17

VALUE TO

ENTREPRENEURSHIP

What we can’t extrapolate from the

National Audit Office figures is how

much money is still invested in BPR

qualifying assets and how much new

money is going into them each year, but

we can speculate that it is significant.

And we can use the data that we do

have to make some educated guesses.

As we’ve noted, to establish exact

figures is challenging - there is no

single place (such as an exchange)

where data can be gathered, so it is

impossible to be 100% confident that

the whole-of-market is captured. Our

figures are based on desktop research

- reviewing marketing literature,

surveying investment providers and

kindly being granted access to the

data collected by platforms and review

providers. We believe they are the most

comprehensive and accurate figures

published to date.

From HMRC data, we do know that

slightly more than £1.5bn went into

EIS in the previous two tax years; over

£12bn has been cumulatively invested in

EIS since its inception. (EIS investments

are BPR qualifying).

Narrowing our focus to BPR, we can also

make an intelligent estimate based on

the AUM data that we have been able to

collect through desktop research, our

surveys and access to data provided

by comparison engine and review

provider MICAP. This is slightly more of a

guesstimate than the EIS figure, (because

there is no upfront relief being claimed,

HMRC does not collate this data), but we

calculate that there is somewhere in the

region of £2bn assets under management

in BPR products at the moment.

Taking the EIS and BPR numbers

together, that’s something like £14bn

of capital currently put to work in small

businesses that may not have found its

way there without investment products

built around these incentives.

To put this figure into some sort of

context, according to the BBA (British

Banking Association), total borrowing

facilities provided by banks for SMEs

stand at around £113bn. And the

think tank NESTA estimate than the

Alternative Finance market has provided

£1.8bn of finance in total (a number that

is growing fast).

The point has been made before, but is

worth making again - this is an injection

of capital into a vital part of the UK

economy:

In addition, BPR is absolutely not a pure

tax loss to HMRC when the contribution

of the investee companies is taken into

account - through Corporation Tax,

National Insurance Contributions, VAT,

employees’ income tax - the money

flowing into these companies via BPR

qualifying products is supporting the

economy and in turn the companies

are contributing to the overall tax take.

BPR incentivises the deployment of

capital into small businesses over long

timeframes - something that perhaps

only EIS, VCTs and BPR can achieve in

today’s economic climate.

While the concepts of avoidance and

evasion have merged somewhat

recently, it’s worth making clear that

BPR is a statutory relief established

in the 1976 Finance Act and the 1984

Inheritance Tax Act: it is not a tax

avoidance scheme of the kind that

occasionally lands celebrity investors

in hot water and it is not affected by

the General Anti-Abuse Rules (GAAR)

introduced in July 2013.

COMPARISONS TO OTHER

IHT SOLUTIONS

Whilst it is beyond the scope of this

report to cover in depth all of the estate

planning solutions that are available

to advisers, it makes sense to put BPR

into the context of other IHT mitigation

strategies as there are obviously

advantages and disadvantages

associated with each of them.

Broadly, there are

2 ways to reduce

IHT liabilities:

Asset reduction strategies

where steps are taken to reduce the

value of the estate

Asset replacement strategies

where assets that are liable for IHT are

replaced with exempt assets. IHT

solutions that utilise BPR would be part

of an asset replacement strategy

ASSET REDUCTION

STRATEGIES

CHARITY

We haven’t included charitable

legacies in our table below, but we

should mention them for the sake of

completeness. If 10% of an estate is left

to a registered charity, there is a 4%

deduction in the rate of inheritance tax

from 40% to 36%. It’s also worth noting

that donations to charities or political

parties made during the donor’s lifetime

are IHT exempt.

GIFTS

Gifts cover a wide range of possibilities.

Smaller gifts of up to £3,000 annually

are exempt from IHT. It is also possible

to make gifts from income, provided

that it can be demonstrated that they

are

a)

habitual

b)

made from post-tax

income and

c)

leave the donor with

sufficient income. This is a surprisingly

underutilised relief.

More common (and included in our

table) are Potentially Exempt Transfers

(PETs) where they are subject to IHT

on a sliding scale: three years from the

date of the gift there is 20% IHT relief,

and the relief increases by 20% every

subsequent year until 100% relief is

achieved after seven years.

£150m

£200m

£335m

£350m

£385m

VALUE OF

TAX RELIEF:

* less than 250 employees

08/09

09/10

10/11

11/12

12/13

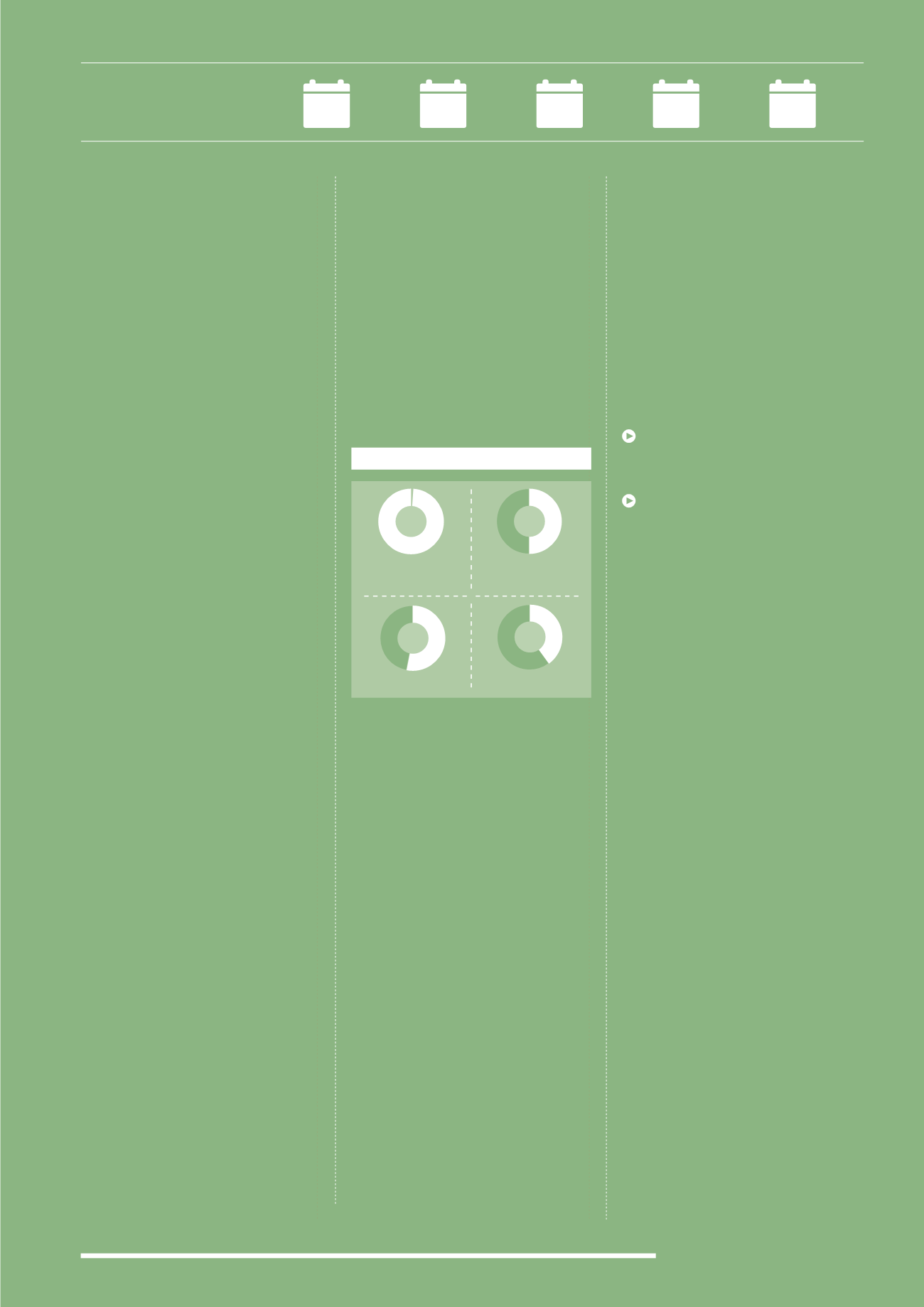

Employment

69

%

Businesses

in the UK

99

%

Gross Value

Added

50

%

Turnover

47

%

SMEs* ACCOUNT FOR

(2014)