East and North Africa.

33

“The Bulk Shipping market is presently very vulnerable to changes in China’s demand”

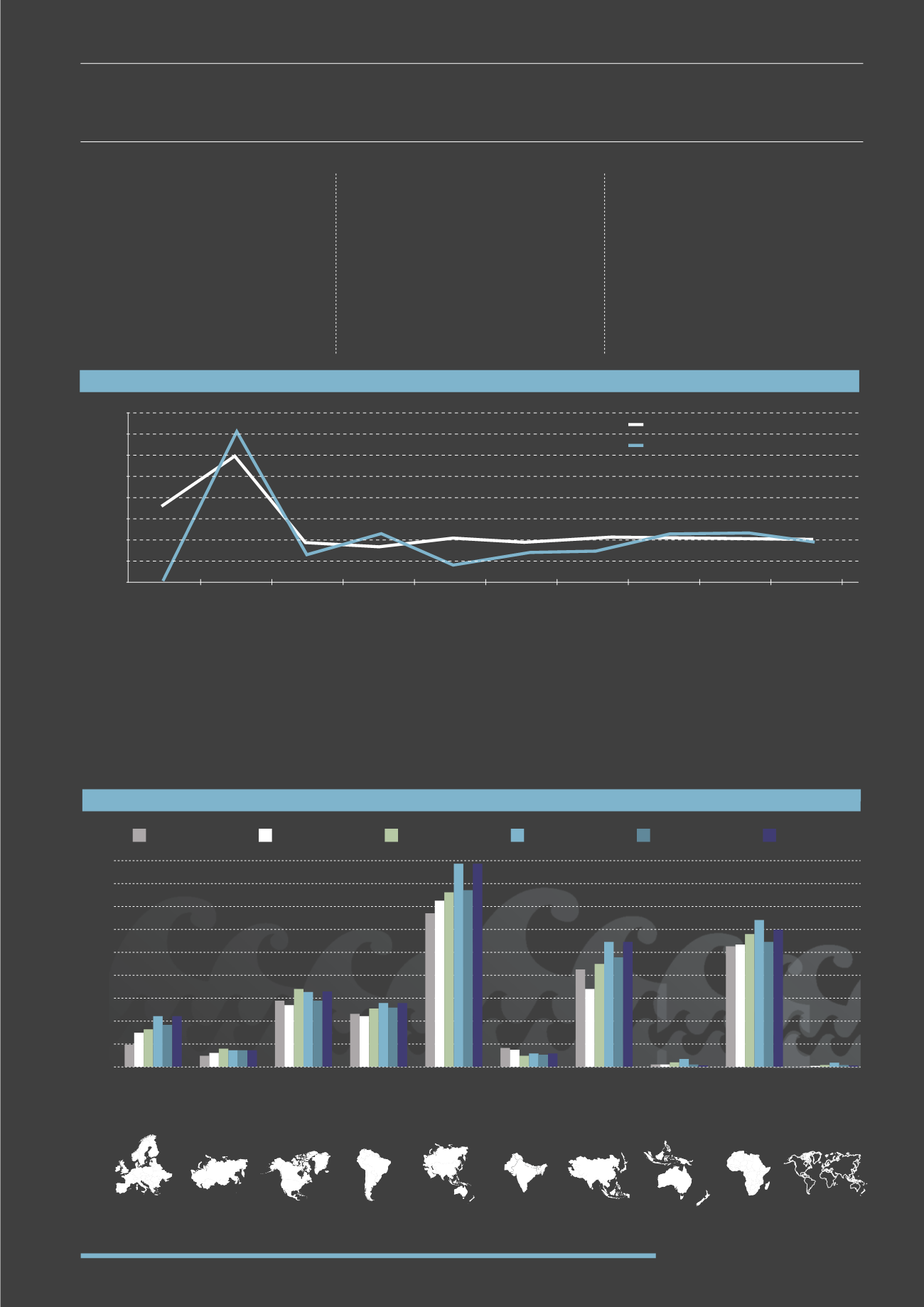

HANDYMAX HISTORIC & FORECAST SUPPLY/DEMAND GROWTH

(2011-2020)

Source: Drewry Maritime Research

34

40

35

30

25

20

15

10

5

0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Growth in demand

Growth in supply

Millions dwt

MAJOR GRAINS IMPORTS

(2009-2014)

EUROPE CIS

N&C

AMERICA

SOUTH

AMERICA

PACIFIC

ASIA

SOUTH

ASIA

NE

ASIA OCEANIA AFRICA OTHERS

90

80

70

60

50

40

30

20

10

0

2009

2010

2011

2012

2013

2014

Millions of tonnes

Source: Drewry Dry Bulk Forecaster 3Q 15

34