61 / 92

61 / 92

61

“VCTS ARE ONLY APPROPRIATE

WHEN BOTH ISA AND PENSION

ALLOWANCES HAVE BEEN

MAXIMISED”

DO YOU THINK IT IS

IMPORTANT TO USE MORE

THAN ONE VCT PROVIDER?

HOWLONG SHOULD A CLIENT

EXPECT TOHOLD THEIR SHARES

BEFORE LOOKING TO EXIT?

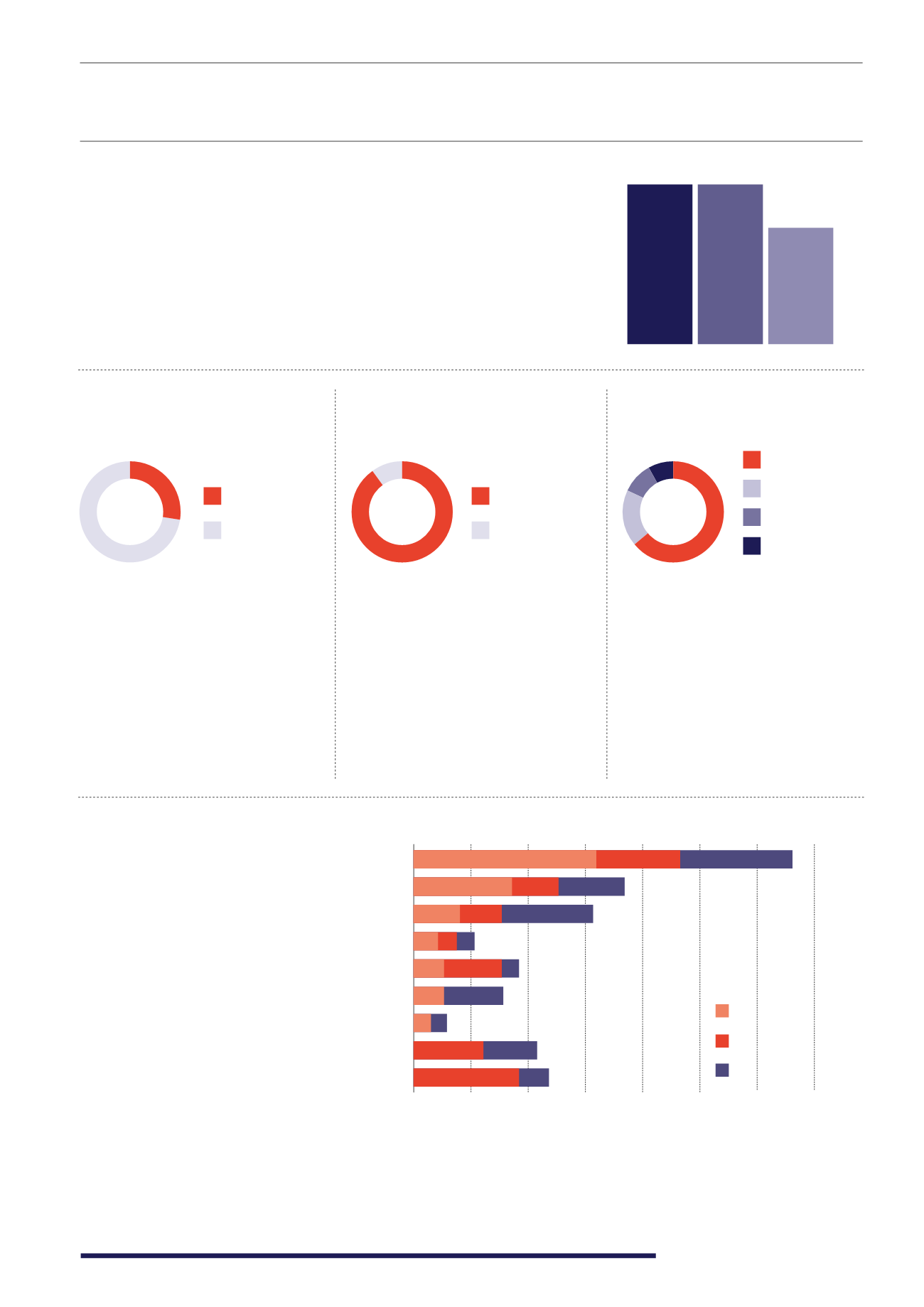

Only 28% believed that VCTs investments

only become appropriate once ISA

and Pensions contributions have been

maximised. The majority believe that

VCTs can coexist alongside these other

options as they offer additional benefits,

such as diversification and ability to

achieve higher returns.

The most important criterion (67%) when choosing a VCT is the managers’ performance track record. 34% and 31% of respondents

cited the economic sector the fund is exposed to and third party reviews respectively, as the second and third most important criteria

when choosing a VCT. Manager’s size and reputation (23%), previous good experience with the manager (18%) and the forecast timing

of exit (18%) were also important criteria. Referring back to a point made earlier in the report about the barriers to entry for new VCT

providers; the importance of track record and previous experience with manager further demonstrates how it is difficult for a new

provider to enter this space.

90% of financial advisers believe it is

important to use more than one VCT

provider. By choosing different managers

advisers can diversify across different

styles of investment, different sectors

and companies at different stages of

development. Most VCTs will usually

invest in around 10 to 30 companies.

Therefore, greater diversification is

difficult to achieve without investing

across several VCTs and VCT providers.

The majority (64%) of financial advisers

feel that their clients should hold onto

their VCTs for at least 6-10 years. While

the minimum holding period to achieve

the tax benefits is only 5 years, it will

often take longer to exit. Advisers seem

to be very aware of this issue, and are

appropriately making clients aware.

Using Limited Life VCTs would be one way

to address this issue if it was a concern.

“The majority of advisers believe that VCTs can coexist alongside Pensions and ISAs as they offer

additional benefits”

WHICH VCT INVESTMENT STRATEGIES

DO YOU RECOMMEND TO YOUR CLIENTS?

These are top level strategies, in which advisers may favour certain investment

managers, sectors or opportunities at a certain time. The majority of respondents

(58%) recommended investment strategies for capital growth or income. These two

options provide clients with the opportunity of gaining higher than average returns

and increase their income due to the income or Capital Gains Tax relief. 48% of advisers

recommended capital preservation as a strategy to invest in VCTs. This is the strategy

most commonly associated with Limited Life VCTs.

WHAT ARE THE 3 MOST IMPORTANT CRITERIA WHEN CHOOSING A VCT?

6-10 years

+10 years

Depends on

Only the minimum

5 years

8%

10%

18%

64%

Yes

No

10%

90%

Agree

Disagree

28%

72%

Most important

2nd most important

3rd most important

Manager’s performance track record

Economic sector fund is exposed to

Third party reviews

The forecast level of return

The forecast timing of exit

Quality of info provided on fund

Ease of investment

Previous good experience with the manager

Manager’s size & reputation in marketplace

31%

15%

21%

18% 8%

8%

5%

5%

5%

3%

13%

18%

8%

5%

3%

10%

10%

3%

3% 3%

8%

15%

8%

10%

0%

20% 30% 40% 50% 60% 70%

CAPITAL

GROWTH

INCOME

CAPITAL X

PRESERVATION

& GROWTH

57% 57%

48%