12 / 92

12 / 92

12

VALUE FOR MONEY?

ADVISERS MUST LOOK UNDER THE BONNET

As specialist investments, higher charges than stock market

based funds can be justified for VCTs. Specialist investment

teams need to put lots of time and effort into doing deals with

smaller companies where the flow of information is limited,

the firms are illiquid and the risks are high. Not all of these

deals come off, but the resource-intensive process still needs

to be paid for. Doing it well can pay handsomely, but the

expertise doesn’t come cheap. These charges are taken in the

form of initial fees, ongoing charges and bonuses for good

performance, although some VCTs charge investees rather

than investors.

It’s also important for advisers to note that some VCTs may

also charge arrangement and deal monitoring fees, fees for

placing non-executive directors on the board of their investee

companies and depository or custodian fees. They may also

charge the underlying investee companies. These underlying

costs should be flagged in the prospectus and it’s important that

as part of their selection process advisers examine them and

take a view on whether they represent good value for money.

The concern is that between the initial costs, annual costs

and discount on the NAV at exit, perhaps as much as half of

the 30% Income Tax relief could be wiped out. We look at

the issue of fees and incentives (and ensuring they align the

managers’ interests with investors’) on page 58.

The majority of advisers will be familiar with the risks of investing in smaller companies, be they AIM listed or unquoted. Smaller

companies can often (but not always) have weak or unproven business models, less financial resilience and be overly reliant upon a

handful of big customers.

However, there can be other risks hidden under the bonnet of VCTs that advisers need to be cognisant of: how liquidity is provided,

the provider’s ability to maintain the discount to the NAV and the interaction between fundraising and deployment are all examples

of nuts and bolts issues that require a little more digging during the due diligence process. We outline the challenges for advisers

and how they can overcome them on page 40.

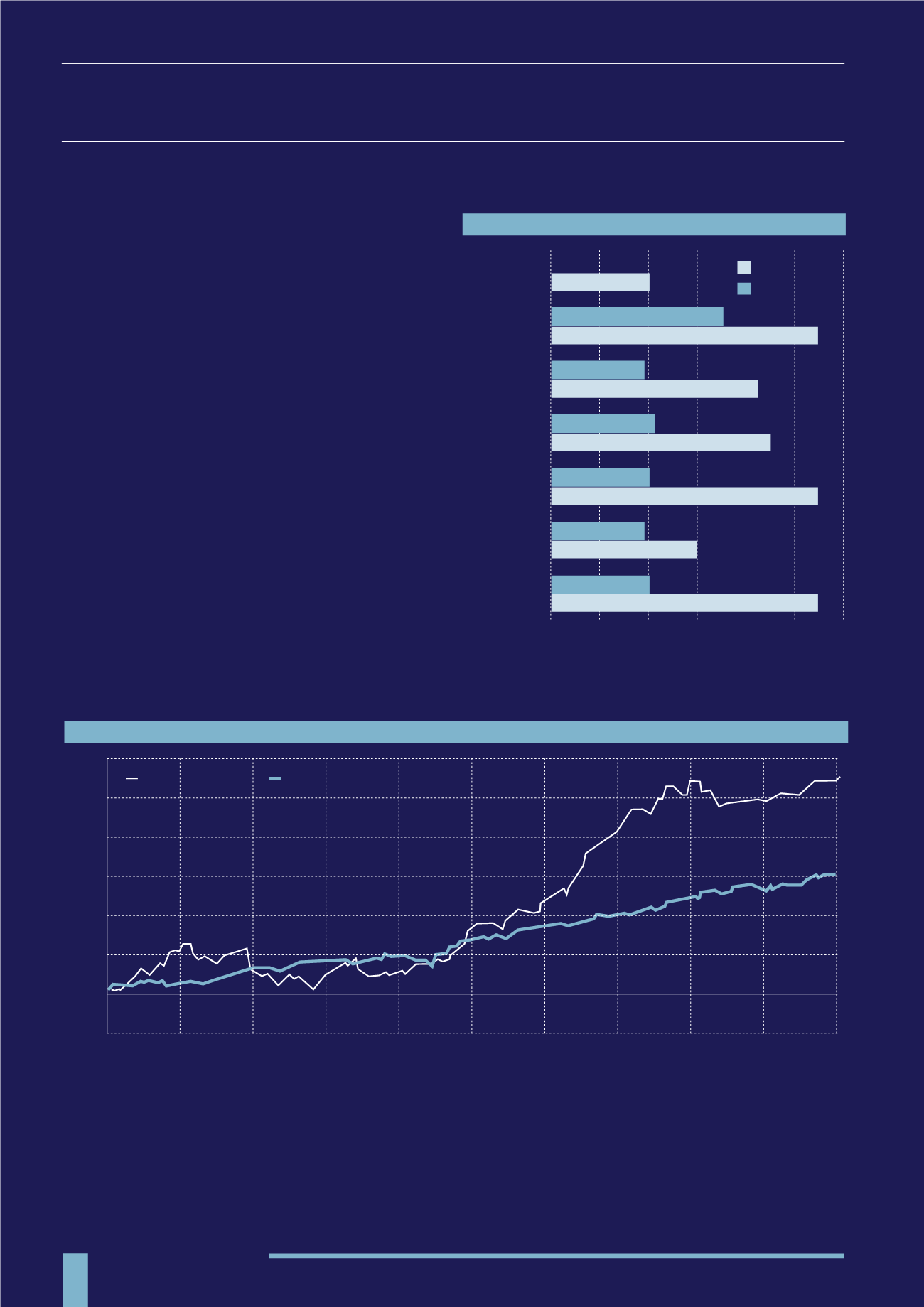

VCT CHARGES

(2015)

MINIMUM

MAXIMUM

AVERAGE

MEDIAN

MODE

LOWER

QUARTILE

UPPER

QUARTILE

VCT PERFORMANCE

(2010-2015)

“There can be other risks hidden under the bonnet of VCTs that advisers need to be cognisant of:

how liquidity is provided, the provider’s ability to maintain the discount to the NAV and the

interaction between fundraising and deployment”

0.0% 1.0%

Percentage charged against initial investment

where the charges are applied to investors

Volatility is not the only risk to consider with VCTs

Source: FE Trustnet (2015)

2.0% 3.0%

5.0%

4.0%

6.0%

Initial charge

Annual AMC

Feb 2011 Aug 2011

Aug 2010

-10%

0%

10%

20%

30%

40%

50%

60%

Aug 2012

Aug 2013

Aug 2014

Aug 2015

Feb 2012

Feb 2013

Feb 2014

Feb 2015

2.0%

1.92%

2.0%

2.0%

1.9%

2.0%

3.0%

3.5%

4.23%

4.5%

5.5%

5.5%

5.5%

VCT AIM Quoted

VCT Generalist