32 / 40

32 / 40

32

adverse market conditions, private

equity firms inject more capital to pay

off a company’s debts and finance

expansion to take advantage of suitable

investment opportunities. One example

is US Private Equity firm Oaktree,

which now controls a series of shipping

companies including Genco Shipping

and Trading Ltd, a Dry Bulk shipping

company

75

.

This explains the massive influx of

private equity money into the shipping

sector in the last two to three years.

In 2013/2014, Bloomberg estimated

$5 billion and rising being invested in

that year alone by private equity and

hedge funds

76

. It is not surprising that

those with the cash are keen to take

the private equity route, as growing

evidence exists to suggest that private

equity outperforms the public stock

market over time; over the decade to

2013, its member funds generated an

annual return rate of 15.7%, compared

to 8.8% for the FTSE All-Share index.

77

In addition, the regulatory protection

of the FCA is available with private

equity as all private equity and venture

capital firms in the UK are regulated by

the Financial Conduct Authority (FCA)

and therefore the Financial Services

Compensation Scheme (FSCS) applies

78

.

However, entry levels are unlikely to be

within the reach of ordinary investors;

£200,000 or more, is a realistic figure

79

,

fees are high at around 2% annual

management charge levied on the

assets under management plus 20% of

the fund’s profits

77

and with no public

market, it is an illiquid investment

sector.

That said, whereas traditional ship

owners tend to hold vessels for at least

20 years, private equity groups hope to

turn a quick profit by listing companies

or selling their vessels once charter

rates and ship valuations recover

94

. The

usual exit target is three to seven years.

HEDGE FUNDS

Like private equity firms, hedge funds

have recently seen the value in investing

in the shipping market and they are

generally inaccessible to ordinary

investors. Typically institutions, such as

pension funds, university endowments

and foundations, or high net worth

individuals are the permitted investors,

with the significant resources required to

enter the market by this method.

Fees are similar to those in private

equity, however, hedge funds generally

invest in relatively liquid assets,

purchase minority positions in company

stocks and bonds for both long and

short term investment purposes and

have much greater liquidity than

the standard private equity route of

purchasing entire companies.

One of the most popular current

methods of hedge fund shipping

investment is purchasing the debt of

distressed companies, for example,

in August 2015, Reuters reported that

“Some of the U.S. hedge funds, often

described as “vulture funds” as they buy

assets cheaply before selling them on in

a rising market, are eyeing portions of

the 373 million euro ($406 million) debt

of shipping firm Premuda.”

80

ENTERPRISE INVESTMENT

SCHEMES

Government backed schemes such

as Enterprise Investment Scheme

(EIS) are vehicles for much smaller

levels of investment than that which

is available through private equity,

institutional or corporate players.

The generous tax reliefs for investors,

which were introduced to provide

incentives for investment in small

unquoted companies, with a perception

of higher-risk, are very attractive.

There is, however, a three-year period

during which investors must hold their

shares to access the tax benefits, which

effectively constitutes a lock- in.

An individual company can apply for EIS

status and investors are then invited

to acquire shares in it, thereby taking

some security over the assets of the

company. A UK company can qualify for

EIS status as long as it does not carry

out certain restricted activities (whilst

leasing or letting assets on hire is a

restricted trade, certain ship-chartering

activities are allowed) and meets other

criteria to ensure that its size is limited.

“Some of the U.S. hedge funds, often described as “vulture funds” as they buy assets cheaply before

selling them on in a rising market, are eyeing portions of the €373 million ($406 million) debt of

shipping firm Premuda”

Reuters

The minimum investment is £500 worth

of shares in any one company in any

one tax year, although in practice, this

minimum is set by the EIS itself and

might typically be £5,000 to £10,000.

Returns can vary considerably, with

targets often high, taking into account

the potential for small and sometimes

young companies, to grow rapidly.

Exit from EIS is variable and is likely

to be by way of sale of the underlying

investee company(ies) or their unlisted

shares after the three year holding

period has elapsed and sometimes

longer, depending on the optimum time

to sell and interest of buyers.

All types of government sponsored

investment schemes are vulnerable to

changes in legislation and in last quarter

of 2015, EIS underwent rule changes in

order to comply with European State

aid rules. As a result, EIS now has a

ten year sunset clause, so it will be

reviewed again in 2025 and this gives

the important advantage of giving the

sector a decade of stability.

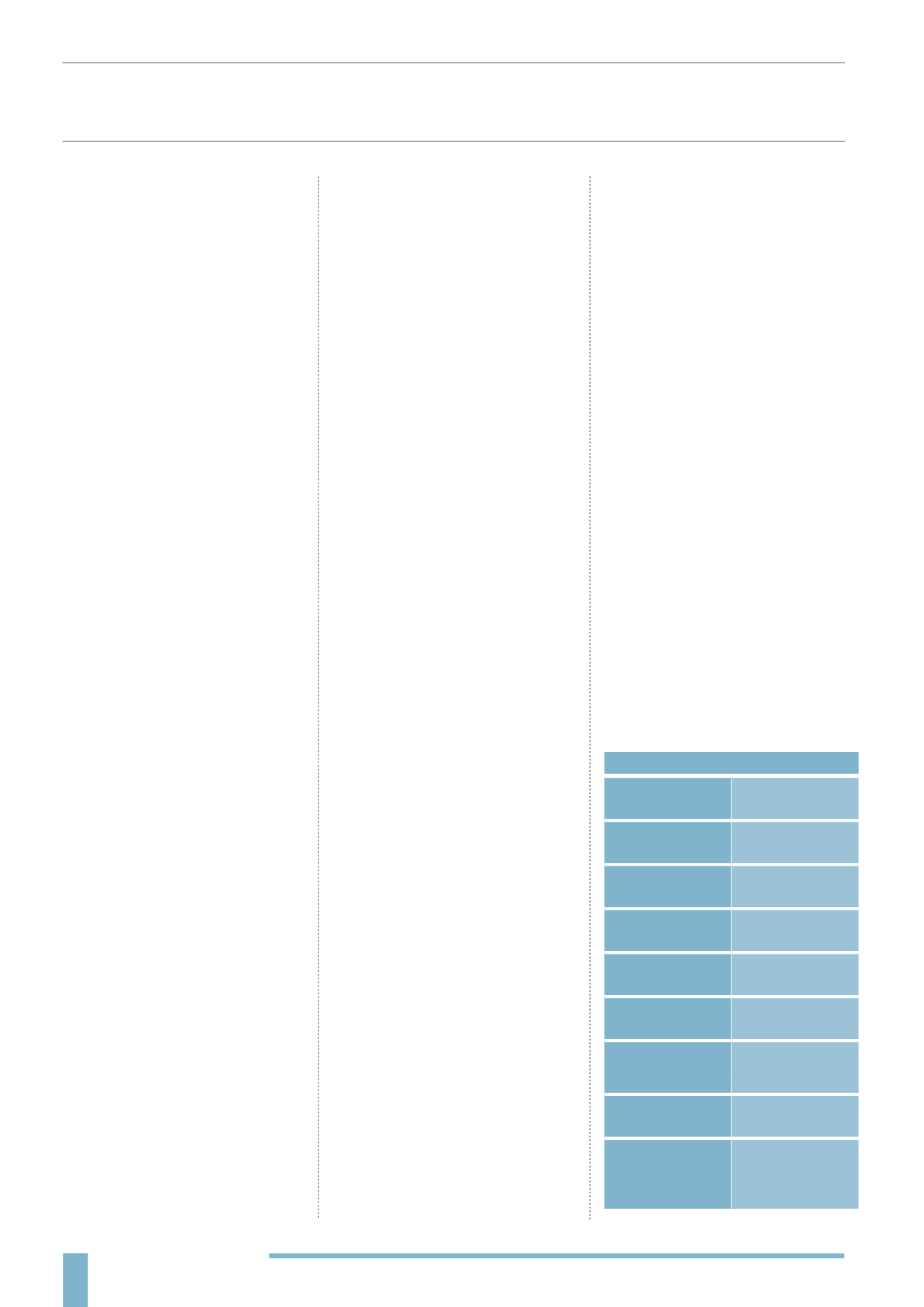

ANNUAL MAX.

INVESTMENT

£1 million

TAX

RELIEF

30%

HOLDING

PERIOD

3 Years

ONE YEAR

CARRY BACK

Yes

DIVIDENDS

Taxable

CAPITAL GAINS

TAX

Gains exempt

after 3 years

CAPITAL GAINS

DEFERRAL

RELIEF

Yes

CAPITAL GAINS

TAX HOLIDAYS

No

INHERITANCE

TAX

EXEMPTION

BPR available

after 2 years

for qualifying

investments

82

EIS TAX RELIEFS

81

(2015/2016)