10 / 92

10 / 92

10

EXECUTIVE SUMMARY

FUNDRAISING IS STRONG AND THERE’S A GOOD INVESTMENT CASE

LOWER PENSION LIMITS MEAN THAT MORE ADVISERS ARE CONSIDERING VCTS

PENSION FREEDOMS COULD HAVE A SIMILAR IMPACT

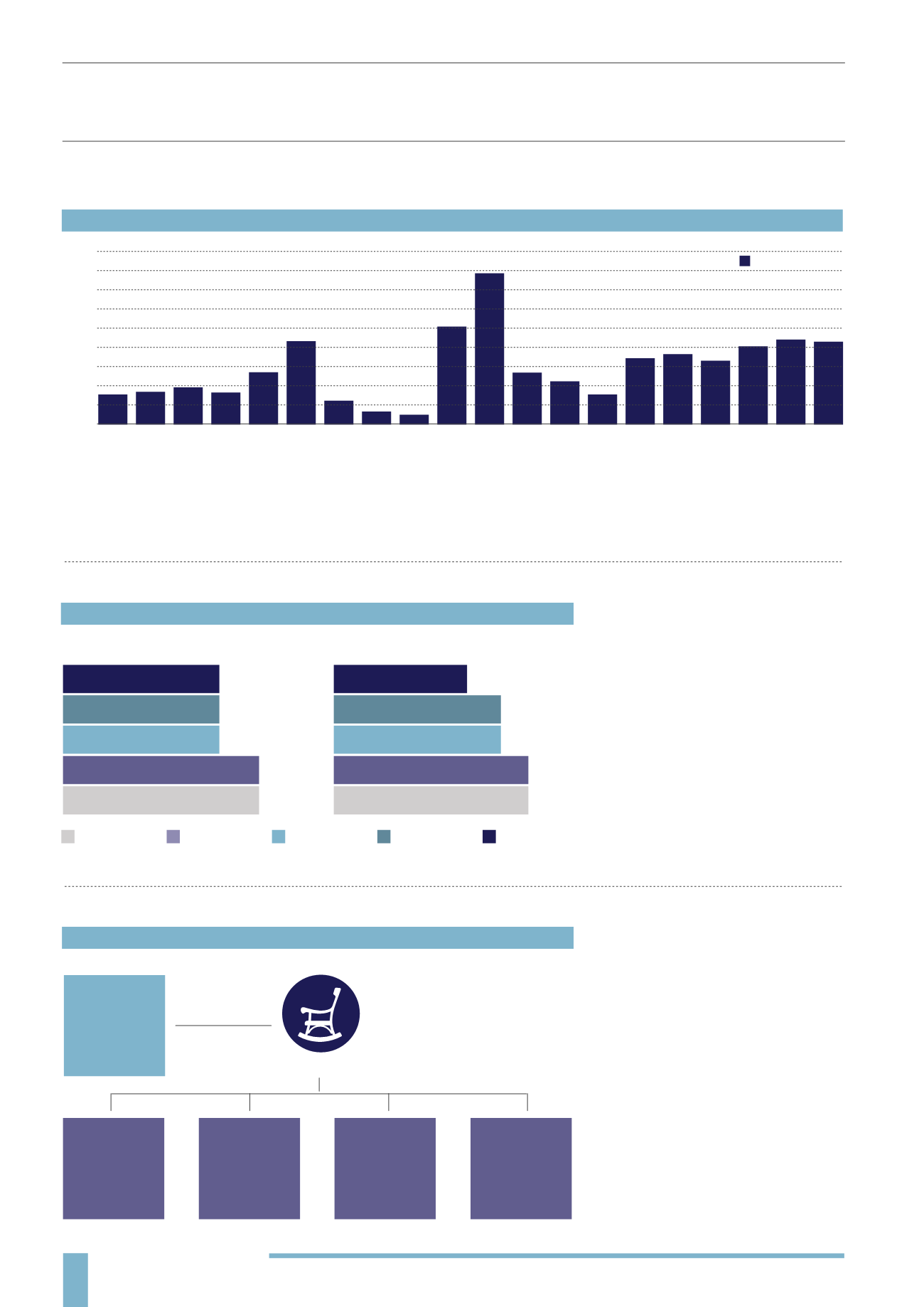

Three events have shaped the picture of historical fundraising into VCTs: the bear market in the early 00’s after the dot com boom,

the bear market after the financial crisis in 2008 and the “boost years” of 2005-06 when the upfront Income Tax relief available to

investors was lifted to 40%. If you can ignore those three events though, the picture is one of steady and consistent growth. We

think this is a sign of a healthy industry that is here is to stay. We look at the growth and development of the VCT market on page 21.

The new pension freedoms that came into

effect this year may mean that many more

investors defer buying an annuity and use

a drawdown solution. This will undoubtedly

mean that other sources of tax-free

income will be welcome to supplement the

(taxable) income from the pension pot and

preserve the capital left in there. Tax-free

dividends are perhaps VCTs strongest selling

point - the current average yield is over 8%

according to the AIC.

We cover how they can be used to develop

tax-efficient decumulation strategies on page

44. The changes to the way dividends are

taxed, announced in the July Budget, may

also make VCTs relatively more attractive.

VCT FUNDRAISING SINCE INCEPTION

(1996–2015)

OPTIONS AT RETIREMENT POST PENSION FREEDOMS

0

100

200

300

400

500

700

600

800

900

1996 1997 1998 1999 2000 2001 2002 2003

2006

2009

2012

2004

2007

2010

2013

2005

2008

2011

2014 2015

160 170 190 165

270

433

125

65

779

156

330

50

267

343

402

505

219

364

438 429

Source: AIC (2015)

We’ll look at the impact of changes to the

pension limits and what they mean for

investors on page 42. But what is clear is

that a number of investors are going to

max out what they can save in ISAs and

pensions, and are therefore going to look

to their advisers to find other tax-efficient

investments such as VCTs.

Pensions limits have been decreasing for some time

VCT Fundraising has been consistent and growing steadily since the 2009 recession

The “Pension Freedoms” announced in the 2014 Budget may require more sophisticated investment planning

AMOUNTS THAT CAN BE SAVED INTO PENSIONS BY TAX YEAR

ANNUAL ALLOWANCE

LIFETIME ALLOWANCE

Source: HM Treasury

2016/2017

2015/2016

2014/2015

2013/2014

2012/2013

£1 MILLION

£1.25 MILLION

£1.25 MILLION

£1.5 MILLION

£1.5 MILLION

£40,000

£40,000

£40,000

£50,000

£50,000

PENSION POT

FULL

WITHDRAWAL

(AT MARGINAL

RATE)

ANNUITY

DRAWDOWN /

OTHER PRODUCTS

UNCRYSTALLISED

FUNDS PENSION

LUMP SUM

25% TAX-FREE

LUMP-SUM

£ Millions