53 / 92

53 / 92

53

OVERALL ANALYSIS

In this section we help readers get their arms around the whole of the VCT market by compiling and examining some of the available data

on VCTs, both historically and for today’s open offers. Much of the data has come from MICAP Ltd, the online platform and comparison

engine for tax-efficient alternative investments. Intelligent Partnership is a part of the same group of companies as MICAP.

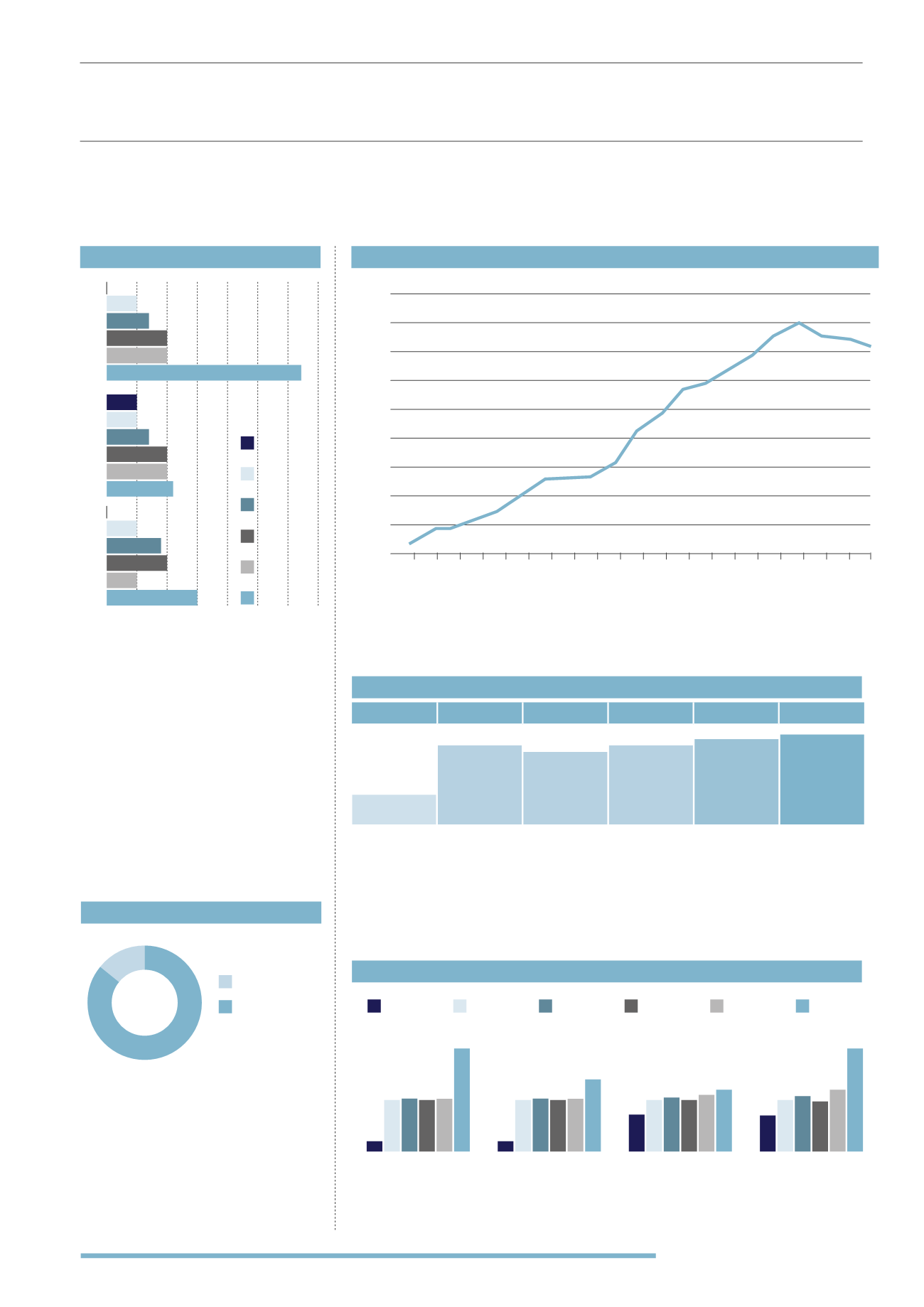

The VCT market development shows consistent growth in the market until 2012. Since 2012 there

has been some consolidation in the market, with several mergers in 2013. The consolidation of the

market is a positive result from the rule changes seen in the VCT sector; limits on VCTs lifted allowed

for companies to merge and become more cost effective and competitive.

At the time of writing the difference between

the NAV and share price range from a 150%

premium to a 70% discount. Many VCT

shareholders will not want to rely on selling

their shares on the secondary market for an

exit and instead, providers offer investors

the opportunity to sell back their shares after

a certain time frame at a given discount or

discount range. Some will buy back shares at a

nil discount to NAV, but the most common policy

in the market is to buy back at a 10% discount.

As we noted earlier, these policies are subject

to the VCT having the funds available to buy-

back shares.

Minimum investment levels are consistent across the whole market. The most common entry level

is £5,000, but the highest minimum investment level is only £6,000. In cases where investment

managers are offering shares in several VCTs or VCT share classes, they may allow investors to

split their investment across several VCTs, lowering the minimum investment per VCT and allowing

greater diversification benefits. The minimum investments are higher than mainstream stock market

based OEICS, but lower than more risky EIS and other venture capital and private equity funds.

Tax-free dividends are possibly the most attractive feature of VCTs and many funds state what

levels of dividends they will be targeting for their investors. The yields are attractive compared to

many other assets (although of course the additional risks and costs must be taken into account).

OVERALL VCT MARKET GROWTH

(1995-2015)

SHARE BUYBACK POLICIES

MINIMUM INVESTMENT

(2015)

TARGET DIVIDEND RETURNS

(PENCE PER SHARE)

(2015)

A substantial majority of VCTs are closed for

new investment at around 86%. Only a small

portion (14%) of the overall VCT market is open

for new investment. However, Evergreen VCTs

open and close periodically for top-up offers or

by way of new share class. This allows advisers

and investors to choose from a range of

established products and invest at the time tax

benefits are needed.

OVERALL VCT STATUS

Open

Closed

86%

14%

15

22 26

36

47 48 49

59

80

92

109

114

123

133

147 147 145

141

155

3

12

180

160

140

120

Number of operating VCTs

100

80

60

40

20

10

95

98

02

96

99

03

95

00

04

08

06

10

13

97

01

05

09

12

07

11

14

Overall

1

1

3.6

3.5

5

5

5

5

5.15

5.15

5.25

5.38

5

5

5

5

5.13

5.13

5.5

6

10

7

6

10

Generalist

AIM

Specialist

Min

LQ

Average

Mode

UQ

Max

15

MIN

LQ AVERAGE MODE

UQ

MAX

GENERALIST

SPECIALIST

AIM

Min

LQ

Average

Mode

UQ

Max

10% 5% 0%

15% 20% 25% 30% 35%

10%

5%

5%

5%

5%

5%

7%

7%

10%

10%

9%

10%

11%

15%

10%

32.2%

£6,000

£5,750

£5,000

£5,000

£2,000

£4,920