8 / 40

8 / 40

8

World trading activity is closely

correlated to global GDP levels and

consequently, as with all industrial

sectors, shipping is susceptible to

macroeconomic trends, including

economic downturns. As a result,

following several years of extremely

strong shipping markets, the

contraction in trade following the

‘credit crunch’ in 2008 inevitably,

severely and suddenly, reduced

shipping demand.

Recovery has been slow and patchy,

with current market conditions

incredibly challenging for ship owners

and operators. Nevertheless, the longer-

term outlook still remains positive. The

continual rise in the global population,

emerging economies providing new

demands for goods and raw materials

and the position of shipping as a safe

and efficient carrier, as well as the most

fuel efficient and carbon friendly form

of commercial transport

5

all stand in the

industry’s favour. Indeed, even in the

midst of the market difficulties, after

the world economic recession of 2008

and beyond, the world’s ships have

carried record volumes of cargo, with

10.8 billion tonnes predicted for 2015

6

and the world fleet now standing at

approximately 55,000 vessels of 1000+

deadweight tonnage (dwt)

7

.

The main shipping segments are

dry bulk, crude oil tankers, product

tankers and containers – each with their

distinct market drivers and volatility,

not necessarily correlated with each

other.According to Drewry research, in

2014 45% of seaborne trade was in the

Dry Bulk Sector. Some commentators

expect this to be over 50% in 2015.

The late 1960s saw the emergence of

Dry Bulk shipping as a separate sector

from conventional general cargo, driven

initially by relatively low value, high

volume commodities – especially iron

ore and metallurgical coal, as well as

the major food and feed grains (these

are known as major bulks, whilst minor

bulks are made up of steel products,

forest products, bauxite or alumina and

cement, and fertilisers)

8

. The massive

increase in the volume of thermal

or steam coal in the 1970s secured

the position of the sector and trade

volumes continued to grow steadily in

the 1980s and 1990s. The Chinese trade

boom from the mid-2000s brought

extraordinary increases in seaborne

trade in commodities such as iron ore,

as well as further expansion of the Dry

Bulk fleet

9

.

In the UK, shipping is not only vital to

our commodity supply as an island

nation, but is also an important income

generator. In 2013, shipping contributed

around £1.8 billion to the UK’s trade

balance, whilst around 95% of goods

that the UK imports and exports are

transported by sea, including about 40%

of our food and about a quarter of our

energy

10

. The UK’s proud history as a

sea-faring nation may have witnessed

the near decimation of its ship-building

industry in the last few decades, but

Lord Mountevans of the Department

of Transport asserts that, “we continue

to provide services to the world that

support their charter, insurance, sale

and purchase”. This is evidenced by the

fact that UK firms account for 30-40%

of the global Dry Bulk chartering ship

broking business and Lord Mountevans

sees “a once in a lifetime opportunity

to exploit the expected growth in world

trade to help create jobs, increase the

export of our maritime services and

encourage maritime-related investment

across the country. This is a sector rich

in SMEs and innovation and one that,

with the right conditions, can contribute

to enterprise, productivity and both

national and regional growth in the UK.”

10

As a result of the differing sizes and

uses of the Dry Bulk vessel types, the

value of the vessels varies and charter

income can also differ. For example, in

August 2015, it was reported that rising

iron ore shipments from Australia and

Brazil to China have led the Capesize

rates to beat the overall Dry Bulk sector

in recent months.

12

Vessel age, speed, and fuel efficiency

in addition to cargo size, where larger

“In 2014 Drewry calculated 45% of seaborne trade was in the Dry Bulk Sector. Some

commentators expect this to be over 50% in 2015”

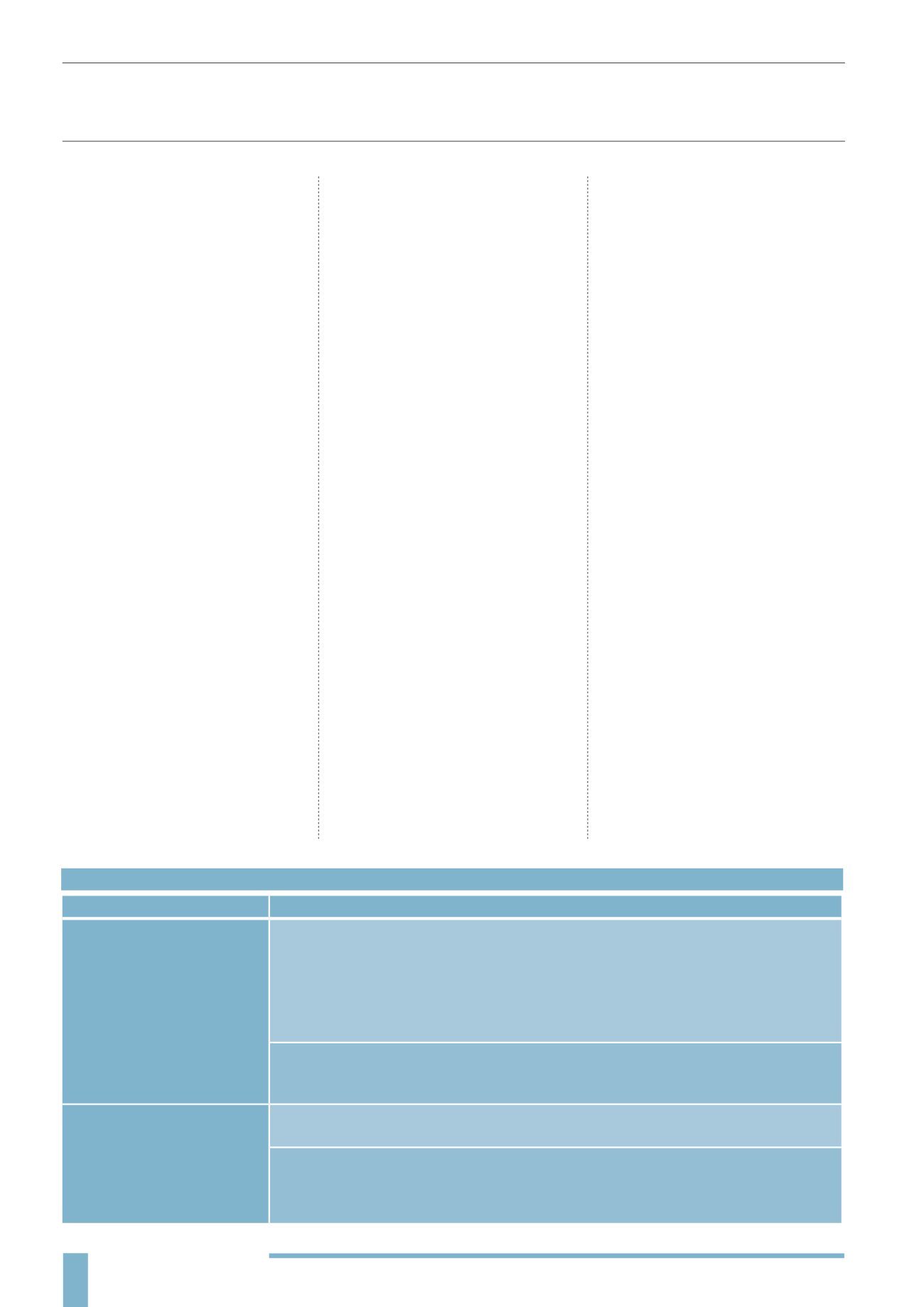

DRY BULK SHIPPING VESSELS CHARTER TYPES

CHARTER TYPE

DESCRIPTION

LONG-TERM

CONTRACT /

TIME CHARTER

Arrangements between producers and consumers of key products – normally industrial raw

materials. The buyers want security of supply guaranteed and some certainty on price over

a known period. The charterer takes the ship on hire for a designated period (for example,

12 months). The freight rate agreed between the ship-owner and charterer is at a daily hire

rate (in US$), rather than as a US$ per tonne figure. The vessel owner meets the ship’s oper-

ating and capital costs, with the charterer paying all variable voyage expenses (mainly fuel

costs, plus port and canal dues)

13

.

Bareboat Charter

gives the charterer responsibility for all crew, fuel and operational costs for

the duration of the charter period. (EIS investments are excluded from entering a bareboat char-

ter as this is akin to asset leasing which is not permitted as a qualifying trade under the EIS regime).

SPOT CHARTER

Single Voyage

involves the hire of a vessel for just one stipulated voyage, carrying a desig-

nated quantity of a named commodity.

Voyage/Trip Charter

generally lasts from 10 days to three months. The ship owner pays for

vessel operating expenses, including crew costs, provisions, deck and engine stores, lubricat-

ing oil, insurance, maintenance and repairs and for commissions on gross revenues. Ship

owner would also be responsible for each vessel’s intermediate and special survey costs.