9 / 40

9 / 40

9

loads benefit from economies of scale

and generally receive a lower rate per

tonne than a smaller one, can also affect

value and charter rates. Charter rates

are generally available on the basis of a

long-term contract or a spot rate.

Spot charters expose ships to the

immediate volatility of market

sentiment, whilst long term contracts

involve committing the vessel over

a period in return for a fixed level

of revenue. In periods of weakening

charter rates and / or market

uncertainty, the time charter is viewed

as the more secure option, whilst a

rising market may encourage ship

owners to accept short term spot rates

to enable them to take immediate

advantage of price increases.

Charter price fluctuations are also

highly influenced by supply and demand

factors, based on the supply of vessels

and the demand generated by trading

conditions and international commodity

prices and requirements. New ships

are generally ordered when owners

judge a shortage in supply, and/or an

increase in demand, (although the price

of new or second hand vessels is also a

consideration, as is the price available

from scrapping existing vessels which

are to be replaced). The supply and

demand curve is heavily affected by the

two-year lead time required to build

new ships, providing both a lag and

market expectation for the delivery of

new tonnage, which eventually pushes

down charter prices when supply of

vessels outstrips supply of cargos.

Consequently, historical data

demonstrates a cyclical market, marked

by rises and falls.

The Baltic Dry Bulk Index (“BDI”) is an

index of daily charter rates issued by

the London-based Baltic Exchange.

It provides an average index for 23

shipping routes measured on a time-

charter basis of current freight rates for

Handysize, Supramax, Panamax, and

Capesize Dry Bulk carriers, carrying a

range of commodities including coal,

iron ore and grain.

15

The cyclicity of the sector as can be

seen in the BDI graph has contributed

to substantial volatility with the BDI

reaching a peak of 11,793 in 2008 and

an all-time low in November 2015 of

just 498. This suggests the possibility

of sizeable future rises in the index

16

,

and even the mean monthly average

from January 1985 to September 2015

(excluding the extraordinary highs of

2007 and 2008) of 1,657

17

, indicates the

real possibility of gains.

Dry Bulk is a fragmented investment

sector, in which, unlike other specialised

areas of the world shipping fleet, there

are approximately 2,000 different

owners and the largest 50 owners

account for only around 36% of the

fleet in terms of deadweight carrying

capacity

13

. This has the effect of allowing

smaller players into the market.

The traditional investment routes of

public and private shipping companies,

including Greek shipping families

who have a history of decades and

even centuries in the industry, other

corporate vehicles, ultra-high net worth

families and family offices, are losing

their monopoly. According to Hedge

Fund Journal, “The global bulk shipping

industry is currently undergoing a

fundamental change. It has been and

continues to be mostly dominated by

principal-led, family-owned companies,

funded mainly by commercial banking.

However, following the financial crisis

and the extended downturn in charter

rates, vessel values and traditional bank

lending, alternative sources of finance

– particularly private equity and hedge

funds – have become increasingly

prevalent in the sector.”

2

The report’s sponsor, TIME Investments

(a part of Alpha Real Capital Group,

a global co-investing fund manager

with over £1 billion of assets under

management) manages an EIS service

which looks at new and interesting

investment sectors on which to overlay

EIS benefits for smaller investors. The

TIME:EIS Service aims to allow investors

who are looking for better growth for

their funds than the returns offered by

banks and orthodox routes, to access

the Dry Bulk shipping market via EIS

companies using the expertise of an

experienced vessel owner and operator,

to acquire, operate and eventually sell

a Dry Bulk ship and target a profitable

investment realisation.

Whilst there is not universal agreement,

many market commentators are now

suggesting a recovery to the Dry

Bulk shipping sector in around three

to five years-time. It is that forecast

which is making it timely to look at

the investment sector now, taking

into account the current low pricing

of vessels and the time required for

market entry and preparation for the

improving charter price outlook, driving

up asset values.

“This is a sector rich in SMEs and innovation and one that, with the right conditions, can

contribute to enterprise, productivity and both national and regional growth in the UK”

Lord Mountevans, Department of Transport

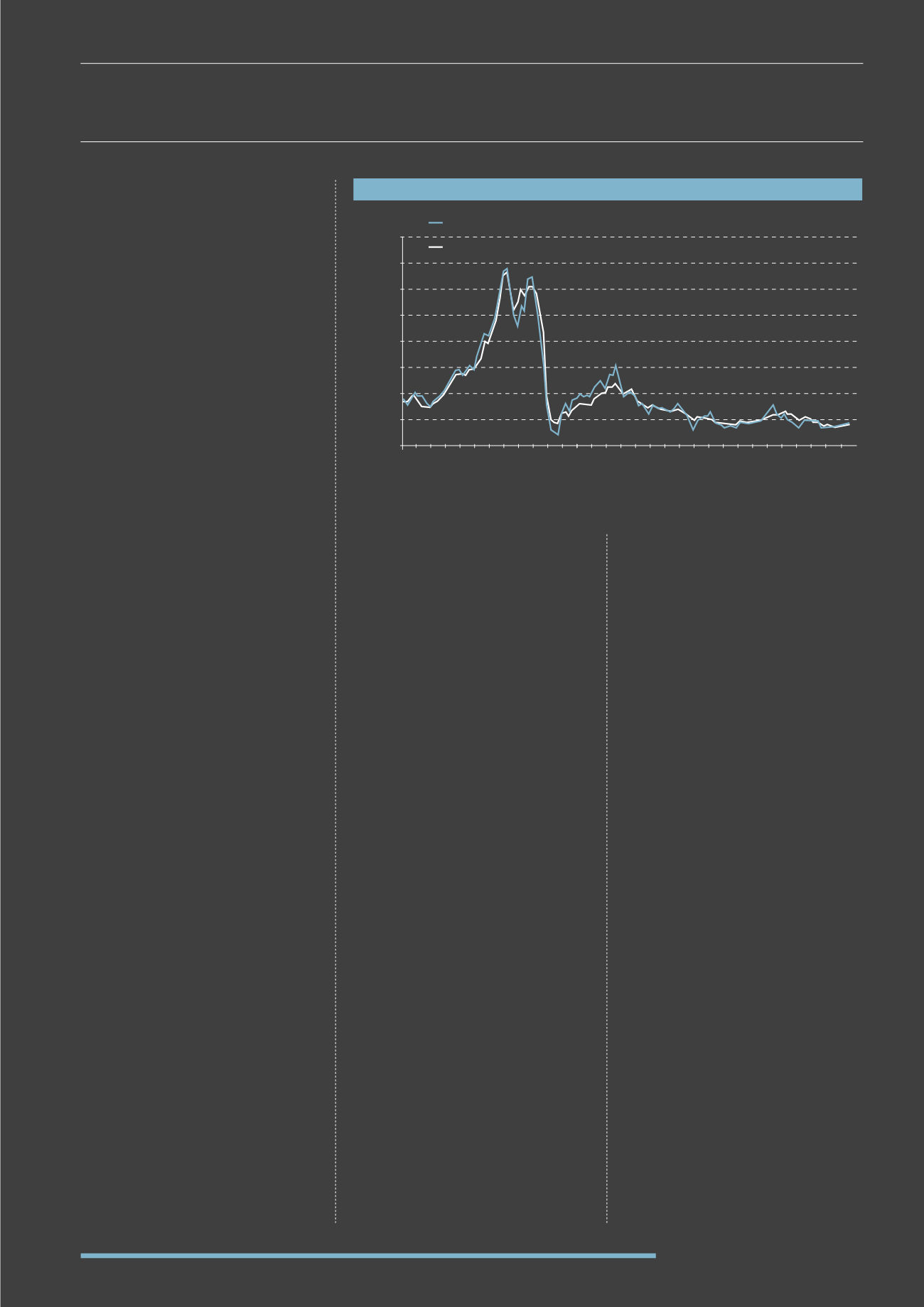

TIME CHARTER VS SPOT RATE

2005 Jul

2005 Nov

2006 Mar

2006 Jul

2006 Nov

2007 Mar

2007 Jul

2007 Nov

2008 Mar

2008 Jul

2008 Nov

2009 Mar

2009 Jul

2009 Nov

2010 Mar

2010 Jul

2010 Nov

2011 Mar

2011 Jul

2011 Nov

2012 Mar

2012 Jul

2012 Nov

2013 Mar

2013 Jul

2013 Nov

2014 Mar

2014 Jul

2014 Nov

2015 Mar

2015 Jul

$80,000

$70,000

$60,000

$50,000

$40,000

$30,000

$20,000

$10,000

$0

Spot: Average of the 6 T / C Routes for Baltic Supramax Index (US$/day)

1 Year Timecharter Rate 52,000 dwt Bulkcarrier (US$/day)

Source: British Marine