57 / 92

57 / 92

57

“Many Limited Life VCTs place significant focus on capital preservation, helping to ensure

downside protection by allocating capital to asset backed investments”

SamMcArthur, Puma Investments

Looking at the number of investee companies held by each structure also tells us

that it is harder to achieve maximum diversification in a Limited Life fund, as these

companies have to aim to wind up as soon as the proposed investment term is up

(usually five years). Lower levels of diversification are accepted in exchange for a more

defined exit.

NUMBER OF INVESTEE COMPANIES BY STRUCTURE

(2015)

Min

Lower Quartile

Average

Upper Quartile

Max

Since 2008 investors have become more concerned with liquidity and Limited Life

funds have grown in popularity. There is also less of a need to launch new Evergreen

products, as there are established funds with track records that periodically open for

new investment, making life harder for new market entrants.

MARKET SHARE BY STRUCTURE

(1995-2015)

Evergreen

Limited life

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2015

2004

2014

2003

2013

2002

2012

2001

2011

2000

2010

1999

2009

1998

2008

1997

2007

1996

2006

1995

2005

52%

51%

51%

50%

45%

37%

24%

16%

10%

4%

2%

48%

49%

49%

50%

55%

63%

76%

84%

90%

100%

100%

96%

100%

100%

98%

100%

100%

100%

100%

100%

100%

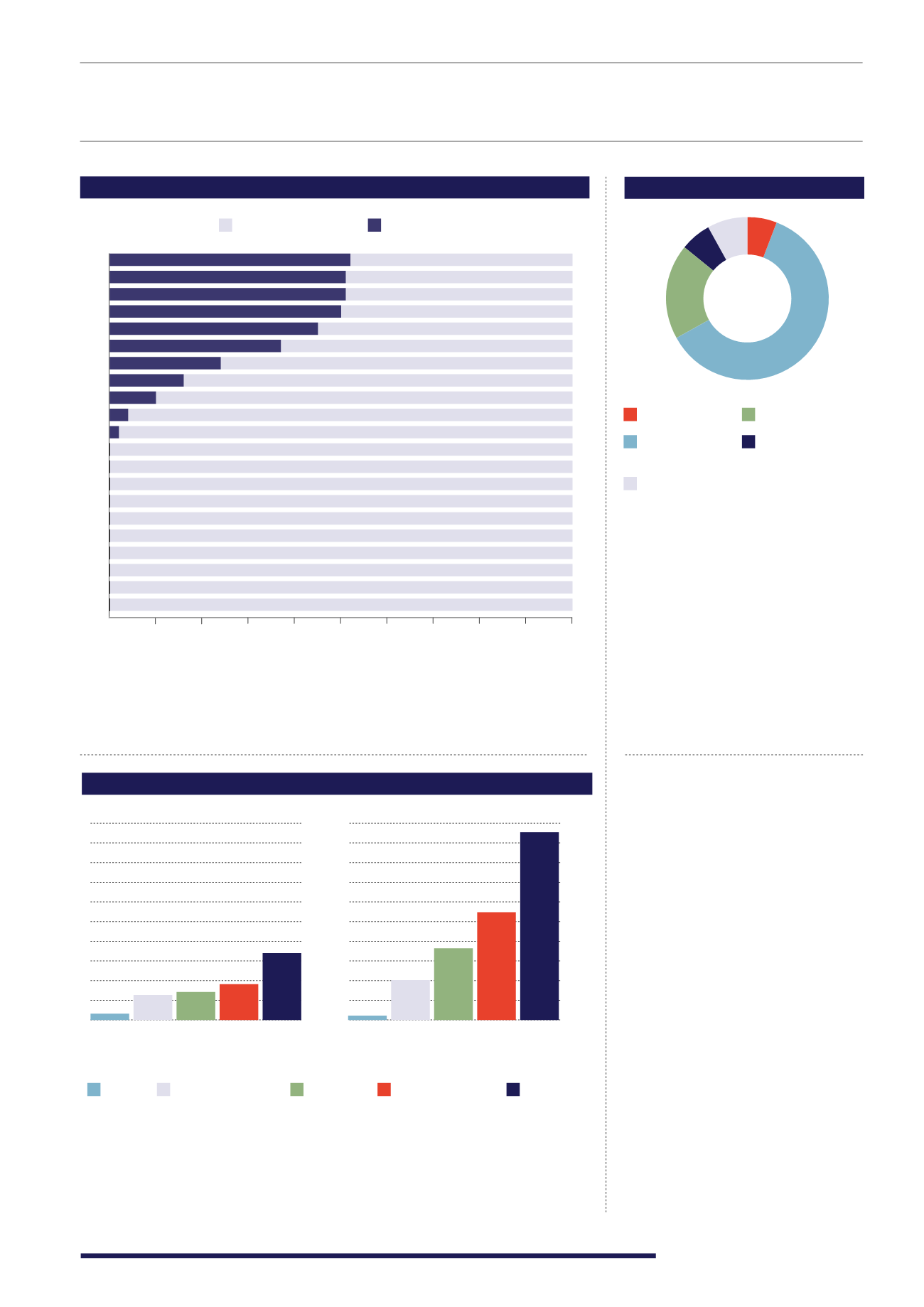

The majority (61%) of VCTs are focused

on capital growth & income. Dividends

received are tax-free and the nature of

the underlying investments of VCTs

goes hand in hand with the capital

growth objective. The second largest

segment is aimed at capital preservation

(19%). Although this focus may seem

unusual considering the inherent risk

that comes with VCTs, Limited Life VCTs

aim to wind up and distribute assets

after a target holding period.

INVESTMENT OBJECTIVE

61%

6%

6%

19%

8%

FEES AND CHARGES

Fees and charges are an important

consideration for advisers and

investors. This section takes a look at

the investments that were open to new

investment in November 2015. There

are two main charges associated to

VCTs when first making an investment:

the initial charge and the annual

management charge. Initial charges

range from 2% to 5.5% of the initial

subscription amount and the annual

management charge range from 0% to

3.5% of the net asset value.

The charges for VCTs are very

similar to that of EIS investments.

VCTs, along with EIS, require a large

amount of research and due diligence

by the managers when investing

shareholders’ funds (even more so

with the new legislation), one of the

many reasons why charges are higher

than mainstream funds.

Capital Growth

Capital Growth

& Income

Capital Preservation

Capital Preservation

& Income

Income

LIMITED LIFE

EVERGREEN

3

2

13

20

37

53

109

18

32

16