51 / 92

51 / 92

51

“Reductions in the amounts that can be saved into pensions and threats to the tax relief available

in pensions have increased the need for tax-efficient investment options”

Creating a panel of VCTs requires an upfront

investment of resources, but can save time and effort

later on and ensures compliance to a centralised

investment proposition throughout a firm

PANEL CREATION STEPS

The key steps where external expertise

could be valuable would be deciding

on the correct filters to apply to reduce

the panel size, and developing a DDQ

questionnaire that is sufficiently

detailed and covers all of the issues that

need to be considered when sourcing

VCT products - it might look similar to the

high level due diligence areas listed in the

chart (left).

The purpose of monitoring the panel

is: to continually review the selection

criteria and ensure that they are right

for the client bank; to assess any new

products that meet the criteria (and

remove any products that no longer

do so); to review sales data and MIS

(management information statistics) to

see if there are any products that the

advisers are not selecting (or those that

have too much money going into them);

to identify any advisers that could do

more VCT business (or those that might

be doing too much); and to review and

act upon adviser feedback.

Putting the panel together and the

ongoing monitoring will probably be the

job of either the investment committee,

a sub committee convened specifically

to look at alternative investments such

as VCTs, or the equivalent body at an

advisory firm. The role of the investment

committee in relation to the panel would

comprise:

Ongoing review of panel selection

criteria

Final decision on investments that go

onto the panel

Review of current panel

Review of MIS (management

information statistics) to ascertain

whether the panel meets adviser needs

a) Volumes and amounts (£) sold

b) Breakdown by manager

c) Breakdown by product

d) Breakdown by adviser

Review of any new market

developments (news, legislation, press

coverage, new entrants, etc.)

Collect and review of adviser feedback

Report back to the full investment

committee or board

CONCLUSIONS

As we’ve seen, reductions in the

amounts that can be saved into pensions

and threats to the tax relief available

in pensions have increased the need

for tax-efficient investment options.

Pension freedoms may require advisers

to use more sophisticated decumulation

strategies, longer lives demand more

tax-efficient accumulation products and

in our low interest rate environment

nearly all investors are still searching for

higher yields. There are a lot of good

reasons to consider investing in VCTs.

The big caveat is that advisers must

ensure that they only use VCTs for

the right clients, and that the right

VCTs are selected. Of course this

comes down to appropriateness and

suitability, assessing the whole-of-the-

market, carrying out comprehensive

due diligence and having a thorough

understanding of the products that are

recommended. For advisory firms who

foresee that they will be doing a lot of

VCT business, using third party review

and comparison sites and setting up a

panel would probably save a lot of time

and effort on their part over the long run.

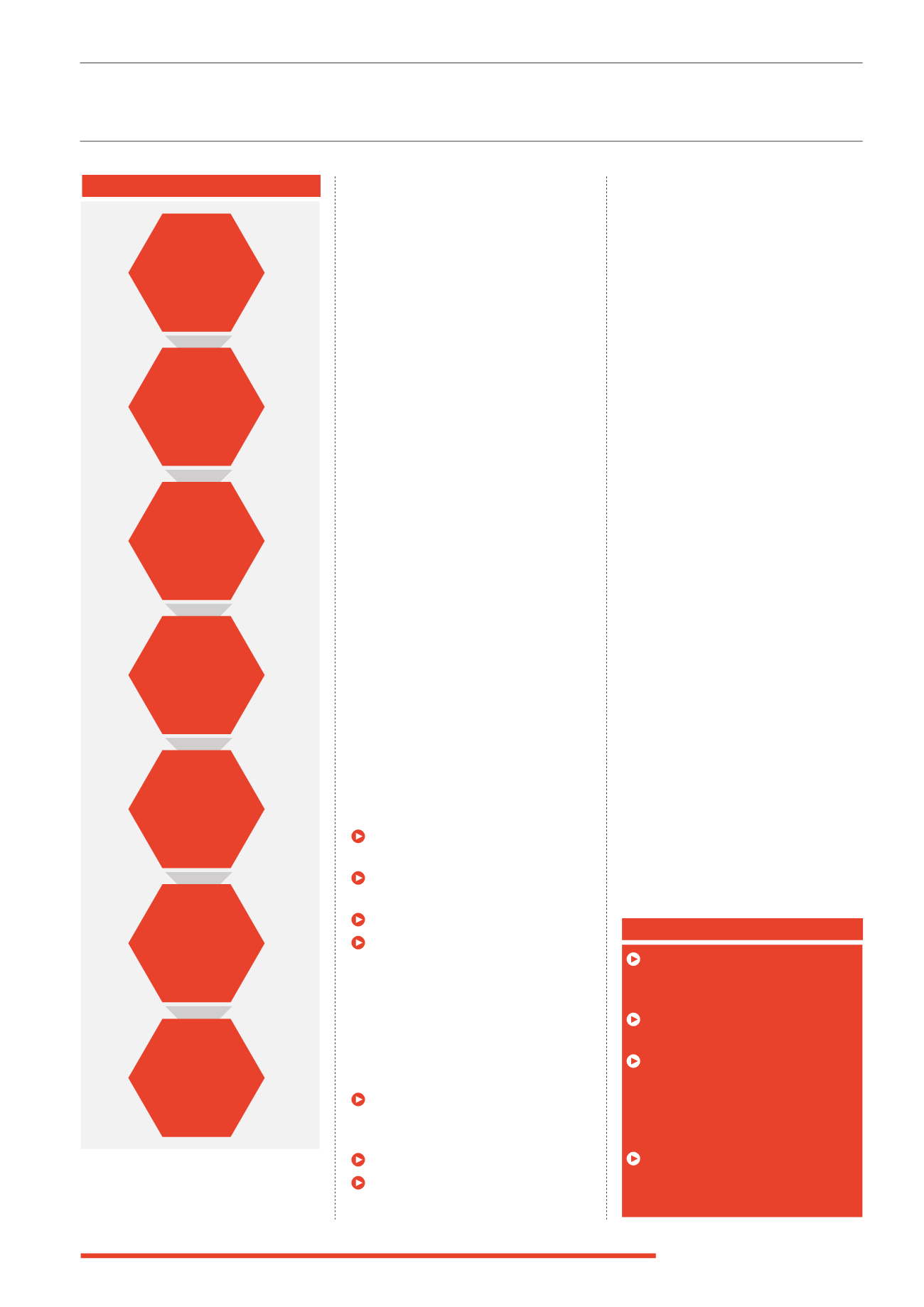

Identify all VCTs in

the marketplace

Apply filters

to reduce to a

manageable size

Send focused

questionnaire to

those on reduced

list

Evaluate returned

questionnaires and

create a shortlist

Meet with

providers (where

necessary) and

choose panel

Maintain and

monitor the panel

of VCTs

Keep records of

the research and

selection process

KEY POINTS

Suitability should primarily

be based upon the underlying

investments and not the tax reliefs

VCTs can be used to construct tax-

efficient decumulation strategies

Advisers’ due diligence has to cover

a lot of ground and consider features

that are unique to closed funds and

VCTs. It will be a longer process than

due diligence on conventional OEICS

Using a panel and a third party

comparison and review service can

save firms time and effort