66 / 92

66 / 92

66

“The majority of providers believe that investors do not need to wait until ISA and pension

allowances have been maximised before investing in VCTs”

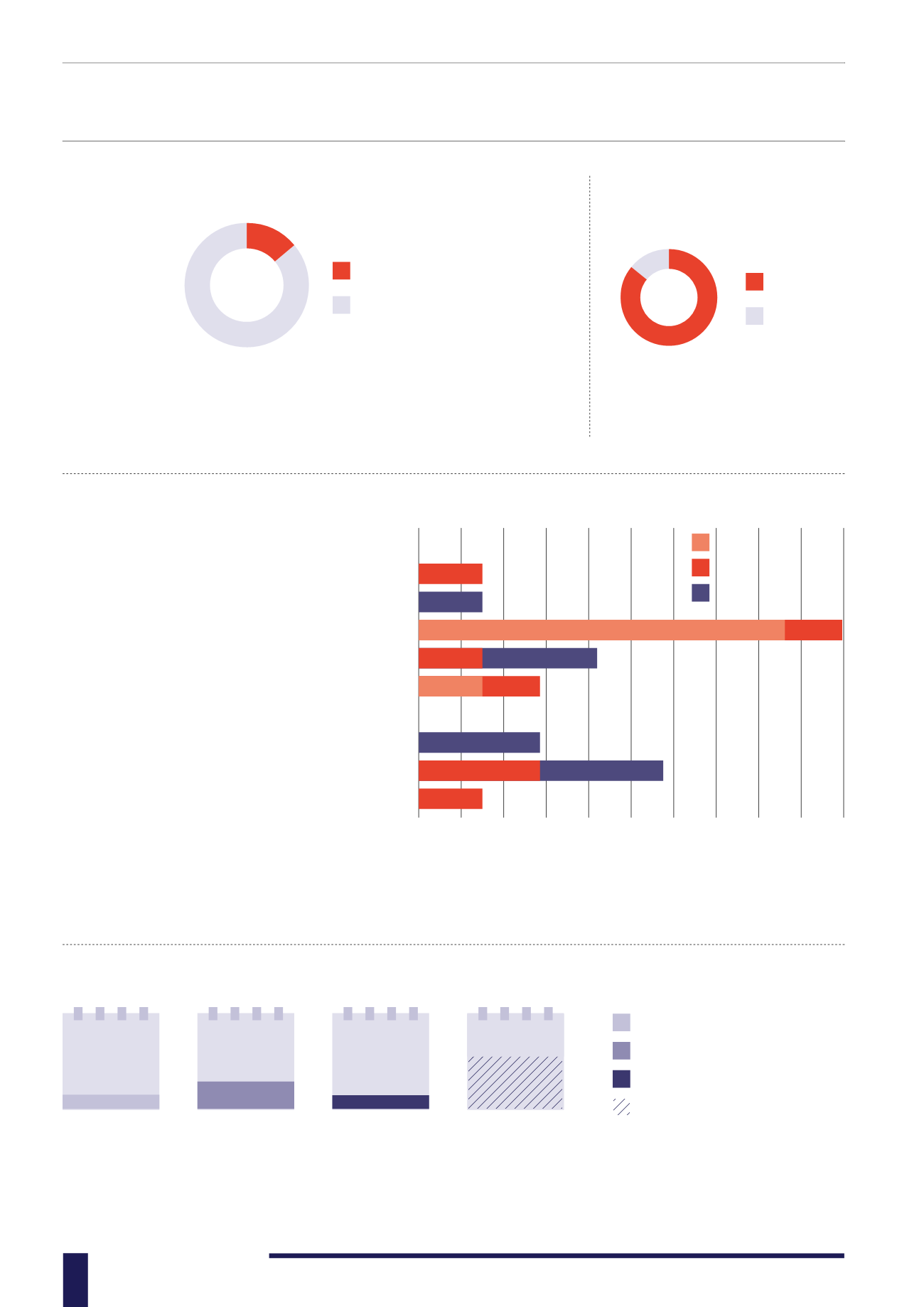

VCTS ARE ONLY APPROPRIATE WHEN BOTH ISA & PENSION

ALLOWANCES HAVE BEEN MAXIMISED

HOW LONG SHOULD AN INVESTOR EXPECT TO HOLD THEIR SHARES BEFORE LOOKING TO EXIT?

DO YOU THINK IT IS IMPORTANT

FOR INVESTORS TO USE MORE

THAN ONE VCT PROVIDER?

Providers believe that their track record is by far the most important criteria for investors/advisers when it comes to choosing a

VCT. Third party reviews, the sector they are investing in and expected level of returns were other important criteria noted by

providers, again chiming with advisers’ thoughts.

This question received a variety of responses, and this is definitely down to what type of VCT the provider offers. Of course Limited

Life VCTs aim to exit after only 5 years, whereas AIM or Generalist VCTs would normally be considered longer term investments.

WHAT ARE THE 3 MOST IMPORTANT CRITERIA FOR INVESTORS / ADVISERS WHEN CHOOSING A VCT?

The majority of providers believe that investors do not need to wait until ISA and

pension allowances have been maximised before investing in VCTs. However, more

advisers agreed with this statement, with 28% stating that the allowances should be

maximised before considering VCTs.

Even the providers aren’t ignorant

to the fact that to achieve greater

diversification, advisers and investors

need to look to several VCT providers.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Top criteria

2nd top criteria

3rd top criteria

Ease of investment

The forecast level of return

The forecast timing of the exit

The manager’s performance track record

The economic sector the fund is exposed to

The quality of information provided on the fund

Previous good experience with the manager

Third party reviews

The manager’s size & reputation in marketplace

Other

The minimum 5 years

6-10 years

+10 years

Depends on the investor

14%

29%

14%

43%

Agree

Disagree

14%

86%

Yes

No

86%

14%

14%

14%

14%

14%

14%

23%

29%

29%

14%

29%

86%

14%