58 / 92

58 / 92

58

VCT PERFORMANCE

AND HURDLE FEES

Normally this section would show the

typical performance fees and hurdle

rates that are seen in the VCT market,

with some charts to show you at a glance

what to expect. However, our normal

data collection exercise of digging

through annual reports, third party

reviews and investment prospectuses,

found that although performance fees

are described as “in line with normal VCT

practice”, it seems that there actually is

no normal VCT practice for calculating

the performance hurdles.

However, we should also note that not all

VCT providers charge a performance fee.

Our analysis is based upon those that

do, but readers should be clear that it is

possible to find VCTs that only charge the

initial and ongoing fees, without taking a

share of the investors’ returns.

Performance fees are meant to align the

interest of managers and investors and

to motivate managers to generate higher

returns by meeting a particular hurdle

rate and taking a percentage of that

return above the hurdle rate. Some have

criticised the industry for not targeting

performance that is worth rewarding.

Now the performance fees aren’t the

difficult part to calculate – the industry

ranges from 10% to 30% of returns

made above the hurdle rate, with the

most common hurdle rate set at a

return of 20%.

It was examining the hurdle rate where

we encountered some problems. There

is not an industry standard and very few

are easily comparable. Some depend

on a certain distribution per share each

year, some on a certain distribution

amount and increase in NAV, some just

an increase in NAV, total returns that

beat inflation plus a certain percent, the

list goes on. The most common way in

which VCT managers calculate a hurdle is

through distributions to investors, but as

we say, don’t just trust that this is what

you’re signing up for: check the IM and

speak to the manager.

There seems to be a trend for Evergreen

funds to use dividends or total

distributions as a hurdle rate, which makes

it simpler. Limited Life VCTs set their hurdle

rates based on the total distribution to

investors when they close the fund.

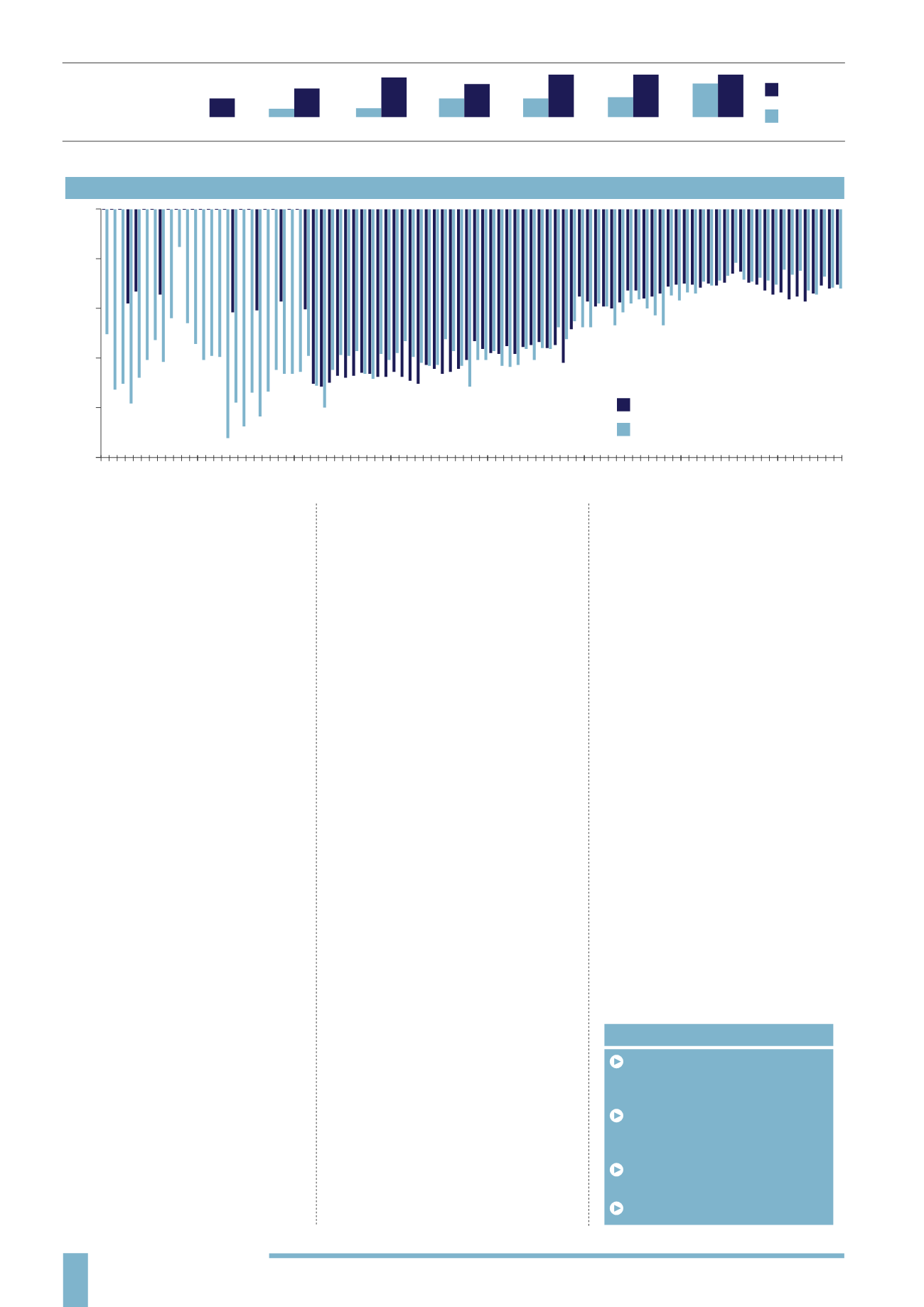

VCT DISCOUNTS

We examined the average discount over

time for the Generalist and AIM Quoted

sectors. Looking at the Generalist sector

discount, although we have some areas

of missing data, we can see the discounts

have ranged from 7.9% to 6.3% since

2008. For AIM VCTs the discount has

ranged from 3.8% to 23.1% in April 2009.

According to the AIC, the average

investment company discount at the

time of writing was near record low

levels of 5.2%, even after the volatility in

the market during the summer of 2015.

According to the AIC, currently 60% of

investment companies in the industry

have discount control policies. The

investment companies that do not have

themmainly invest in illiquid assets, like

KEY POINTS

Discounts have been as much as

-23.1% in the AIM Quoted sector, and

-17.6% in the Generalist sector

75% of VCTs are either focused on

growth, income or a combination of

both

Specialist VCTs have a much higher

concentration of assets

Average min. investment is £5,000

property and private equity, which would

be difficult to liquidate at a particular time.

The most widely used discount control

policy for VCTs are redemption offers,

although there are other types such as

tender offers and continuation votes.

Remember that the NAV can rise or

fall depending upon the frequency

of valuations and the timing of

any realisations or acquisitions of

underlying assets.

CONCLUSIONS

The market analysis shows us how the

VCT industry has developed over time,

introducing more products such as

AIM Quoted, Limited Life and Specialist

VCTs. We can see that there are

differences in the level of diversification

that these products tend to have, and

it is interesting to see how the discount

changes over time. Charges are higher

than more conventional investments,

which we think is reasonable given the

nature of their investment universe, but

it is difficult to assess and compare the

potential impact of performance fees.

VCT

CHARGES

(% OF INITIAL

INVESTMENT):

VCT DISCOUNTS

0

-5

-10

-15

-20

-25

2009

2010

2011

2012

2013

2014

2015

VCT Generalist sector

VCT AIM Quoted sector

MIN

2

MEDIAN

2

4.5

MODE

5.5

2

UQ

2

MAX

3.5

5.5

LQ

3

1.9

AVERAGE

1.92

4.23

Initial charge

Annual AMC

5.5