35 / 40

35 / 40

35

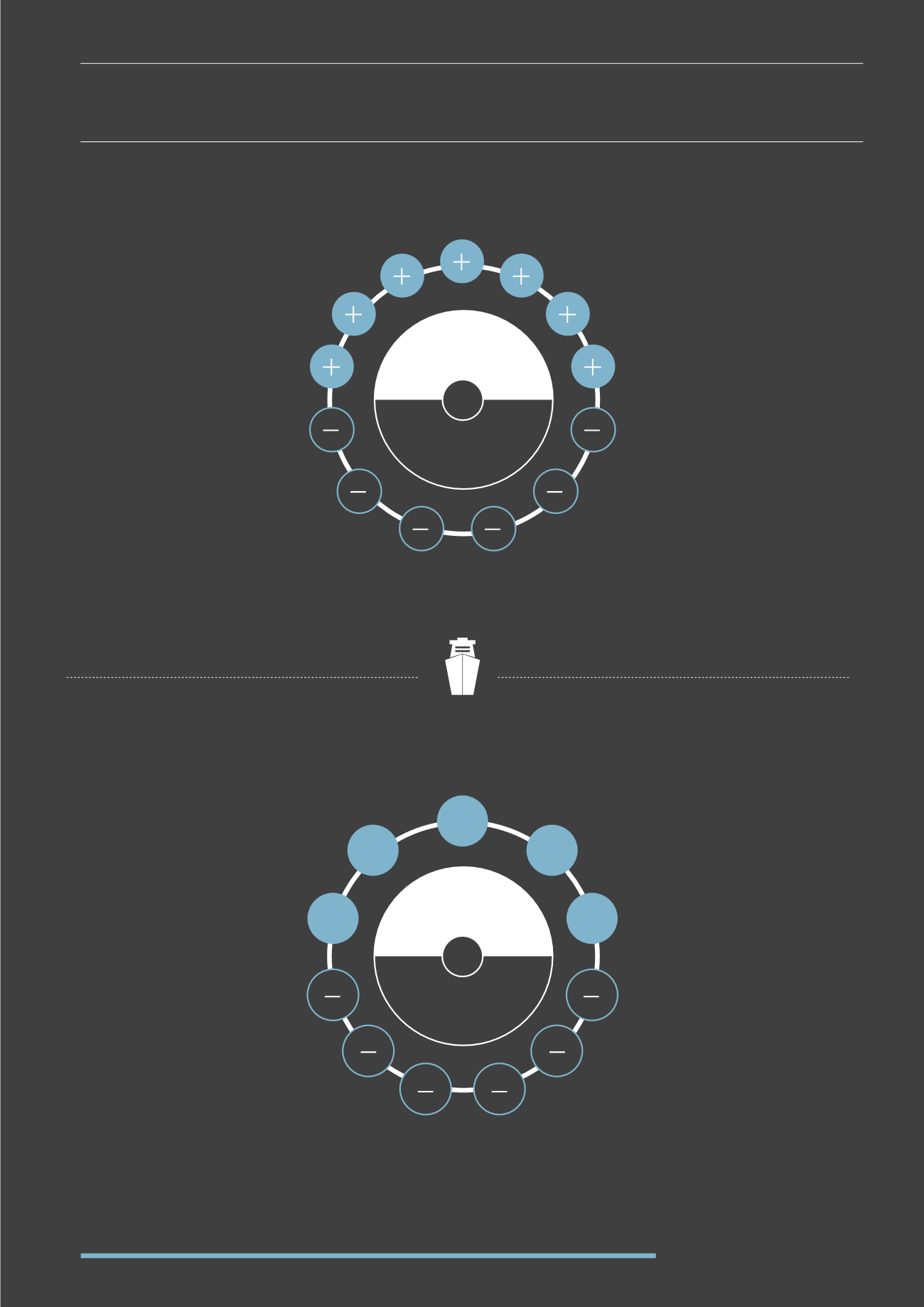

SWOT ANALYSIS

Growing world population and emerging

economies creating strong demand drivers

Essential sector for global industry and growth

Supported by the UK Department for Transport

Potential for significant capital growth with

the right investment, at the right time and

the right exit

Market volatility – very sensitive to

macroeconomic and political factors

Exposure to potential currency fluctuations

Potentially costly nature of ongoing

requirements for environmental/safety

upgrades

Most environmentally friendly method

of transporting goods and ongoing

improvements taking place

Real asset with safety net of scrappage to

partially offset potential capital loss

Long established business – with strong

history of long term growth driven by

proven drivers – e.g. globalisation, emerging

economies, world population growth

Accessible industry expertise

through UK owners and operators

Smaller scale private investors

have only recently started to

become fully aware of the market

Reduced availability of bank funding

Very complex market for the poorly

advised amateur – requires appreciation

of cyclical market with all of the global and

local demand factors

Over-supply of vessels, depressing

charter prices and ship values

Use of debt

Access to Dry Bulk shipping has historically been

largely limited to institutions, corporations and

private equity firms with access to the significant

funds and knowledge required to enter the market

Deterioration of general market conditions

which directly impact demand factors – e.g.

continued Chinese economic slow-down

Opportunities at the bottom of the

market when upturn is predicted

and eventual upswing in Dry Bulk

charter rates and vessel values

Concentration on one specific

sub sector of shipping – lack of

diversification

Availability of political support in the

form of UK Tonnage Tax and eligibility for

state aid and qualification for incentivised

investment schemes such as EIS and VCT

Inexperienced managers

if not carefully selected

Significant market data allows for

identification of most cost-effective

vessels and risk mitigation strategies

No guarantee of interested third parties to

acquire the asset at the desired price and

facilitate investor exit at expected level

OPPORTUNITIES

THREATS

+

+

+

+

+

STRENGTHS

WEAKNESSES